Financial News

Unpacking Q1 Earnings: Photronics (NASDAQ:PLAB) In The Context Of Other Semiconductor Manufacturing Stocks

The end of the earnings season is always a good time to take a step back and see who shined (and who not so much). Let’s take a look at how semiconductor manufacturing stocks fared in Q1, starting with Photronics (NASDAQ: PLAB).

The semiconductor industry is driven by demand for advanced electronic products like smartphones, PCs, servers, and data storage. The need for technologies like artificial intelligence, 5G networks, and smart cars is also creating the next wave of growth for the industry. Keeping up with this dynamism requires new tools that can design, fabricate, and test chips at ever smaller sizes and more complex architectures, creating a dire need for semiconductor capital manufacturing equipment.

The 14 semiconductor manufacturing stocks we track reported a mixed Q1. As a group, revenues missed analysts’ consensus estimates by 0.7% while next quarter’s revenue guidance was 2.9% below.

Luckily, semiconductor manufacturing stocks have performed well with share prices up 18.6% on average since the latest earnings results.

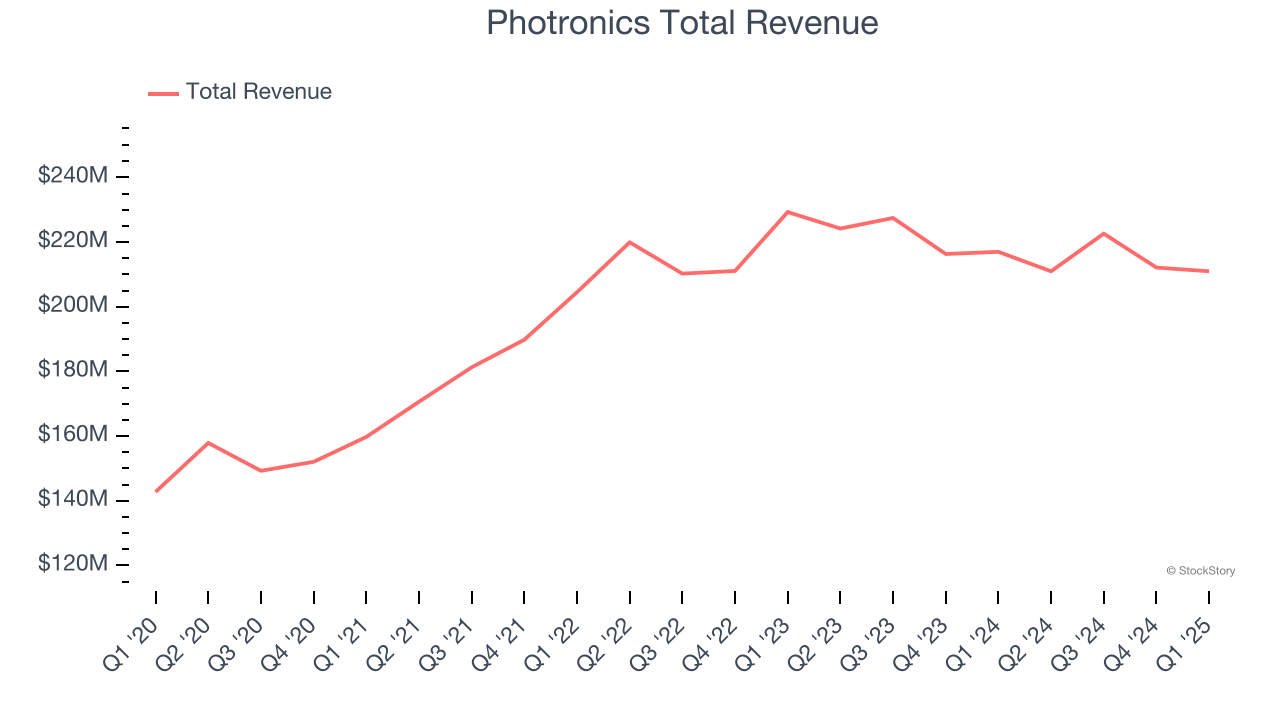

Weakest Q1: Photronics (NASDAQ: PLAB)

Sporting a global footprint of facilities, Photronics (NASDAQ: PLAB) is a manufacturer of photomasks, templates used to transfer patterns onto semiconductor wafers.

Photronics reported revenues of $211 million, down 2.8% year on year. This print was in line with analysts’ expectations, but overall, it was a disappointing quarter for the company with revenue guidance for next quarter missing analysts’ expectations significantly and a significant miss of analysts’ EPS estimates.

“I would like to thank Frank for leading Photronics over the past three years as CEO,” said Mr. Macricostas.

The stock is down 6.6% since reporting and currently trades at $18.75.

Is now the time to buy Photronics? Access our full analysis of the earnings results here, it’s free.

