Financial News

Markforged (NYSE:MKFG) Reports Sales Below Analyst Estimates In Q3 Earnings

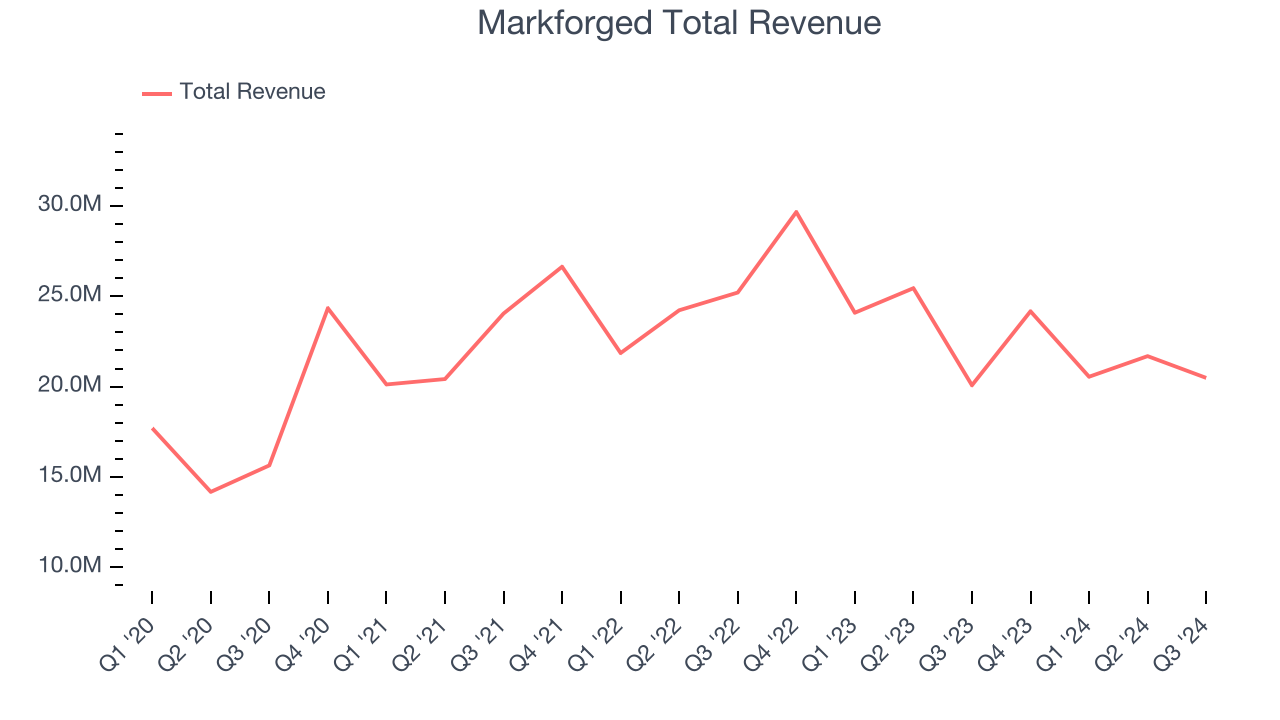

3D printer provider Markforged (NYSE: MKFG) missed Wall Street’s revenue expectations in Q3 CY2024 as sales rose 2% year on year to $20.48 million. Its GAAP loss of $1.15 per share was also 62% below analysts’ consensus estimates.

Is now the time to buy Markforged? Find out by accessing our full research report, it’s free.

Markforged (MKFG) Q3 CY2024 Highlights:

- Revenue: $20.48 million vs analyst estimates of $22.54 million (9.1% miss)

