Financial News

Kimball Electronics’s (NASDAQ:KE) Q3 Earnings Results: Revenue In Line With Expectations

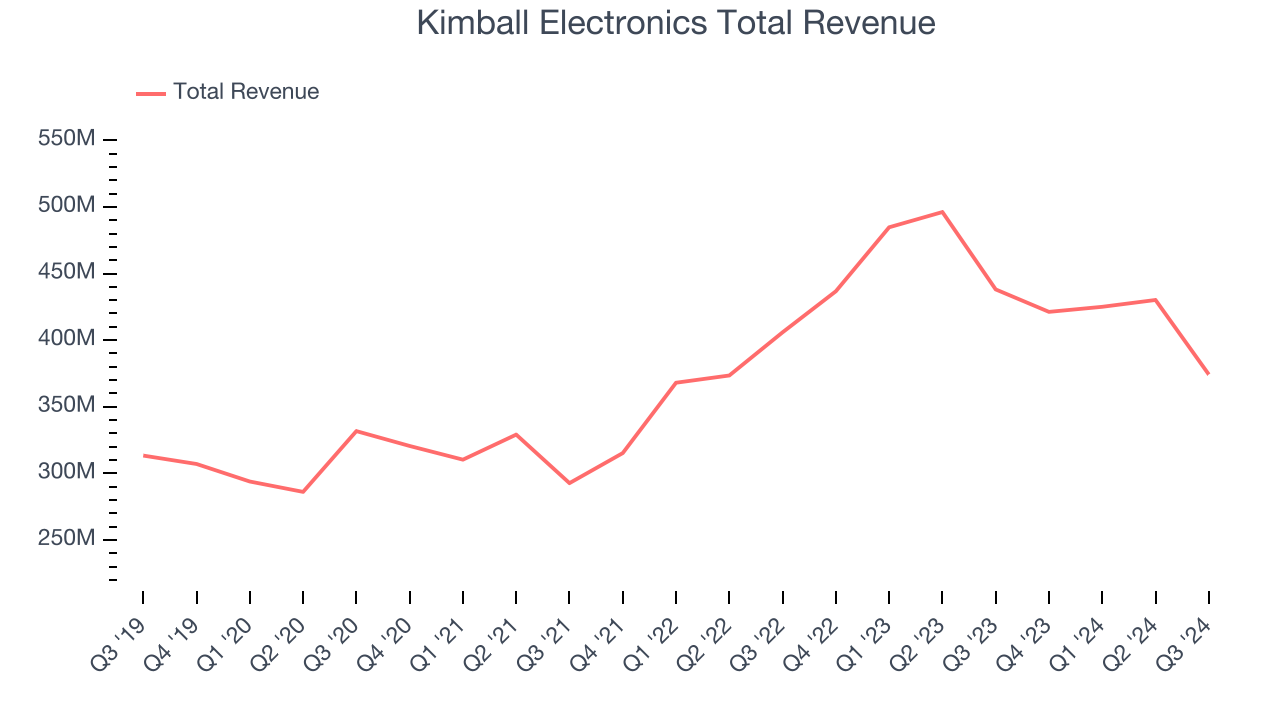

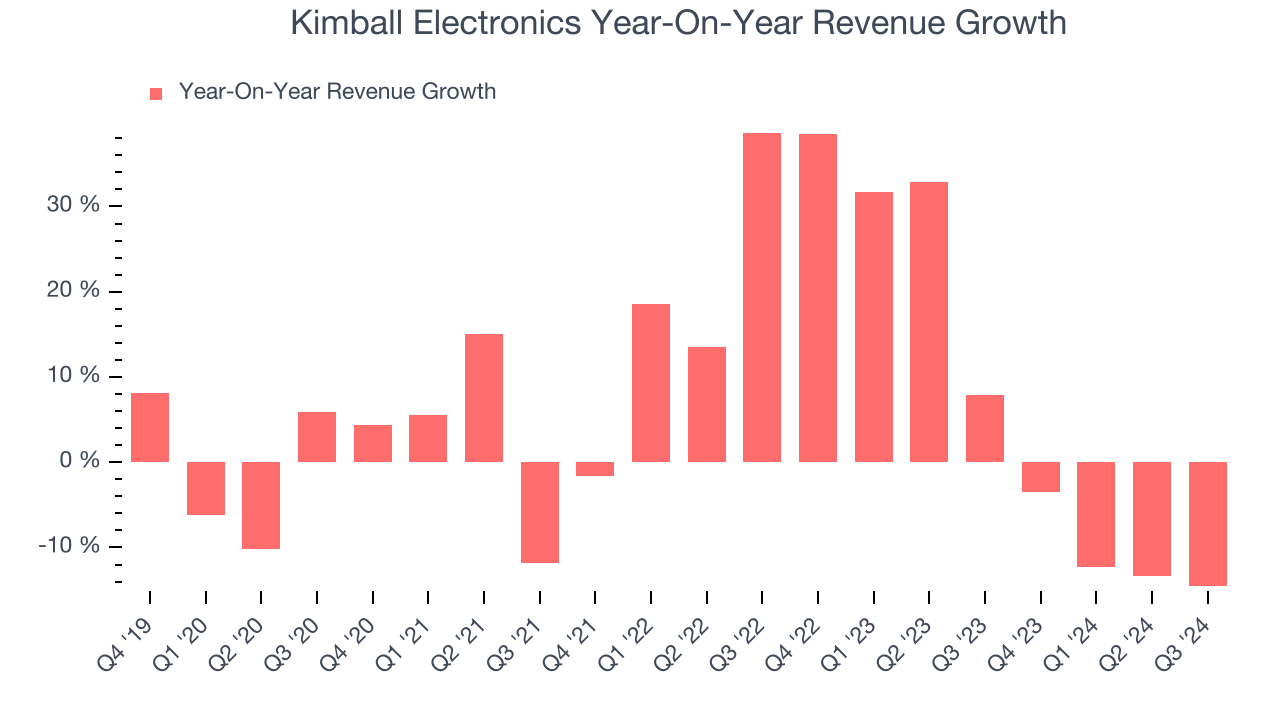

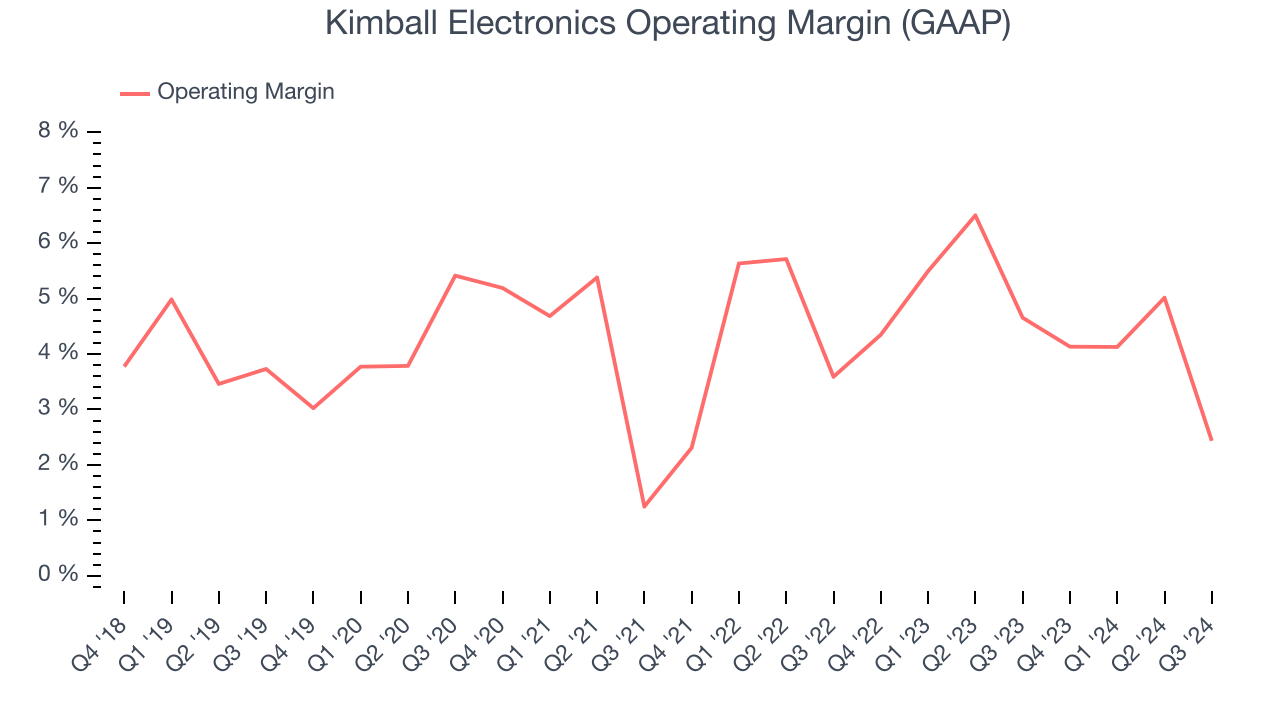

