Financial News

Lennox (NYSE:LII) Reports Strong Q3

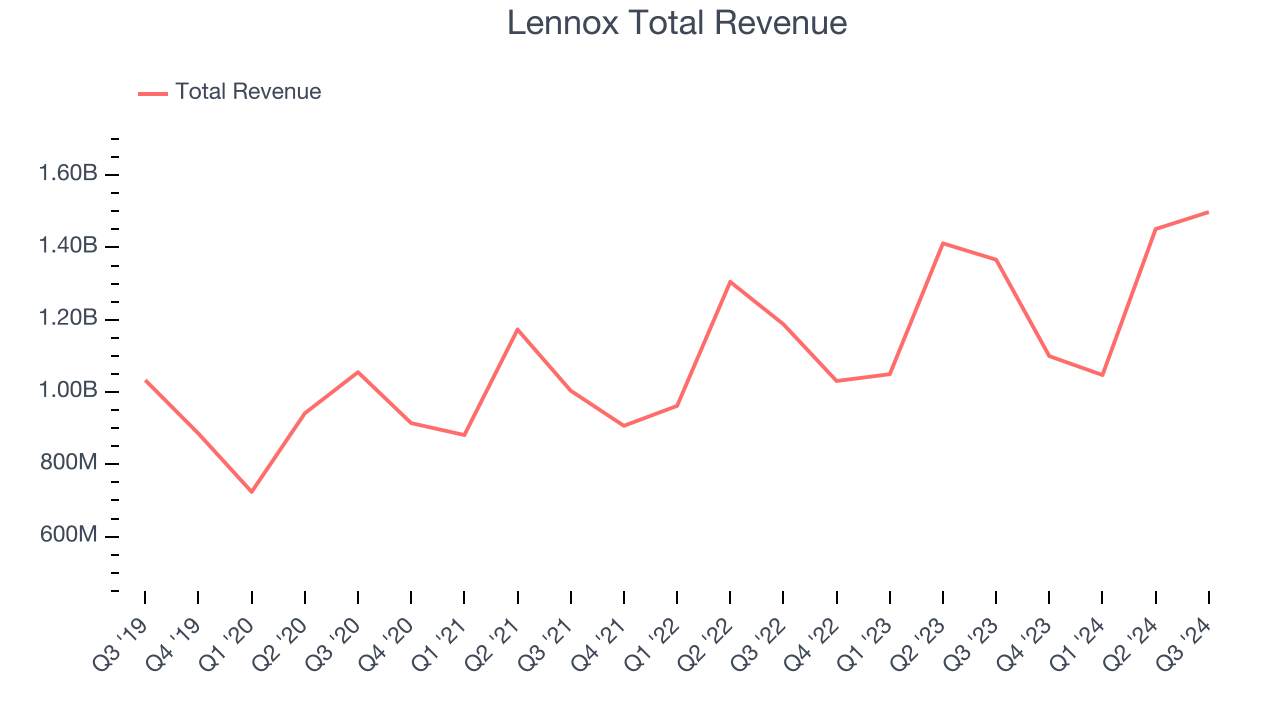

Climate control solutions innovator Lennox International (NYSE: LII) beat Wall Street’s revenue expectations in Q3 CY2024, with sales up 9.6% year on year to $1.50 billion. Its non-GAAP profit of $6.68 per share was also 11.1% above analysts’ consensus estimates.

Is now the time to buy Lennox? Find out by accessing our full research report, it’s free.

Lennox (LII) Q3 CY2024 Highlights:

- Revenue: $1.50 billion vs analyst estimates of $1.42 billion (5.9% beat)

