Financial News

3 Reasons to Sell NOVT and 1 Stock to Buy Instead

Over the past six months, Novanta’s stock price fell to $105.42. Shareholders have lost 5% of their capital, which is disappointing considering the S&P 500 has climbed by 27.9%. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Novanta, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free for active Edge members.

Why Is Novanta Not Exciting?

Even though the stock has become cheaper, we don't have much confidence in Novanta. Here are three reasons we avoid NOVT and a stock we'd rather own.

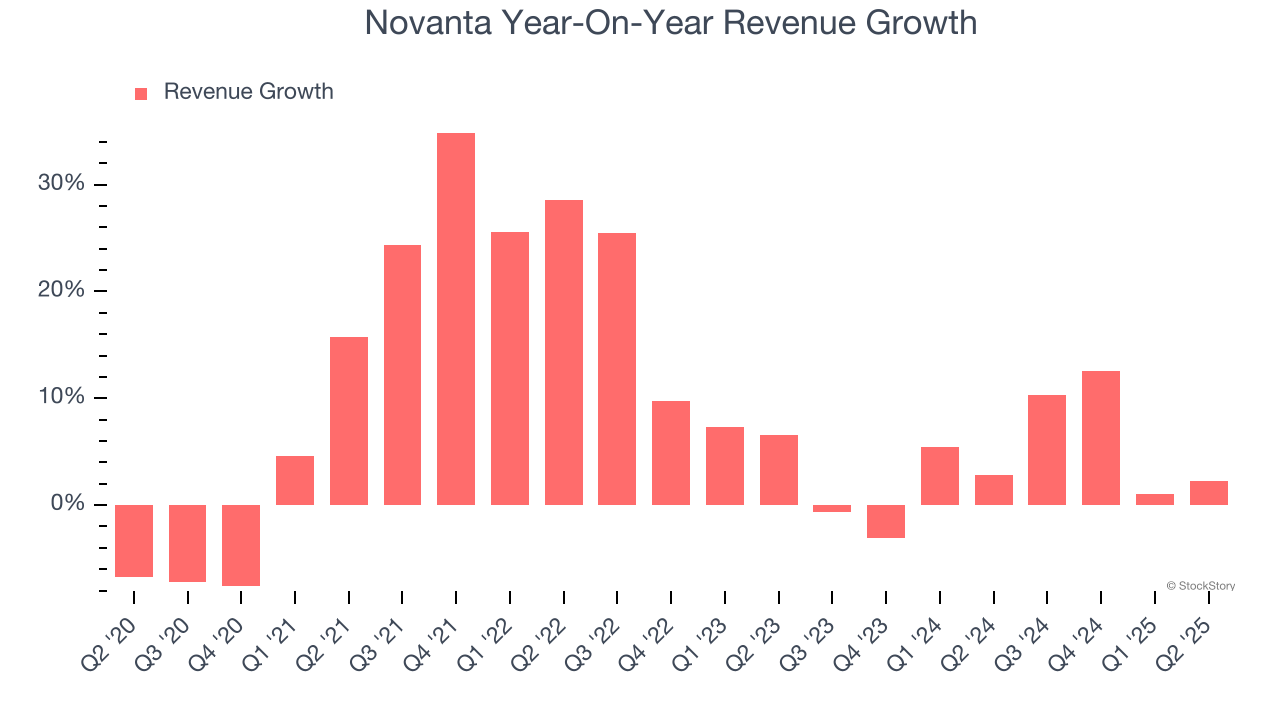

1. Lackluster Revenue Growth

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. Novanta’s recent performance shows its demand has slowed as its annualized revenue growth of 3.7% over the last two years was below its five-year trend. We also note many other Electronic Components businesses have faced declining sales because of cyclical headwinds. While Novanta grew slower than we’d like, it did do better than its peers.

