Financial News

Sealed Air’s (NYSE:SEE) Q3 Earnings Results: Revenue In Line With Expectations

Integrated packaging solutions provider Sealed Air Corporation (NYSE: SEE) met Wall Street’s revenue expectations in Q3 CY2024, but sales fell 2.7% year on year to $1.35 billion. The company’s outlook for the full year was close to analysts’ estimates with revenue guided to $5.4 billion at the midpoint. Its non-GAAP profit of $0.79 per share was 18% above analysts’ consensus estimates.

Is now the time to buy Sealed Air? Find out by accessing our full research report, it’s free.

Sealed Air (SEE) Q3 CY2024 Highlights:

- Revenue: $1.35 billion vs analyst estimates of $1.34 billion (in line)

- Adjusted EPS: $0.79 vs analyst estimates of $0.67 (18% beat)

- EBITDA: $276 million vs analyst estimates of $264.4 million (4.4% beat)

- The company reconfirmed its revenue guidance for the full year of $5.4 billion at the midpoint

- Management raised its full-year Adjusted EPS guidance to $3.05 at the midpoint, a 7% increase

- EBITDA guidance for the full year is $1.1 billion at the midpoint, in line with analyst expectations

- Gross Margin (GAAP): 29.8%, in line with the same quarter last year

- Operating Margin: 13.9%, up from 11.4% in the same quarter last year

- EBITDA Margin: 20.5%, in line with the same quarter last year

- Free Cash Flow Margin: 8.6%, down from 10% in the same quarter last year

- Sales Volumes rose 1% year on year (-5.9% in the same quarter last year)

- Market Capitalization: $5.40 billion

"With the shift into two verticals, Food and Protective, and the onboarding of new leadership, we have positioned Sealed Air for long-term success," said Patrick Kivits, Sealed Air's CEO.

Company Overview

Founded in 1960, Sealed Air Corporation (NYSE: SEE) specializes in the development and production of protective and food packaging solutions, serving a variety of industries.

Industrial Packaging

Industrial packaging companies have built competitive advantages from economies of scale that lead to advantaged purchasing and capital investments that are difficult and expensive to replicate. Recently, eco-friendly packaging and conservation are driving customers preferences and innovation. For example, plastic is not as desirable a material as it once was. Despite being integral to consumer goods ranging from beer to toothpaste to laundry detergent, these companies are still at the whim of the macro, especially consumer health and consumer willingness to spend.

