Financial News

Three Reasons to Avoid GIII and One Stock to Buy Instead

Over the last six months, G-III’s shares have sunk to $29.12, producing a disappointing 6.2% loss - a stark contrast to the S&P 500’s 14% gain. This may have investors wondering how to approach the situation.

Is now the time to buy G-III, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.Even though the stock has become cheaper, we're cautious about G-III. Here are three reasons why there are better opportunities than GIII and a stock we'd rather own.

Why Do We Think G-III Will Underperform?

Founded as a small leather goods business, G-III (NASDAQ: GIII) is a fashion and apparel conglomerate with a diverse portfolio of brands.

1. Long-Term Revenue Growth Flatter Than a Pancake

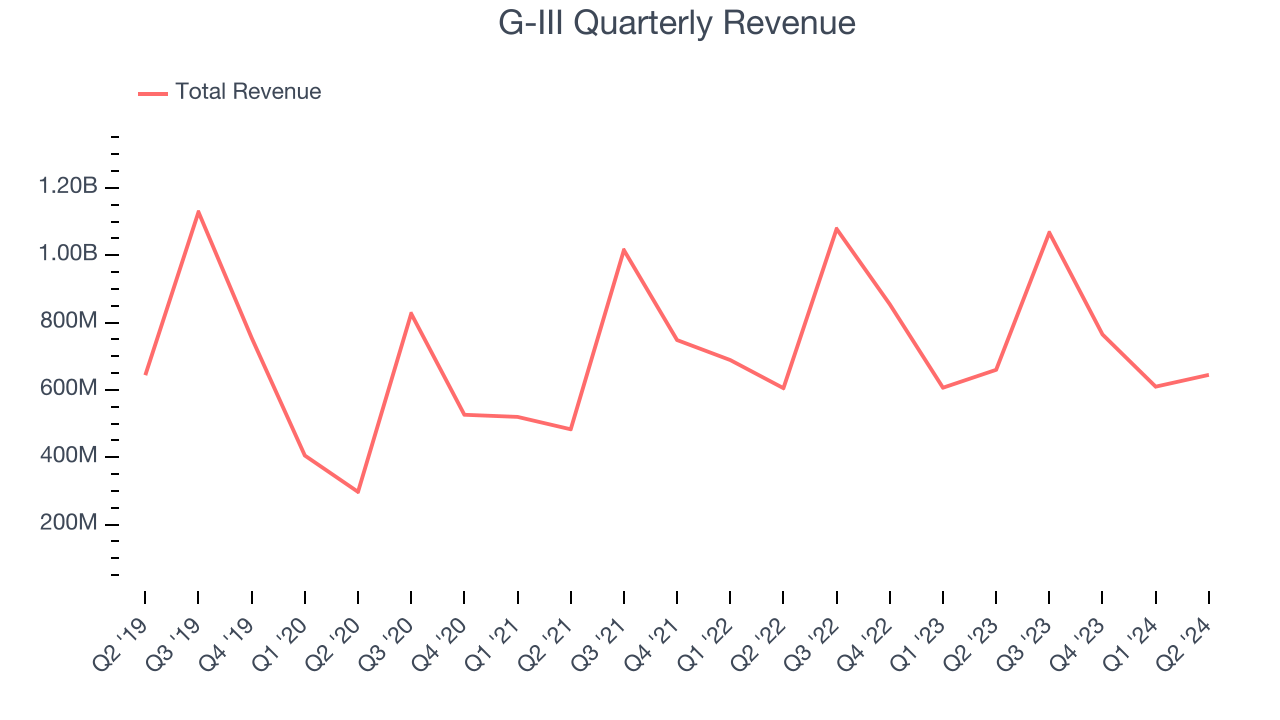

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, G-III struggled to consistently increase demand as its $3.09 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and is a sign of poor business quality.

