Financial News

Q4 Earnings Highs And Lows: Sanmina (NASDAQ:SANM) Vs The Rest Of The Electrical Systems Stocks

Looking back on electrical systems stocks’ Q4 earnings, we examine this quarter’s best and worst performers, including Sanmina (NASDAQ: SANM) and its peers.

Like many equipment and component manufacturers, electrical systems companies are buoyed by secular trends such as connectivity and industrial automation. More specific pockets of strong demand include Internet of Things (IoT) connectivity and the 5G telecom upgrade cycle, which can benefit companies whose cables and conduits fit those needs. But like the broader industrials sector, these companies are also at the whim of economic cycles. Interest rates, for example, can greatly impact projects that drive demand for these products.

The 13 electrical systems stocks we track reported a slower Q4. As a group, revenues were in line with analysts’ consensus estimates while next quarter’s revenue guidance was 6.1% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 20.3% since the latest earnings results.

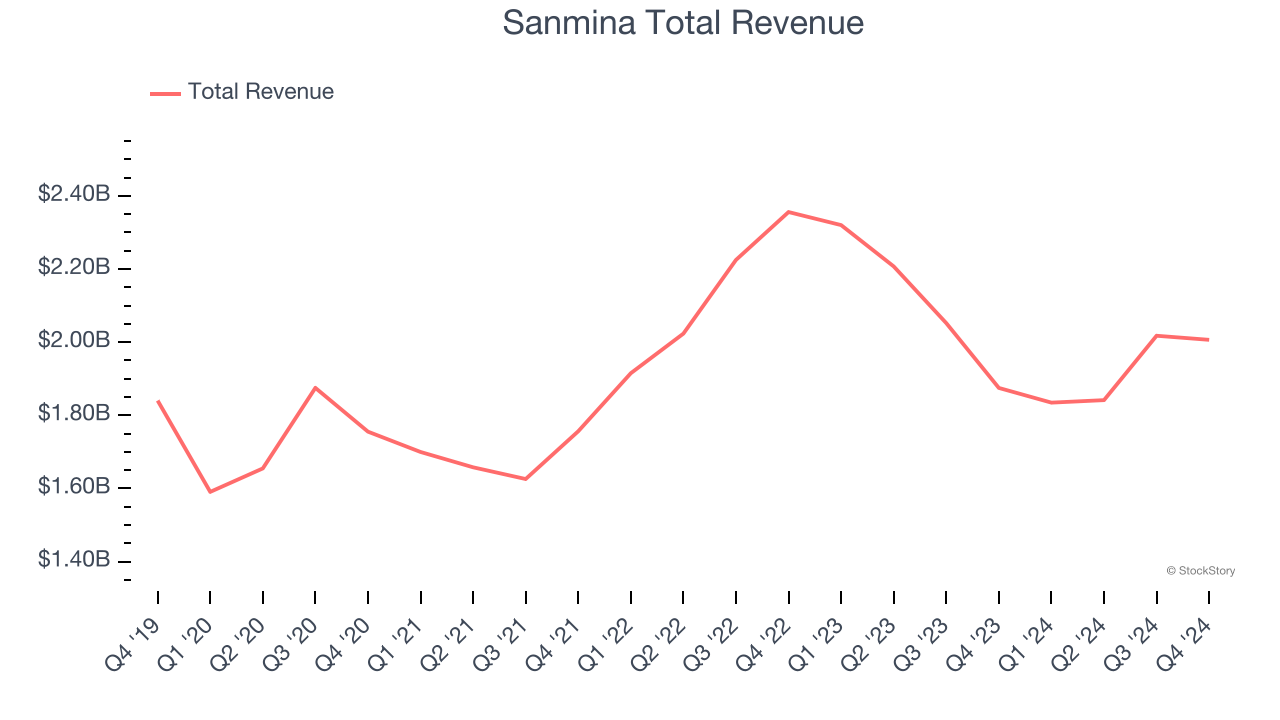

Sanmina (NASDAQ: SANM)

Founded in 1980, Sanmina (NASDAQ: SANM) is an electronics manufacturing services company offering end-to-end solutions for various industries.

Sanmina reported revenues of $2.01 billion, up 7% year on year. This print exceeded analysts’ expectations by 1.5%. Despite the top-line beat, it was still a mixed quarter for the company with a decent beat of analysts’ EPS estimates but EPS guidance for next quarter missing analysts’ expectations significantly.

"We delivered solid first quarter financial results, with revenue towards the high end and non-GAAP earnings per share exceeding our outlook. We continue to execute well, as evident in our consistent operating margin and cash generation," stated Jure Sola, Chairman and Chief Executive Officer of Sanmina Corporation.

The market was likely pricing in the results, and the stock is flat since reporting. It currently trades at $78.42.

Read our full report on Sanmina here, it’s free.

Best Q4: LSI (NASDAQ: LYTS)

Enhancing commercial environments, LSI (NASDAQ: LYTS) provides lighting and display solutions for businesses and retailers.

LSI reported revenues of $147.7 million, up 35.5% year on year, outperforming analysts’ expectations by 14.3%. The business had an incredible quarter with a solid beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

LSI achieved the biggest analyst estimates beat and fastest revenue growth among its peers. The stock is down 10.7% since reporting. It currently trades at $17.69.

Is now the time to buy LSI? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Methode Electronics (NYSE: MEI)

Founded in 1946, Methode Electronics (NYSE: MEI) is a global supplier of custom-engineered solutions for Original Equipment Manufacturers (OEMs).

Methode Electronics reported revenues of $239.9 million, down 7.6% year on year, falling short of analysts’ expectations by 8.9%. It was a disappointing quarter as it posted revenue guidance for next quarter missing analysts’ expectations.

Methode Electronics delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 48% since the results and currently trades at $5.11.

Read our full analysis of Methode Electronics’s results here.

Powell (NASDAQ: POWL)

Originally a metal-working shop supporting local petrochemical facilities, Powell (NYSE: POWL) has grown from a small Houston manufacturer to a global provider of electrical systems.

Powell reported revenues of $241.4 million, up 24.4% year on year. This number topped analysts’ expectations by 3.8%. Taking a step back, it was a satisfactory quarter as it also produced a decent beat of analysts’ EPS estimates but a significant miss of analysts’ EBITDA estimates.

The stock is down 28% since reporting and currently trades at $176.11.

Read our full, actionable report on Powell here, it’s free.

Kimball Electronics (NASDAQ: KE)

Founded in 1961, Kimball Electronics (NYSE: KE) is a global contract manufacturer specializing in electronics and manufacturing solutions for automotive, medical, and industrial markets.

Kimball Electronics reported revenues of $357.4 million, down 15.2% year on year. This print missed analysts’ expectations by 0.7%. Overall, it was a softer quarter as it also recorded full-year revenue guidance missing analysts’ expectations and a significant miss of analysts’ EBITDA estimates.

Kimball Electronics had the weakest full-year guidance update among its peers. The stock is down 24.1% since reporting and currently trades at $13.57.

Read our full, actionable report on Kimball Electronics here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.

More News

View More

Recent Quotes

View MoreQuotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.