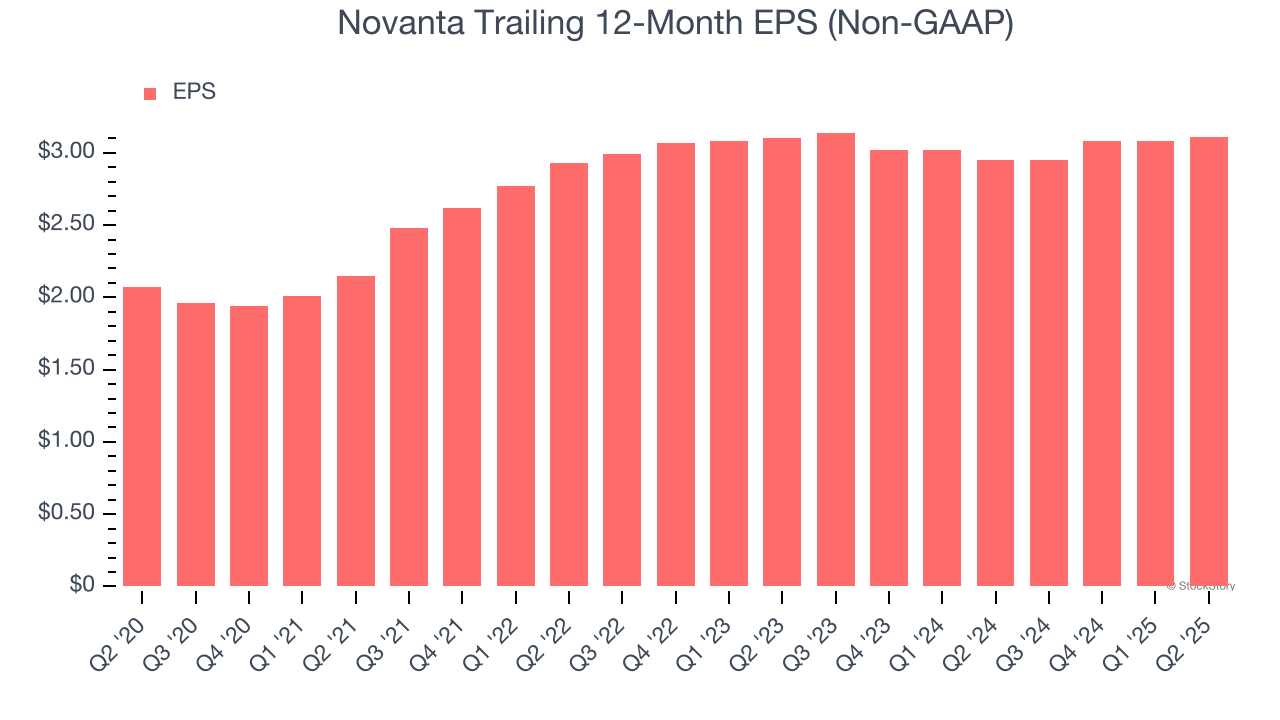

2. EPS Growth Has Stalled Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Novanta’s flat EPS over the last two years was worse than its 3.7% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

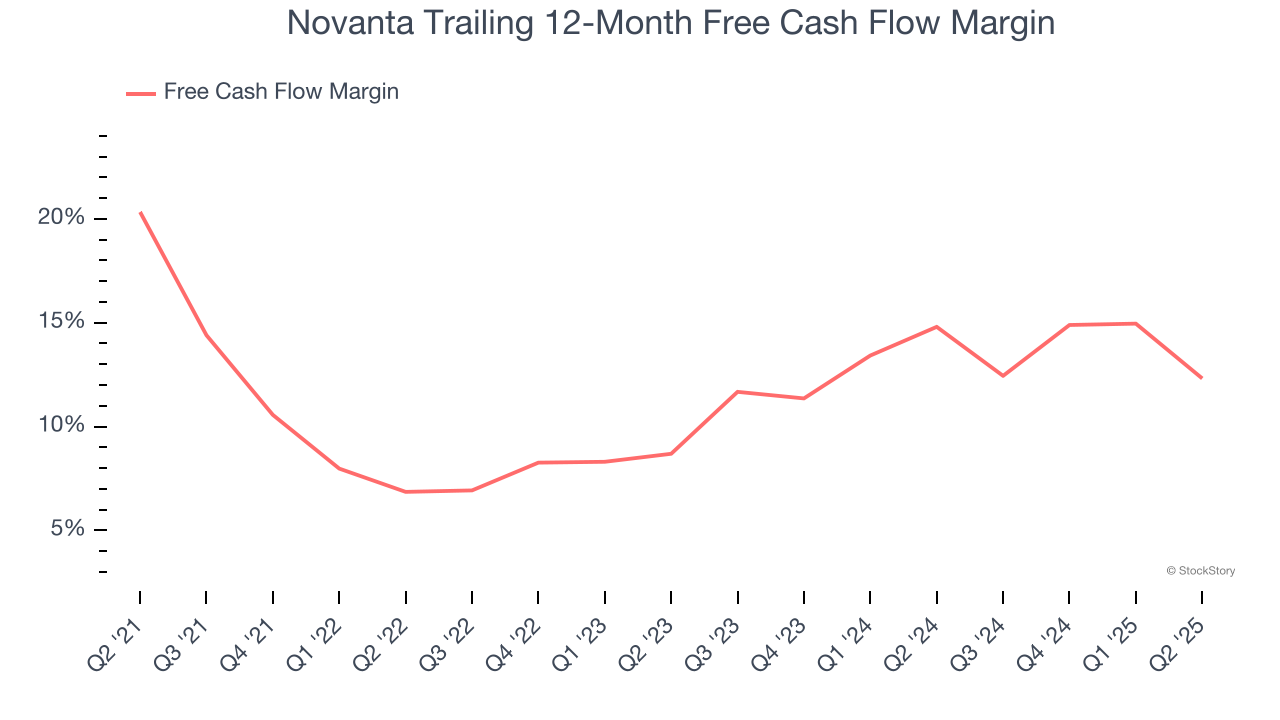

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Novanta’s margin dropped by 8 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Novanta’s free cash flow margin for the trailing 12 months was 12.3%.

Final Judgment

Novanta isn’t a terrible business, but it isn’t one of our picks. Following the recent decline, the stock trades at 30.8× forward EV-to-EBITDA (or $105.42 per share). This multiple tells us a lot of good news is priced in - we think other companies feature superior fundamentals at the moment. We’d suggest looking at one of Charlie Munger’s all-time favorite businesses.

Stocks We Like More Than Novanta

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

More News

View More

Recent Quotes

View MoreQuotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.