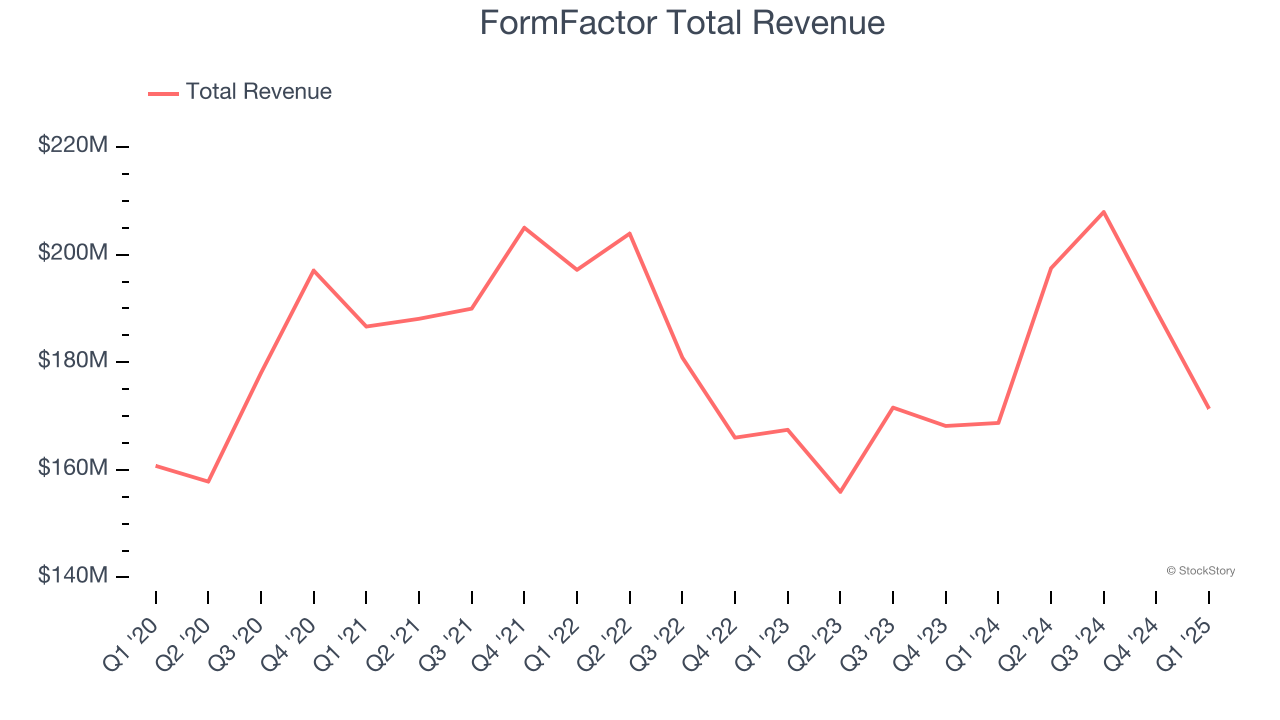

Best Q1: FormFactor (NASDAQ: FORM)

With customers across the foundry and fabless markets, FormFactor (NASDAQ: FORM) is a US-based provider of test and measurement technologies for semiconductors.

FormFactor reported revenues of $171.4 million, up 1.6% year on year, outperforming analysts’ expectations by 0.9%. The business had a strong quarter with a solid beat of analysts’ EPS estimates and an impressive beat of analysts’ adjusted operating income estimates.

The market seems happy with the results as the stock is up 21.9% since reporting. It currently trades at $34.22.

Is now the time to buy FormFactor? Access our full analysis of the earnings results here, it’s free.

Amtech (NASDAQ: ASYS)

Focusing on the silicon carbide and power semiconductor sectors, Amtech Systems (NASDAQ: ASYS) produces the machinery and related chemicals needed for manufacturing semiconductors.

Amtech reported revenues of $15.58 million, down 38.7% year on year, falling short of analysts’ expectations by 15.8%. It was a disappointing quarter as it posted revenue guidance for next quarter missing analysts’ expectations significantly and a significant miss of analysts’ EPS estimates.

Amtech delivered the weakest performance against analyst estimates and slowest revenue growth in the group. Interestingly, the stock is up 39.6% since the results and currently trades at $4.69.

Read our full analysis of Amtech’s results here.

Nova (NASDAQ: NVMI)

Headquartered in Israel, Nova (NASDAQ: NVMI) is a provider of quality control systems used in semiconductor manufacturing.

Nova reported revenues of $213.4 million, up 50.5% year on year. This number topped analysts’ expectations by 1.2%. It was a strong quarter as it also put up an impressive beat of analysts’ adjusted operating income estimates and a solid beat of analysts’ EPS estimates.

The stock is up 32.8% since reporting and currently trades at $267.66.

Read our full, actionable report on Nova here, it’s free.

Amkor (NASDAQ: AMKR)

Operating through a largely Asian facility footprint, Amkor Technologies (NASDAQ: AMKR) provides outsourced packaging and testing for semiconductors.

Amkor reported revenues of $1.32 billion, down 3.2% year on year. This print surpassed analysts’ expectations by 3%. Overall, it was a strong quarter as it also recorded an impressive beat of analysts’ adjusted operating income estimates and a solid beat of analysts’ EPS estimates.

Amkor delivered the biggest analyst estimates beat among its peers. The stock is up 21.9% since reporting and currently trades at $21.30.

Read our full, actionable report on Amkor here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

More News

View More

Recent Quotes

View MoreQuotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.