Financial News

2 Reasons to Like BY and 1 to Stay Skeptical

Since January 2025, Byline Bancorp has been in a holding pattern, posting a small loss of 2.7% while floating around $27.73. The stock also fell short of the S&P 500’s 4.5% gain during that period.

Given the weaker price action, is now a good time to buy BY? Or should investors expect a bumpy road ahead? Find out in our full research report, it’s free.

Why Does Byline Bancorp Spark Debate?

Ranking as the fifth most active Small Business Administration lender in the country, Byline Bancorp (NYSE: BY) is a Chicago-based bank that provides banking services to small and medium-sized businesses, commercial real estate developers, and consumers.

Two Things to Like:

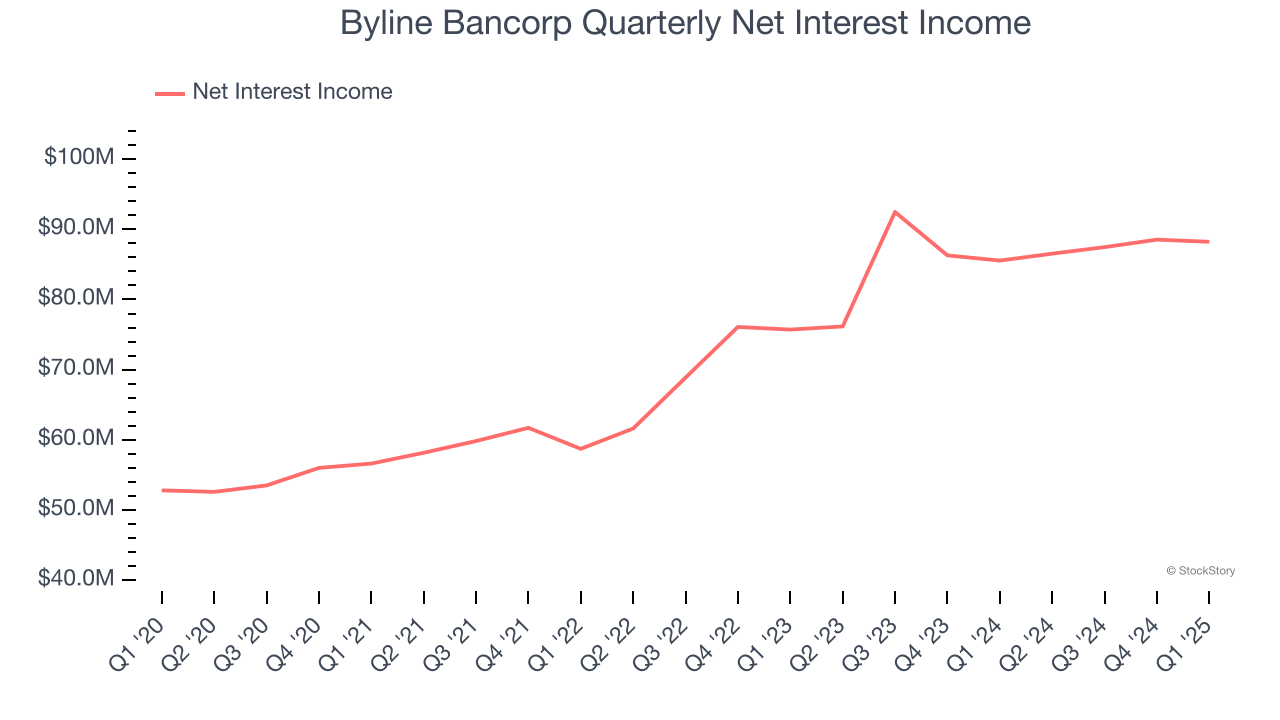

1. Net Interest Income Skyrockets, Fueling Growth Opportunities

Net interest income commands greater market attention due to its reliability and consistency, whereas non-interest income is often seen as lower-quality revenue that lacks the same dependable characteristics.

Byline Bancorp’s net interest income has grown at a 12.5% annualized rate over the last four years, better than the broader bank industry. Its growth was driven by an increase in its net interest margin, which represents how much a bank earns in relation to its outstanding loans, as its loan book shrank throughout that period.