Sales Growth

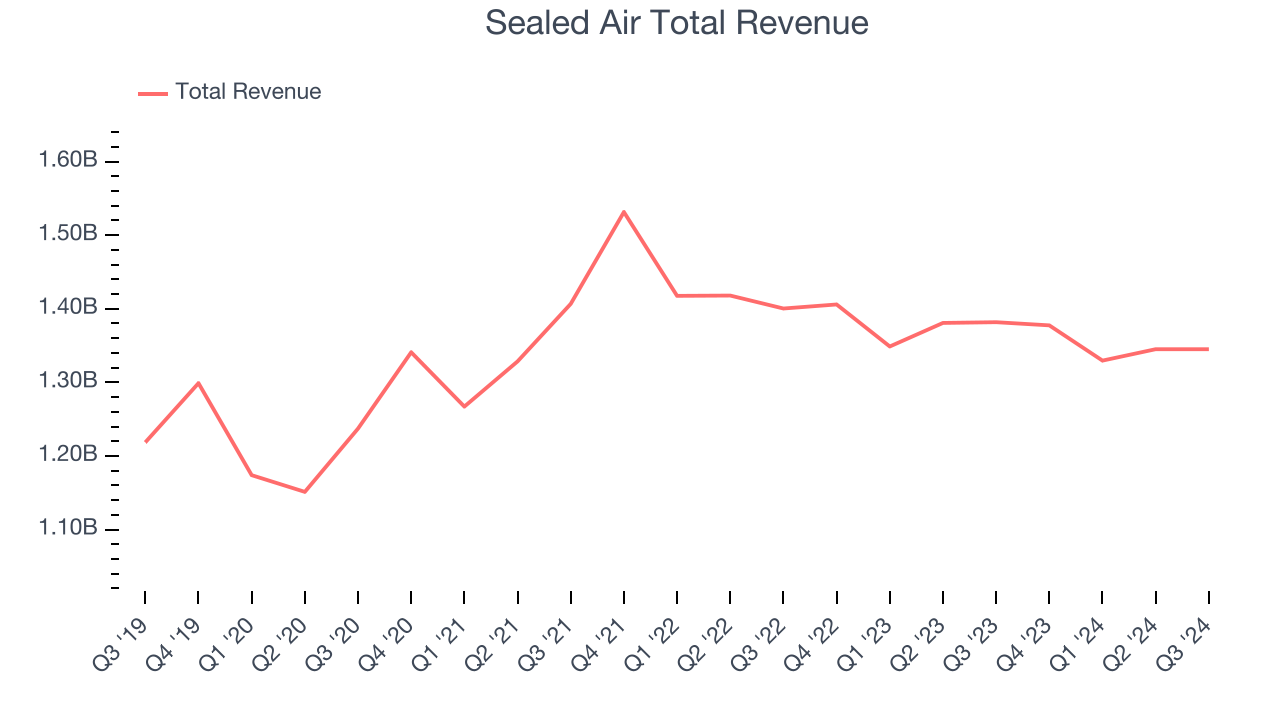

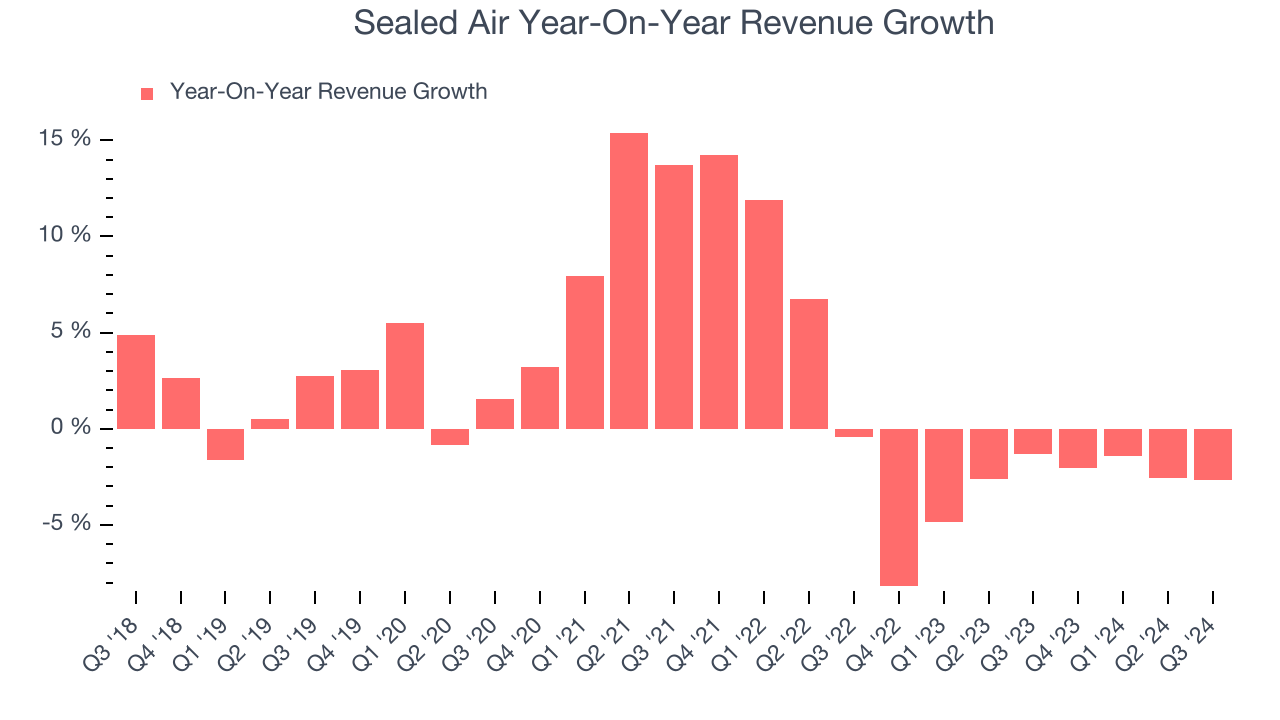

Examining a company’s long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Sealed Air grew its sales at a sluggish 2.6% compounded annual growth rate. This shows it couldn’t expand in any major way, a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Sealed Air’s history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 3.3% annually. Sealed Air isn’t alone in its struggles as the Industrial Packaging industry experienced a cyclical downturn, with many similar businesses seeing lower sales at this time.