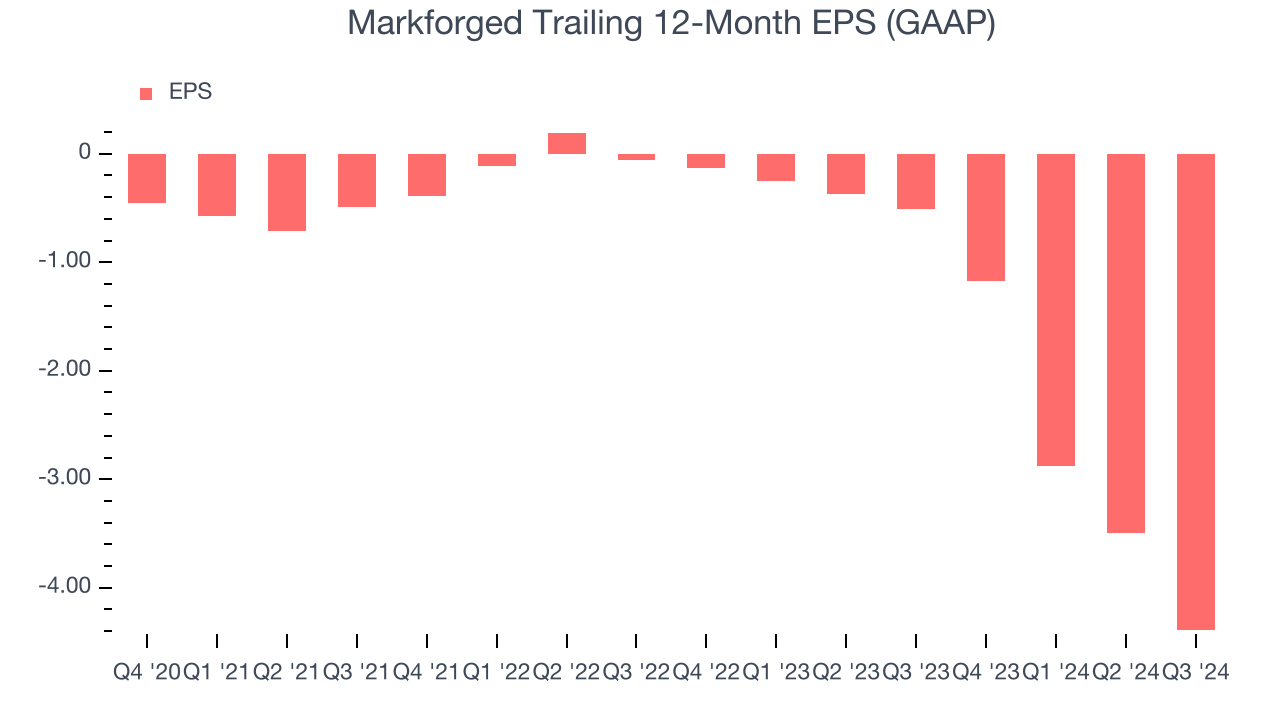

- EPS: -$1.15 vs analyst estimates of -$0.71 (-$0.44 miss)

- Gross Margin (GAAP): 49%, up from 45.7% in the same quarter last year

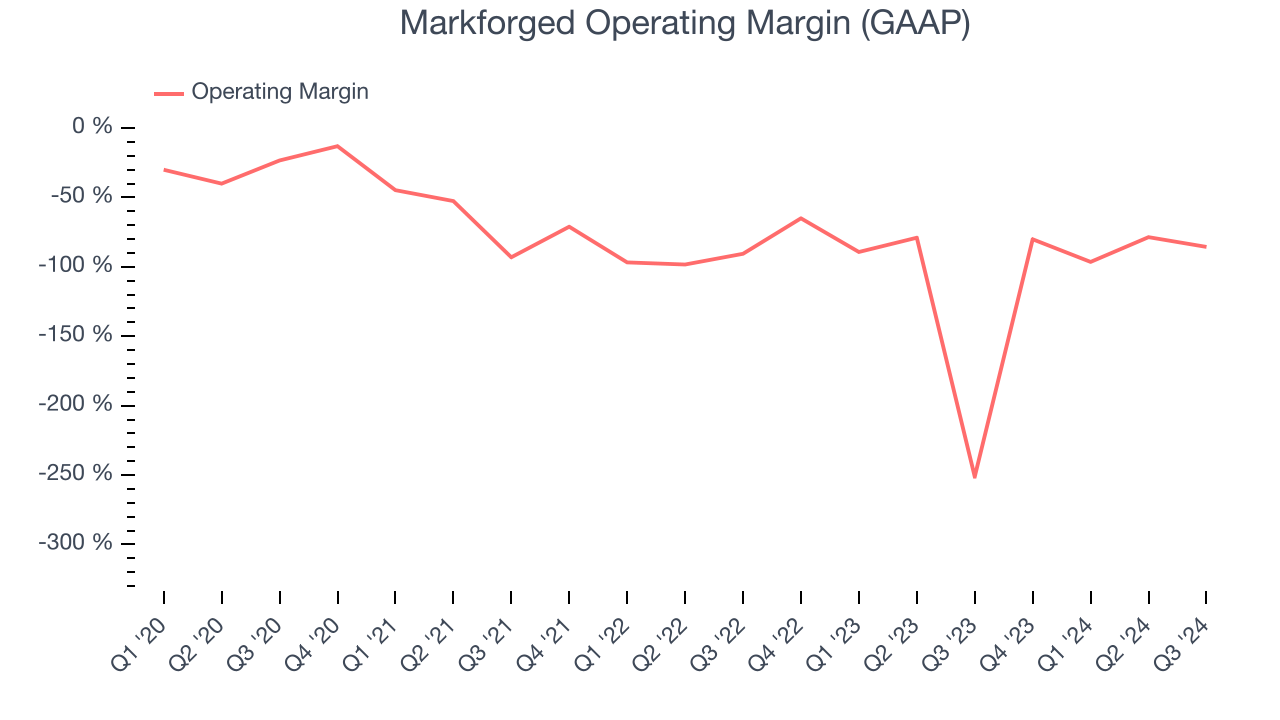

- Operating Margin: -85.6%, up from -251% in the same quarter last year

- Market Capitalization: $90.68 million

“We are pleased with our results in Q3 that were supported by the encouraging adoption of our latest product innovations despite facing a challenging industrial environment,” said Shai Terem, President and CEO of Markforged.

Company Overview

Beginning as a start-up at SolidWorks World–an annual design and engineering conference, Markforged (NYSE: MKFG) offers 3D printers and softwares to manufacturers of various industries.

