Financial News

2 Reasons to Watch RBC and 1 to Stay Cautious

Since July 2020, the S&P 500 has delivered a total return of 95.5%. But one standout stock has nearly doubled the market - over the past five years, RBC Bearings has surged 184% to $378.24 per share. Its momentum hasn’t stopped as it’s also gained 24.2% in the last six months, beating the S&P by 17.1%.

Is now still a good time to buy RBC? Or are investors being too optimistic? Find out in our full research report, it’s free.

Why Does RBC Bearings Spark Debate?

With a Guinness World Record for engineering the largest spherical plain bearing, RBC Bearings (NYSE: RBC) is a manufacturer of bearings and related components for the aerospace & defense, industrial, and transportation industries.

Two Positive Attributes:

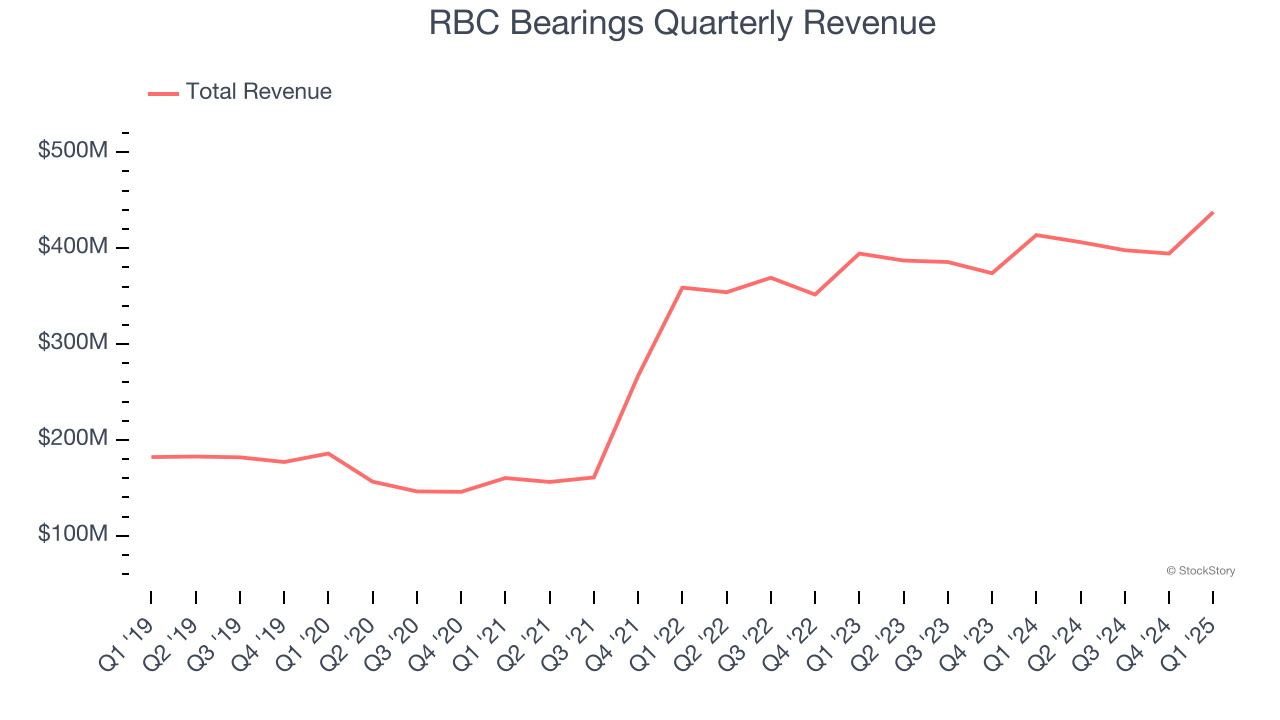

1. Skyrocketing Revenue Shows Strong Momentum

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Thankfully, RBC Bearings’s 17.6% annualized revenue growth over the last five years was incredible. Its growth beat the average industrials company and shows its offerings resonate with customers.

