Financial News

3 Reasons We’re Fans of SentinelOne (S)

SentinelOne trades at $24.61 per share and has stayed right on track with the overall market, gaining 16% over the last six months. At the same time, the S&P 500 has returned 13.2%.

Is S a buy right now? Find out in our full research report, it’s free.

Why Is SentinelOne a Good Business?

With roots in the Israeli cyber intelligence community, SentinelOne (NYSE: S) provides software to help organizations efficiently detect, prevent, and investigate cyber attacks.

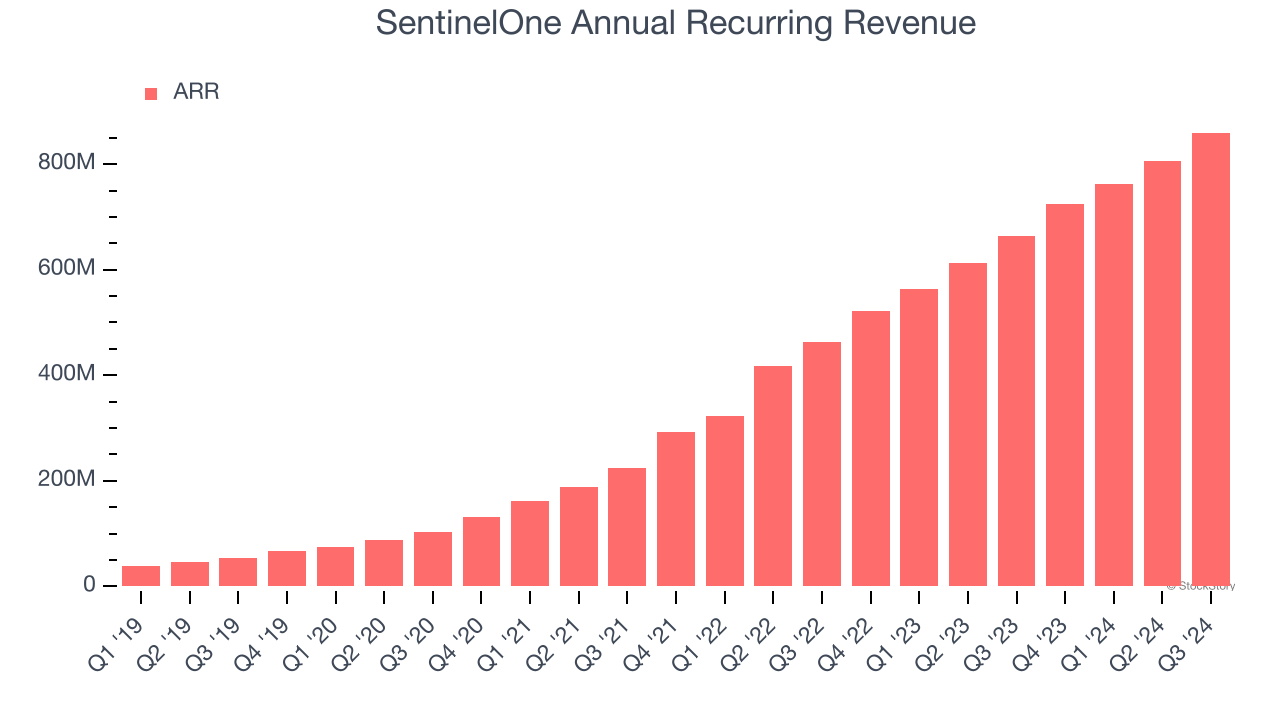

1. ARR Surges as Recurring Revenue Flows In

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

SentinelOne’s ARR punched in at $859.7 million in Q3, and over the last four quarters, its year-on-year growth averaged 33.8%. This performance was fantastic and shows that customers are willing to take multi-year bets on the company’s technology. Its growth also makes SentinelOne a more predictable business, a tailwind for its valuation as investors typically prefer businesses with recurring revenue.