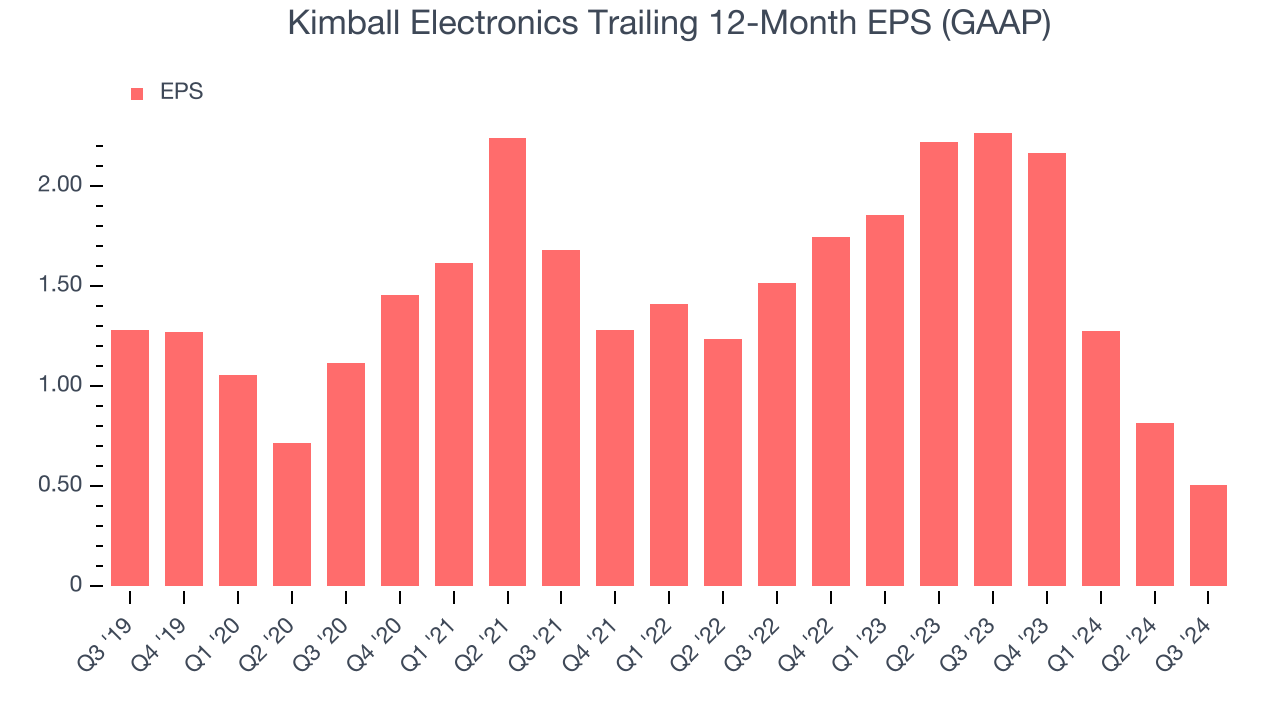

Global electronics contract manufacturer Kimball Electronics (NYSE: KE) met Wall Street’s revenue expectations in Q3 CY2024, but sales fell 14.6% year on year to $374.3 million. The company’s outlook for the full year was close to analysts’ estimates with revenue guided to $1.49 billion at the midpoint. Its GAAP profit of $0.12 per share was 46.7% below analysts’ consensus estimates.