We can dig further into the company’s revenue dynamics by analyzing its sales volumes, which show how many products it was moving. Over the last two years, Sealed Air’s sales volumes averaged 4.4% year-on-year declines. Because this number is in line with its revenue growth, we can see the company kept its prices fairly consistent.

This quarter, Sealed Air reported a rather uninspiring 2.7% year-on-year revenue decline to $1.35 billion of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, an improvement versus the last two years. While this projection suggests its newer products and services will fuel better performance, it is still below average for the sector.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

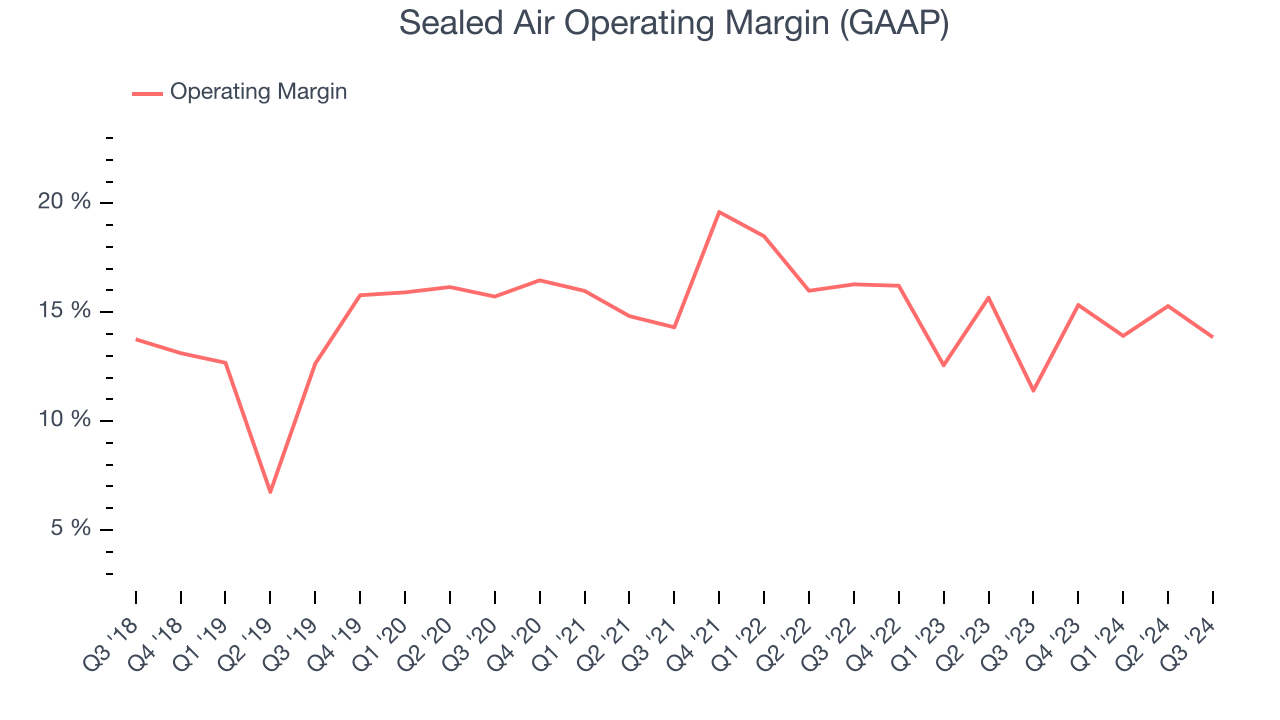

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling them, and, most importantly, keeping them relevant through research and development.

Sealed Air has been an optimally-run company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 15.5%.