2. Projected Revenue Growth Is Remarkable

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite, though some deceleration is natural as businesses become larger.

Over the next 12 months, sell-side analysts expect SentinelOne’s revenue to rise by 26%. While this projection is below its 65.8% annualized growth rate for the past three years, it is eye-popping and implies the market is baking in success for its products and services.

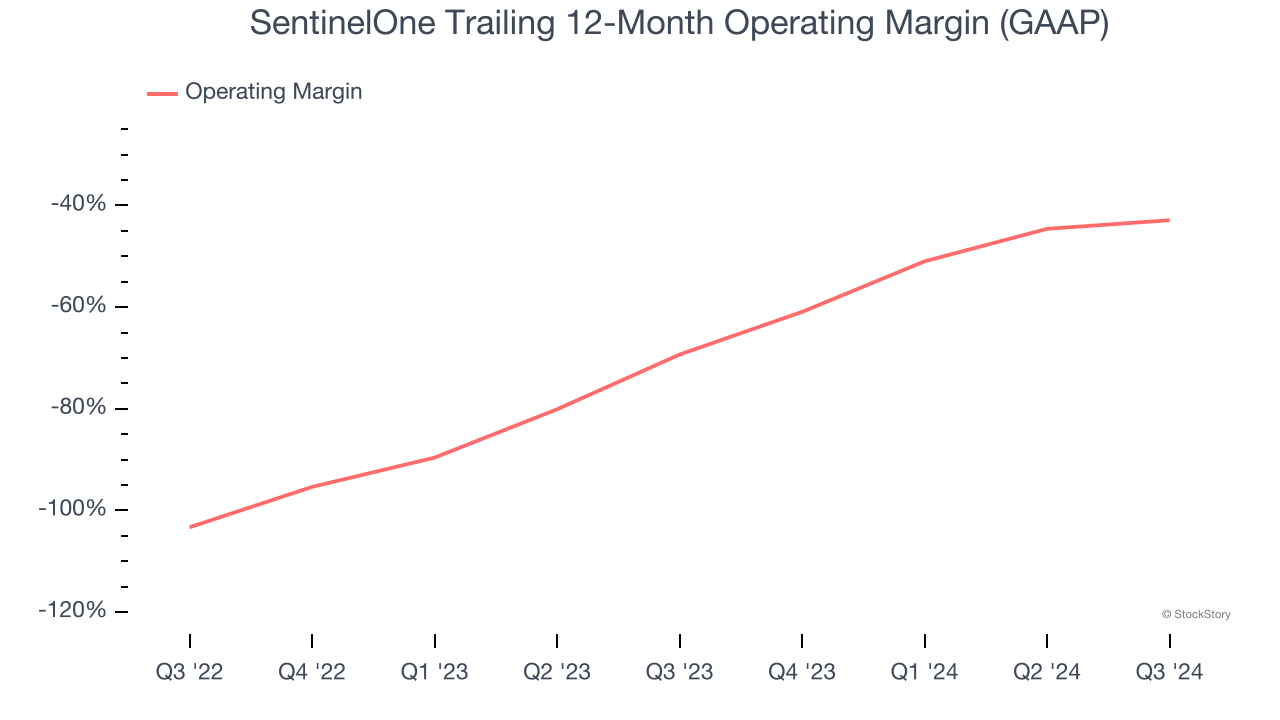

3. Operating Margin Rising, Profits Up

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

Over the last year, SentinelOne’s expanding sales gave it operating leverage as its margin rose by 26.4 percentage points. Although its operating margin for the trailing 12 months was negative 42.9%, we’re confident it can one day reach sustainable profitability.

Final Judgment

These are just a few reasons SentinelOne is a high-quality business worth owning, but at $24.61 per share (or 8× forward price-to-sales), is now the right time to buy the stock? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than SentinelOne

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.

More News

View More

Recent Quotes

View MoreQuotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.