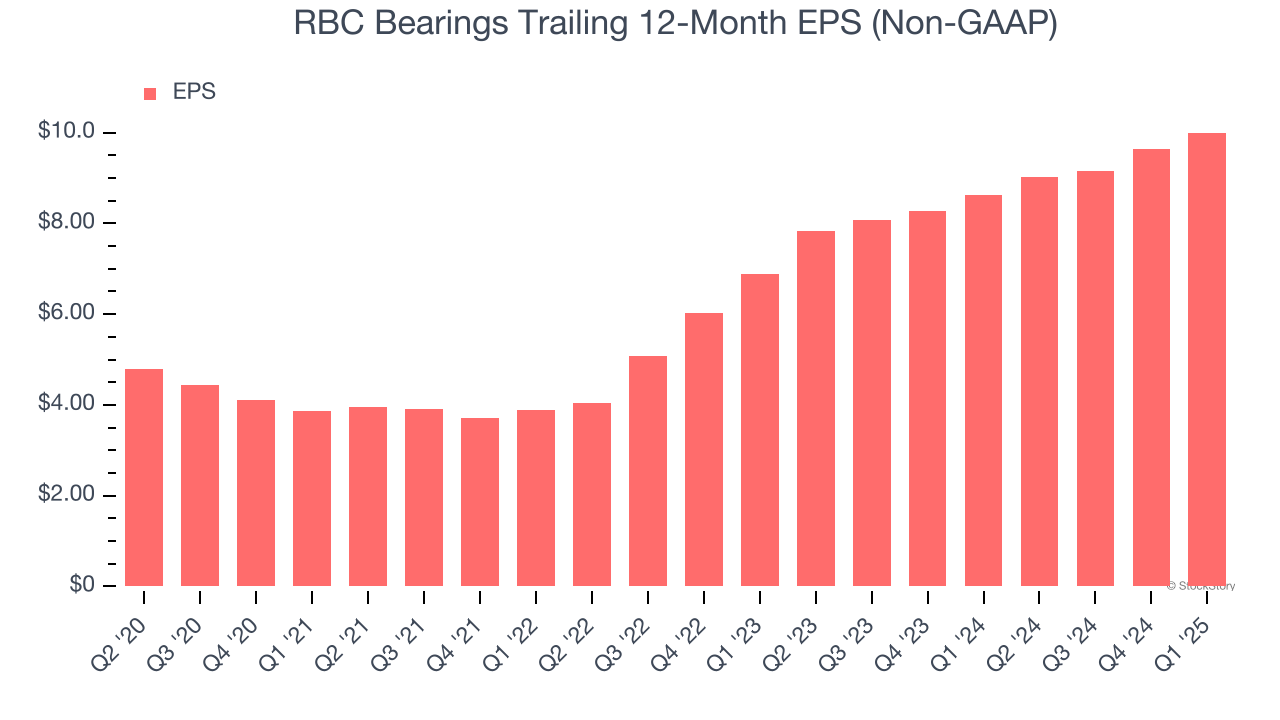

2. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

RBC Bearings’s EPS grew at a remarkable 14.1% compounded annual growth rate over the last five years. This performance was better than most industrials businesses.

One Reason to be Careful:

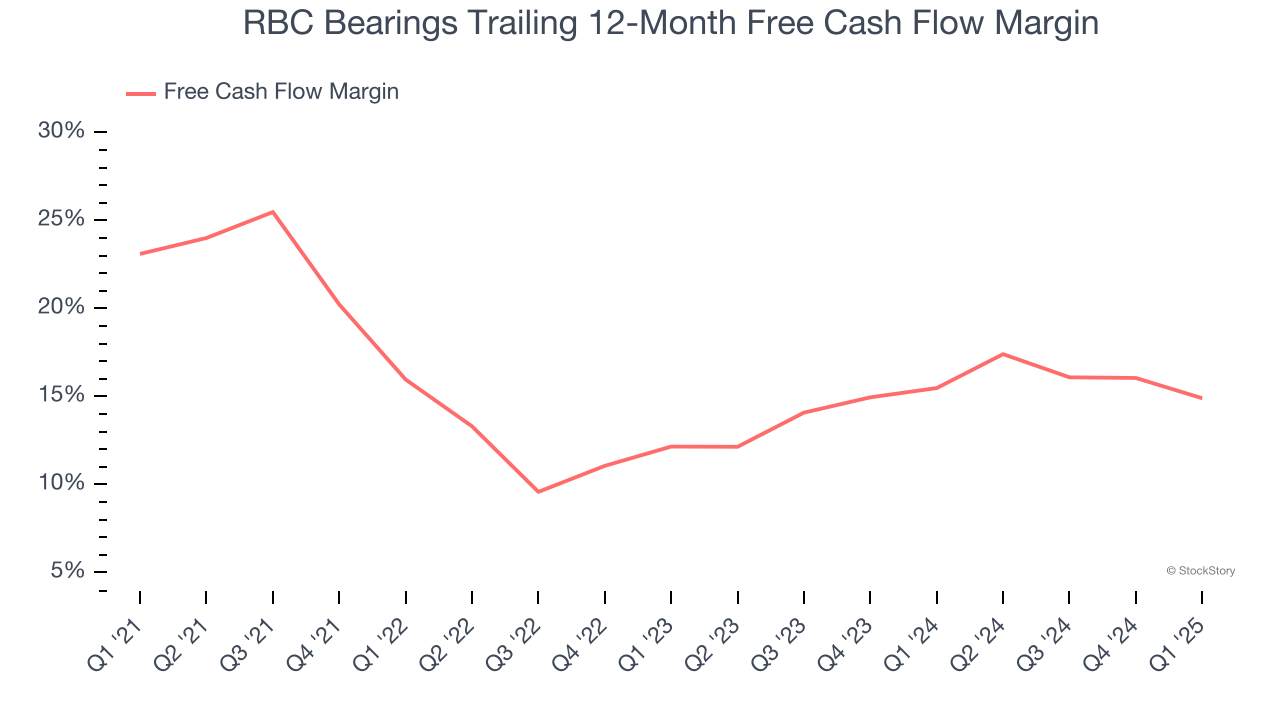

Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, RBC Bearings’s margin dropped by 8.2 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. RBC Bearings’s free cash flow margin for the trailing 12 months was 14.9%.

Final Judgment

RBC Bearings’s positive characteristics outweigh the negatives, and with its shares beating the market recently, the stock trades at 34.5× forward P/E (or $378.24 per share). Is now a good time to initiate a position? See for yourself in our comprehensive research report, it’s free.

High-Quality Stocks for All Market Conditions

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

More News

View More

Recent Quotes

View MoreQuotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.