Is now the time to buy Kimball Electronics? Find out by accessing our full research report, it’s free.

Kimball Electronics (KE) Q3 CY2024 Highlights:

- Revenue: $374.3 million vs analyst estimates of $374.8 million (in line)

- EPS: $0.12 vs analyst expectations of $0.23 (46.7% miss)

- EBITDA: $16.24 million vs analyst estimates of $24.16 million (32.8% miss)

- The company reconfirmed its revenue guidance for the full year of $1.49 billion at the midpoint

- The company reconfirmed its adjusted operating margin for the full year of 4.25% at the midpoint

- Gross Margin (GAAP): 6.3%, down from 8.1% in the same quarter last year

- Operating Margin: 2.4%, down from 4.7% in the same quarter last year

- EBITDA Margin: 4.3%, down from 6.9% in the same quarter last year

- Free Cash Flow Margin: 12.2%, up from 0.4% in the same quarter last year

- Market Capitalization: $449.9 million

Commenting on today’s announcement, Richard D. Phillips, Chief Executive Officer, stated, “Q1 represents another chapter of ‘controlling what we can control’ while navigating the challenging operating environment stemming from sustained end market weakness. Our results for the quarter were in line with expectations, considering the difficult comparisons from a record-setting Q1 last year. We continue to adjust costs, improve working capital management, and generate positive cash flow used to pay down debt. We made meaningful progress in the quarter with debt levels at a 2-year low, a result of the cash generated from operating activities and the proceeds from the disposition of the Automation, Test, and Measurement business, with its divestiture closing in July.”

Company Overview

Founded in 1961, Kimball Electronics (NYSE: KE) is a global contract manufacturer specializing in electronics and manufacturing solutions for automotive, medical, and industrial markets.

Electrical Systems

Like many equipment and component manufacturers, electrical systems companies are buoyed by secular trends such as connectivity and industrial automation. More specific pockets of strong demand include Internet of Things (IoT) connectivity and the 5G telecom upgrade cycle, which can benefit companies whose cables and conduits fit those needs. But like the broader industrials sector, these companies are also at the whim of economic cycles. Interest rates, for example, can greatly impact projects that drive demand for these products.

Sales Growth

A company’s long-term performance can indicate its business quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, Kimball Electronics’s sales grew at a mediocre 6.1% compounded annual growth rate over the last five years. This shows it couldn’t expand in any major way, a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Kimball Electronics’s annualized revenue growth of 6.2% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, Kimball Electronics reported a rather uninspiring 14.6% year-on-year revenue decline to $374.3 million of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to decline 10.2% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and shows the market thinks its products and services will see some demand headwinds.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Kimball Electronics was profitable over the last five years but held back by its large cost base. Its average operating margin of 4.4% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Analyzing the trend in its profitability, Kimball Electronics’s annual operating margin might have seen some fluctuations but has generally stayed the same over the last five years, which doesn’t help its cause.

In Q3, Kimball Electronics generated an operating profit margin of 2.4%, down 2.2 percentage points year on year. Since Kimball Electronics’s operating margin decreased more than its gross margin, we can assume it was recently less efficient because expenses such as marketing, R&D, and administrative overhead increased.

Earnings Per Share

Analyzing revenue trends tells us about a company’s historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Kimball Electronics, its EPS declined by 16.9% annually over the last five years while its revenue grew by 6.1%. However, its operating margin didn’t change during this timeframe, telling us that non-fundamental factors affected its ultimate earnings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Kimball Electronics, its two-year annual EPS declines of 42.1% show it’s continued to underperform. These results were bad no matter how you slice the data.In Q3, Kimball Electronics reported EPS at $0.12, down from $0.43 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Kimball Electronics’s full-year EPS of $0.51 to grow by 149%.

Key Takeaways from Kimball Electronics’s Q3 Results

There were no surprises this quarter. Revenue was in line, and the company reconfirmed full year guidance for revenue and adjusted operating margin. The stock traded up 4.8% to $19.39 immediately after reporting.

Big picture, is Kimball Electronics a buy here and now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

More News

View More

Recent Quotes

View MoreQuotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.