Financial News

3 Reasons to Sell BURL and 1 Stock to Buy Instead

Over the last six months, Burlington’s shares have sunk to $243.51, producing a disappointing 10.4% loss - a stark contrast to the S&P 500’s 8.9% gain. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Is now the time to buy Burlington, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Even though the stock has become cheaper, we're sitting this one out for now. Here are three reasons why we avoid BURL and a stock we'd rather own.

Why Is Burlington Not Exciting?

Founded in 1972 as a discount coat and outerwear retailer, Burlington Stores (NYSE: BURL) is now an off-price retailer that has broadened into general apparel, footwear, and home goods.

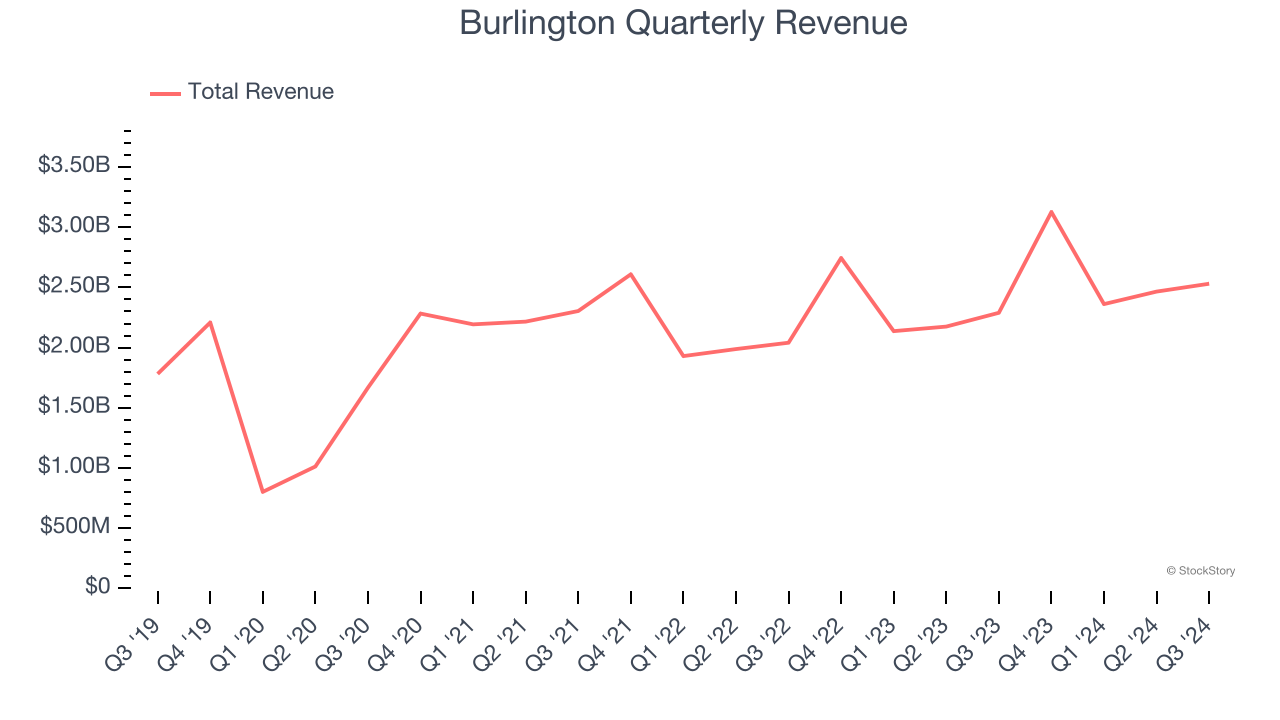

1. Long-Term Revenue Growth Disappoints

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Burlington grew its sales at a mediocre 8.2% compounded annual growth rate. This was below our standard for the consumer retail sector.

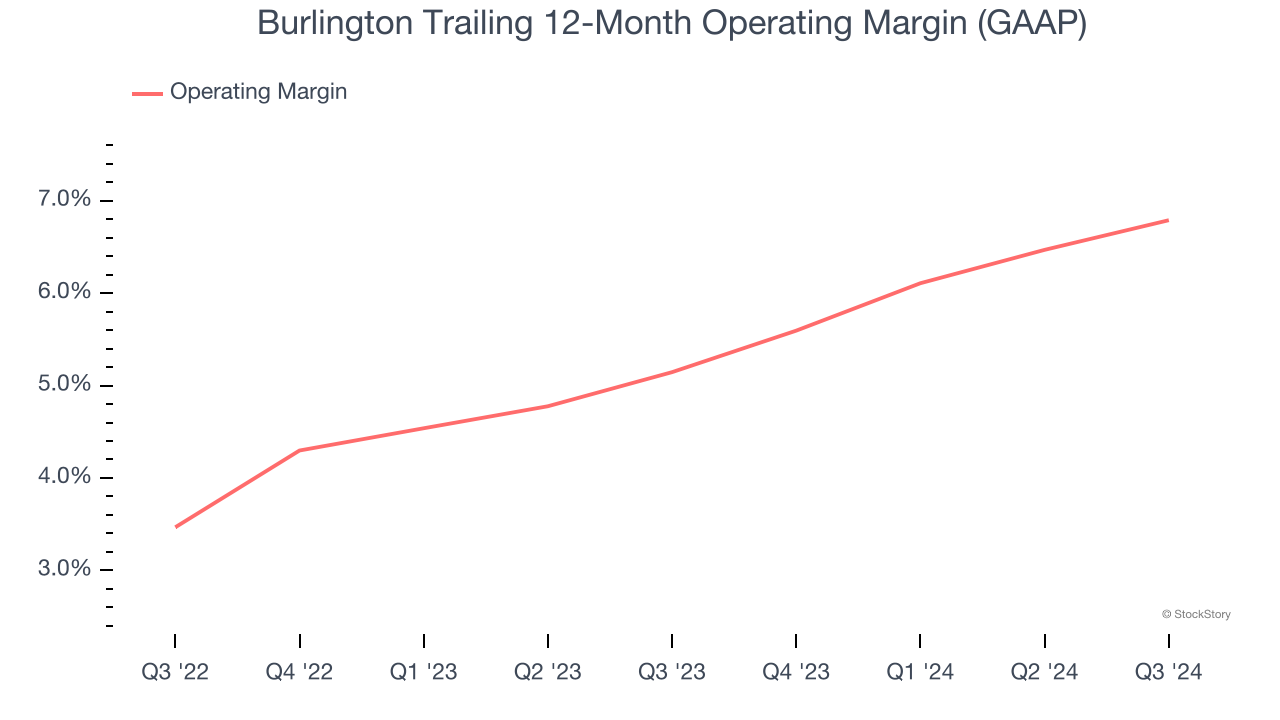

2. Weak Operating Margin Could Cause Trouble

Operating margin is a key profitability metric because it accounts for all expenses keeping the lights on, including wages, rent, advertising, and other administrative costs.

Burlington was profitable over the last two years but held back by its large cost base. Its average operating margin of 6% was weak for a consumer retail business. This result is surprising given its high gross margin as a starting point.

3. Previous Growth Initiatives Haven’t Paid Off Yet

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Burlington historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 6.5%, somewhat low compared to the best consumer retail companies that consistently pump out 25%+.

Final Judgment

Burlington isn’t a terrible business, but it isn’t one of our picks. After the recent drawdown, the stock trades at 27.1× forward price-to-earnings (or $243.51 per share). Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're fairly confident there are better stocks to buy right now. We’d recommend looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Like More Than Burlington

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.

More News

View More

Recent Quotes

View More

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.