Looking at the trend in its profitability, Sealed Air’s annual operating margin decreased by 1.3 percentage points over the last five years. Even though its historical margin is high, shareholders will want to see Sealed Air become more profitable in the future.

This quarter, Sealed Air generated an operating profit margin of 13.9%, up 2.4 percentage points year on year. The increase was encouraging, and since its operating margin rose more than its gross margin, we can infer it was recently more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

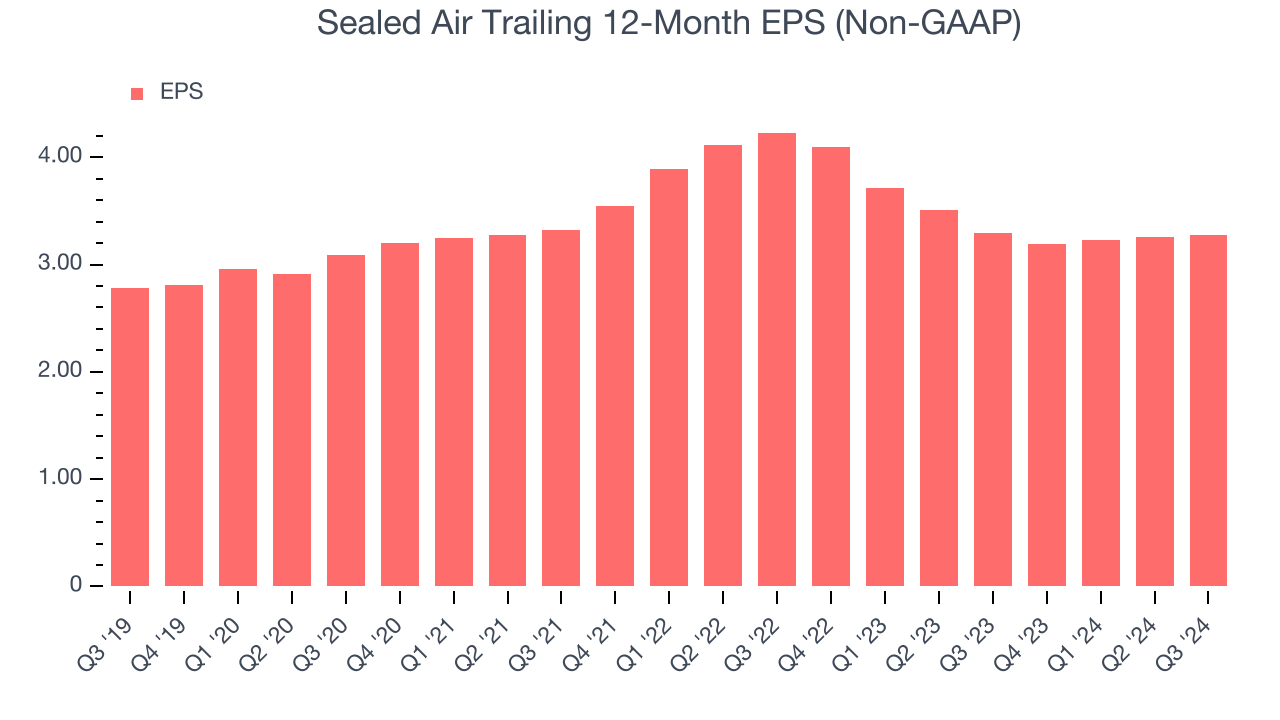

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth was profitable.

Sealed Air’s weak 3.3% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business. Sealed Air’s two-year annual EPS declines of 11.9% were bad and lower than its two-year revenue performance.

In Q3, Sealed Air reported EPS at $0.79, up from $0.77 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Sealed Air’s full-year EPS of $3.28 to shrink by 7.6%.

Key Takeaways from Sealed Air’s Q3 Results

We enjoyed seeing Sealed Air exceed analysts’ EPS and EBITDA expectations this quarter. We were also excited it raised its full-year EPS guidance. Overall, we think this was a good quarter with some key metrics above expectations. The stock traded up 2.5% to $38 immediately following the results.

Sealed Air put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.

More News

View More

Recent Quotes

View More

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.