Custom Parts Manufacturing

Onshoring and inventory management–themes that grew in focus after COVID wreaked havoc on global supply chains–are tailwinds for companies that combine economies of scale with reliable service. Many in the space have adopted 3D printing to efficiently address the need for bespoke parts and components, but all companies are still at the whim of economic cycles. For example, consumer spending and interest rates can greatly impact the industrial production that drives demand for these companies’ offerings.

Sales Growth

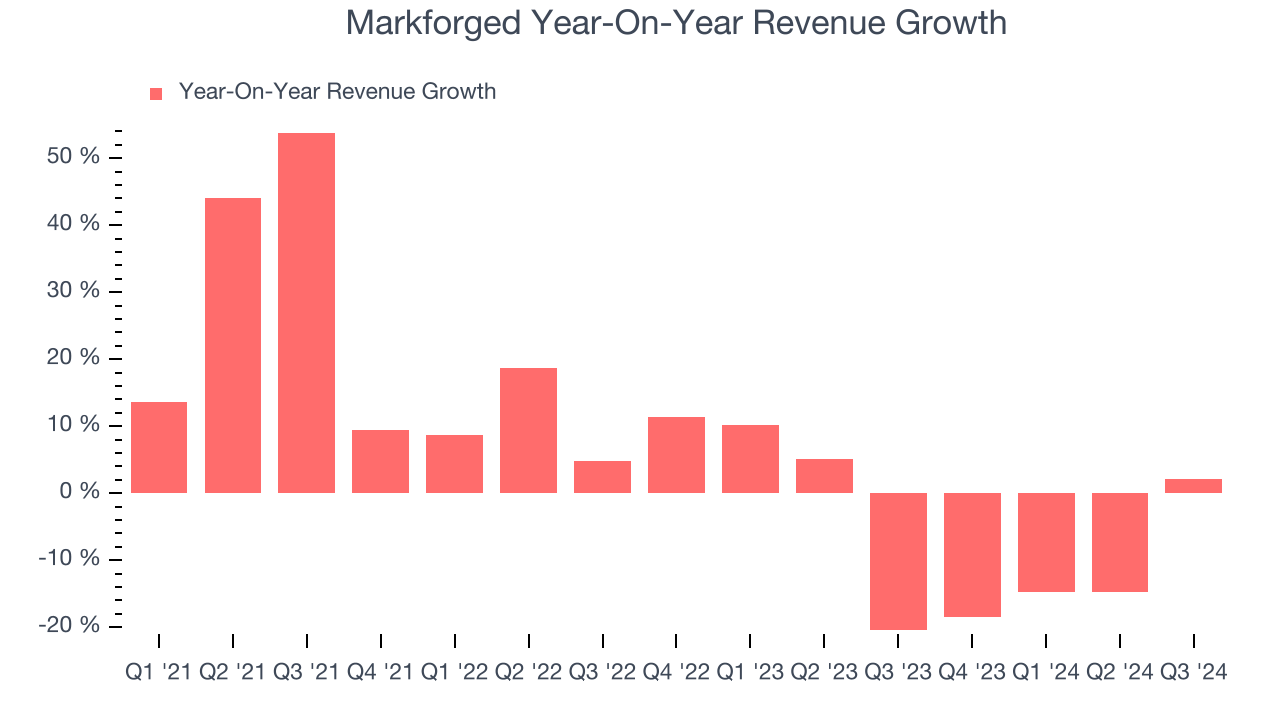

A company’s long-term performance is an indicator of its overall business quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for multiple years. Unfortunately, Markforged’s 7.2% annualized revenue growth over the last four years was mediocre. This shows it couldn’t expand in any major way, a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a stretched historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Markforged’s history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 5.8% annually.

This quarter, Markforged’s revenue grew 2% year on year to $20.48 million, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 10.9% over the next 12 months, an improvement versus the last two years. This projection is commendable and shows the market believes its newer products and services will catalyze higher growth rates.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Markforged’s high expenses have contributed to an average operating margin of negative 78.9% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Looking at the trend in its profitability, Markforged’s annual operating margin decreased by 55.9 percentage points over the last five years. The company’s performance was poor no matter how you look at it. It shows operating expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Markforged generated a negative 85.6% operating margin. The company's lacking profits are certainly concerning.

Earnings Per Share

Analyzing revenue trends tells us about a company’s historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Markforged’s earnings losses deepened over the last four years as its EPS dropped 77.4% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Markforged’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Markforged, its two-year annual EPS declines of 754% show it’s continued to underperform. These results were bad no matter how you slice the data.In Q3, Markforged reported EPS at negative $1.15, down from negative $0.26 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Markforged to improve its earnings losses. Analysts forecast its full-year EPS of negative $4.38 will advance to negative $2.08.

Key Takeaways from Markforged’s Q3 Results

We struggled to find many strong positives in these results. Its revenue missed and its EPS fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 2.8% to $4.34 immediately after reporting.

Markforged may have had a tough quarter, but does that actually create an opportunity to invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

More News

View More

Recent Quotes

View MoreQuotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.