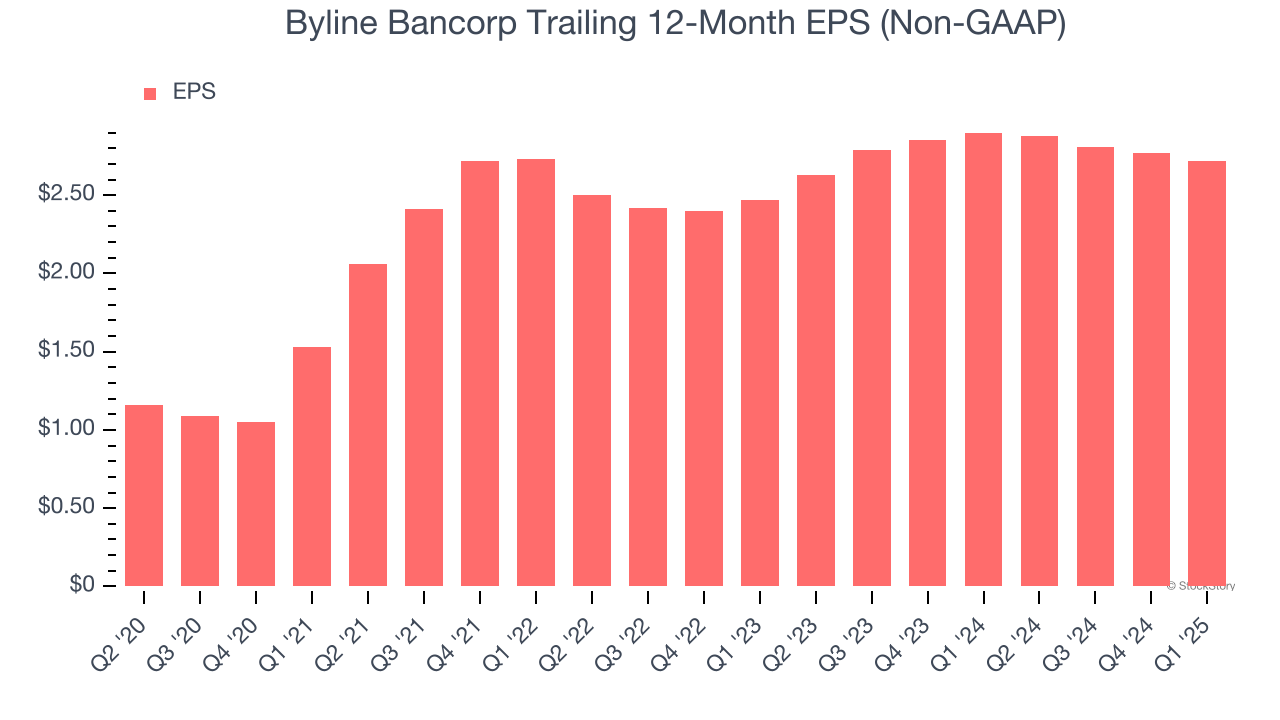

2. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Byline Bancorp’s EPS grew at an astounding 17.3% compounded annual growth rate over the last five years, higher than its 8.5% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

One Reason to be Careful:

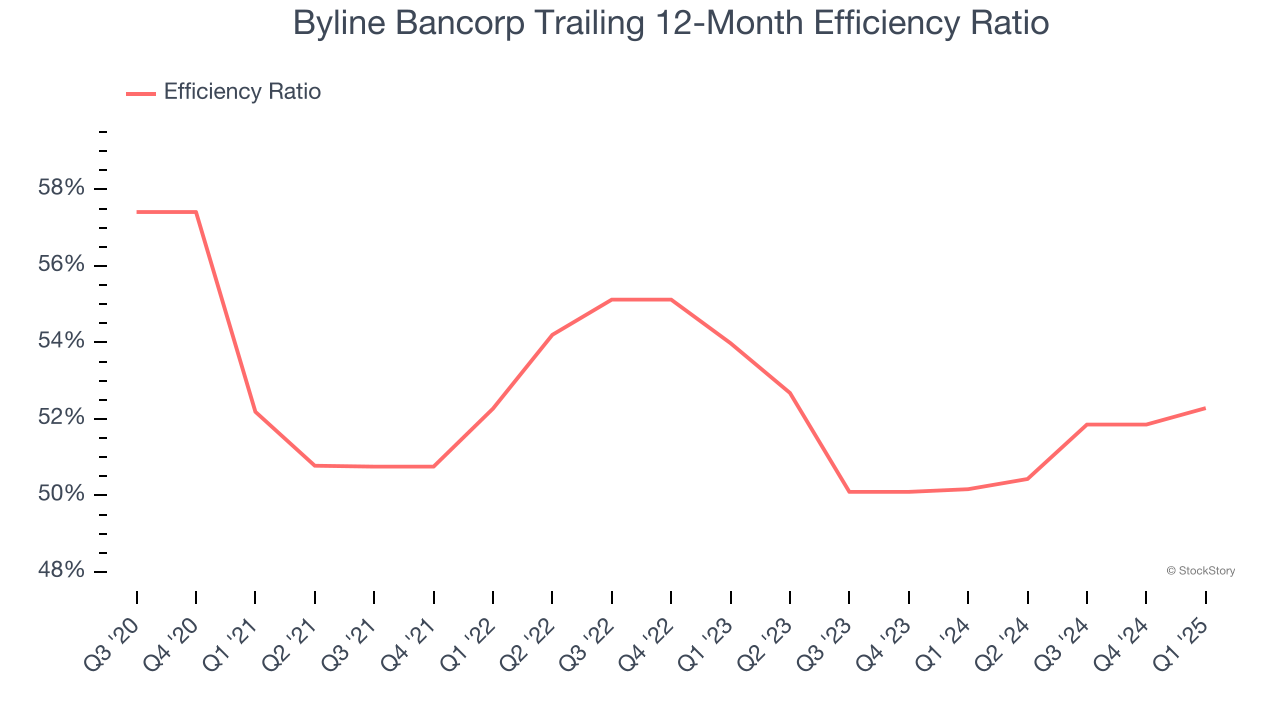

Efficiency Ratio Expected to Falter

The underlying profitability of top-line growth determines the actual bottom-line impact. Banking institutions measure this dynamic using the efficiency ratio, which is calculated by dividing non-interest expenses like personnel, facilities, technology, and marketing by total revenue.

Investors focus on efficiency ratio changes rather than absolute levels, understanding that expense structures vary by revenue mix. Counterintuitively, lower efficiency ratios indicate better performance since they represent lower costs relative to revenue.

For the next 12 months, Wall Street expects Byline Bancorp to become less profitable as it anticipates an efficiency ratio of 53.7% compared to 52.3% over the past year.

Final Judgment

Byline Bancorp has huge potential even though it has some open questions. With its shares trailing the market in recent months, the stock trades at 1× forward P/B (or $27.73 per share). Is now a good time to initiate a position? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than Byline Bancorp

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.