2. Previous Growth Initiatives Haven’t Paid Off Yet

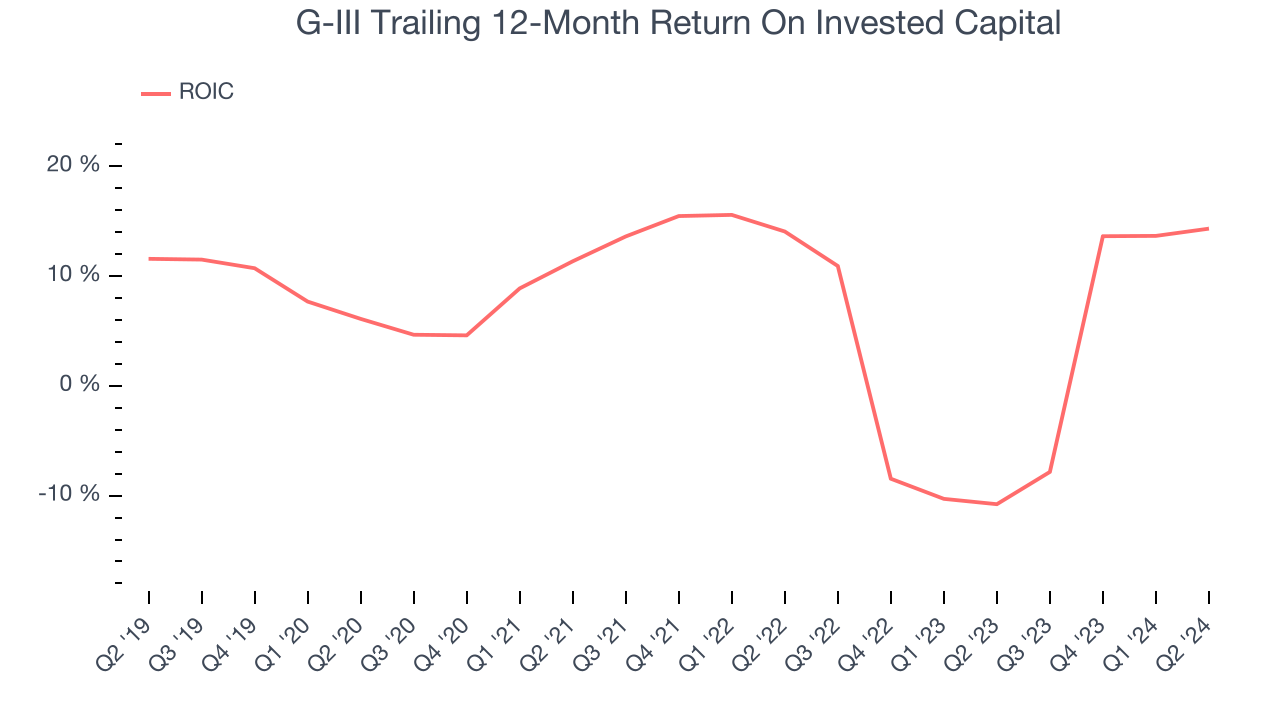

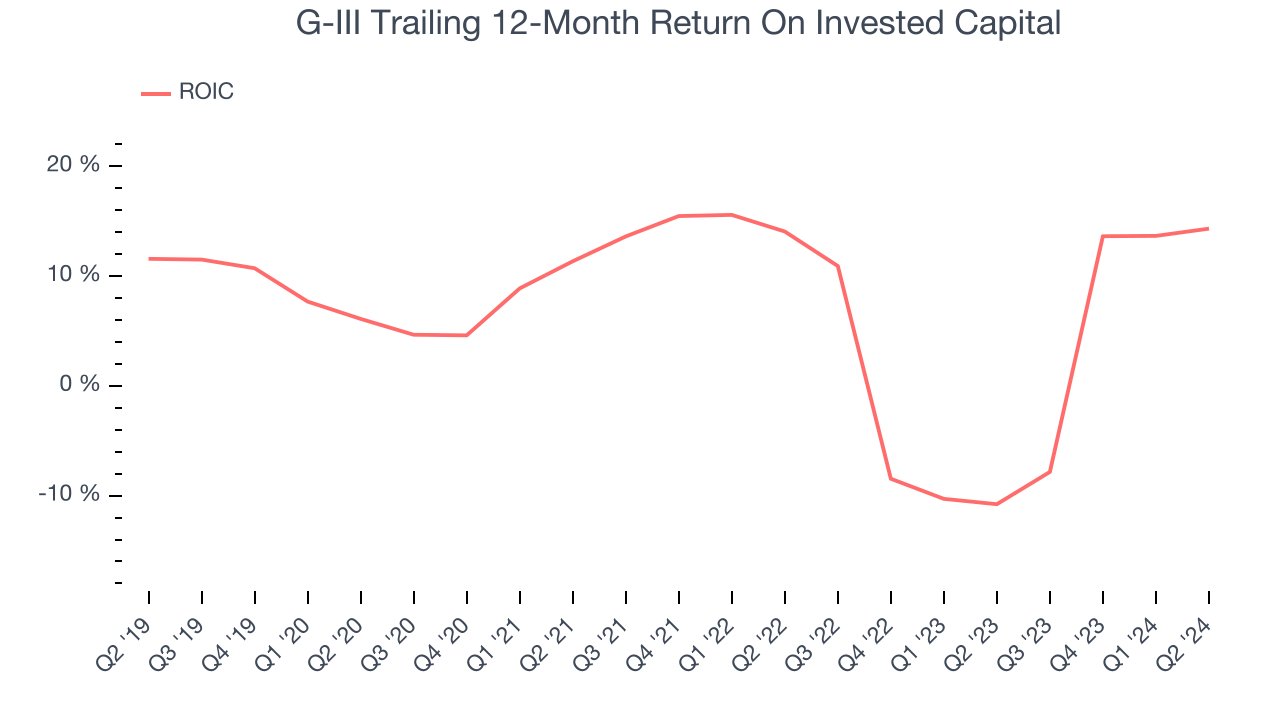

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

G-III’s five-year average ROIC was 7%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+. Its returns suggest it historically did a mediocre job investing in profitable growth initiatives.

3. New Investments Fail to Bear Fruit as ROIC Declines

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We typically prefer to invest in companies with high returns because it means they have viable business models, but the trend in a company’s ROIC is often what surprises the market and moves the stock price. Unfortunately, G-III’s ROIC has decreased over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

Final Judgment

We see the value of companies helping consumers, but in the case of G-III, we’re out. After the recent drawdown, the stock trades at 8.4x forward price-to-earnings (or $29.12 per share). While this valuation is optically cheap, the potential downside is still huge given its shaky fundamentals. There are more exciting stocks to buy at the moment. We’d suggest looking at Yum! Brands, an all-weather company that owns household favorite Taco Bell.

Stocks We Like More Than G-III

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market to cap off the year - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.

More News

View More

Recent Quotes

View More

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.