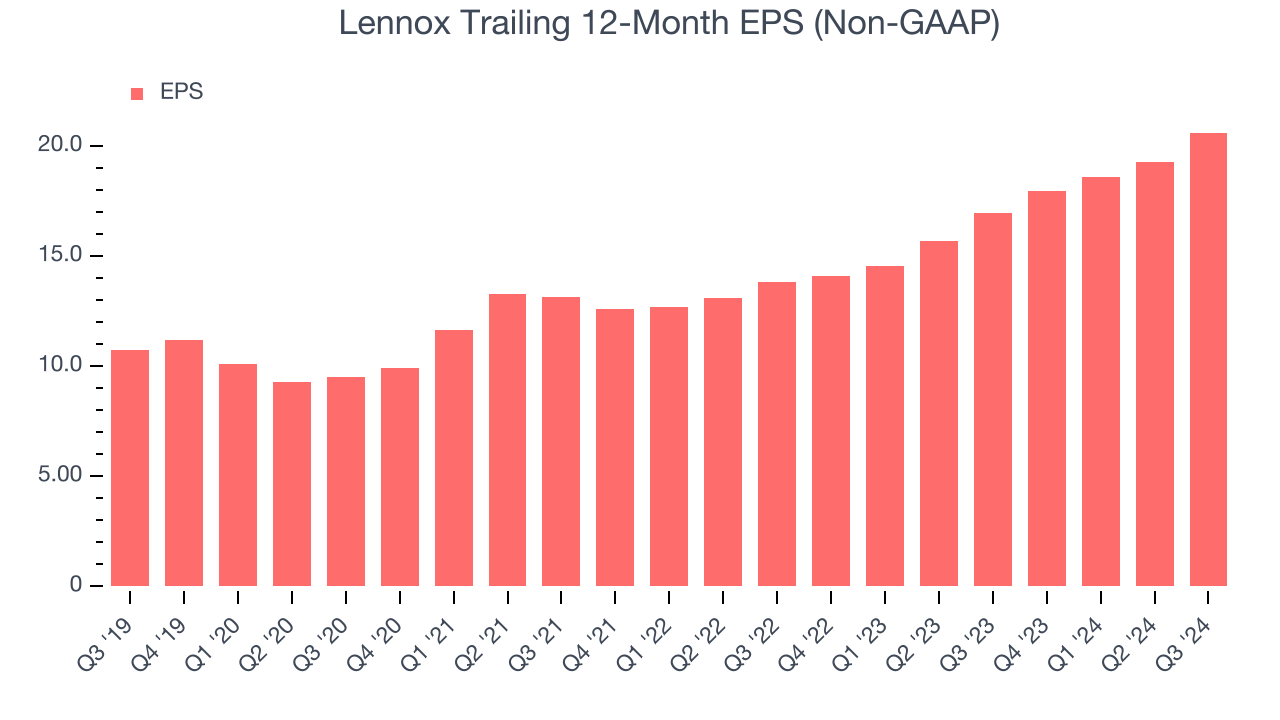

- Adjusted EPS: $6.68 vs analyst estimates of $6.01 (11.1% beat)

- Management raised its full-year Adjusted EPS guidance to $20.88 at the midpoint, a 5% increase

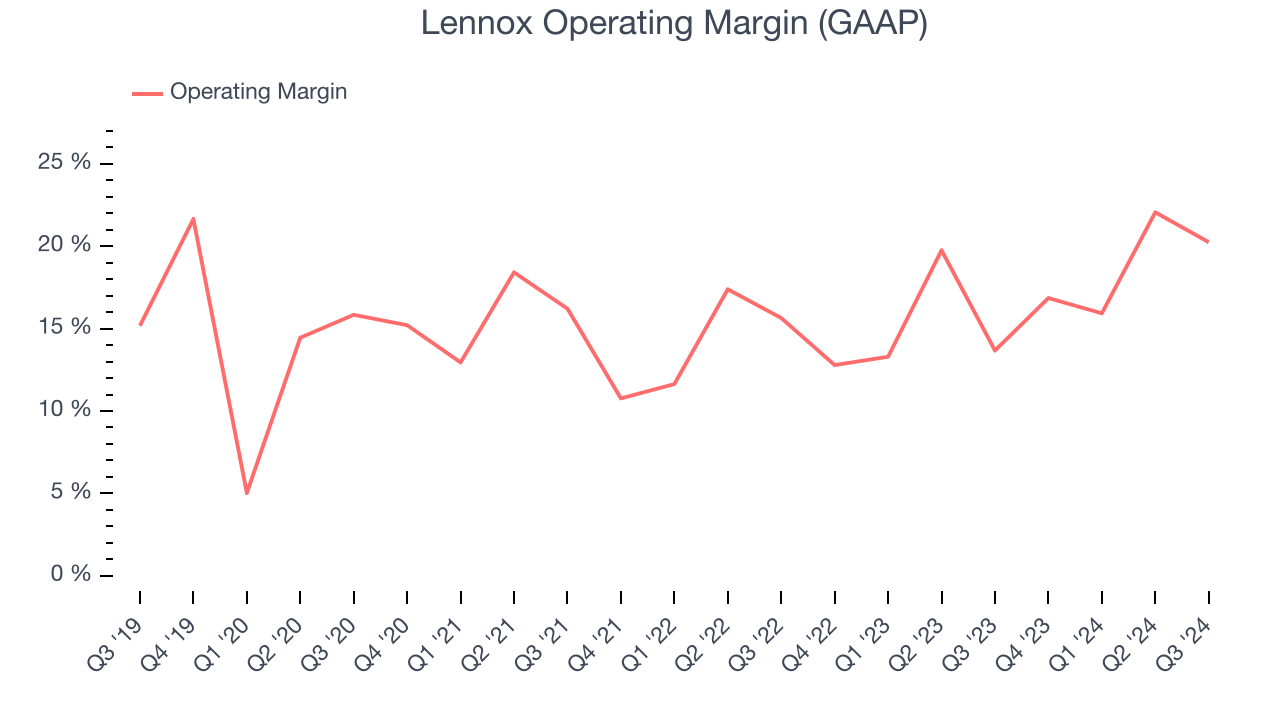

- Gross Margin (GAAP): 32.6%, up from 31.4% in the same quarter last year

- Free Cash Flow Margin: 27.4%, up from 20% in the same quarter last year

- Organic Revenue rose 15% year on year (9.3% in the same quarter last year)

- Market Capitalization: $21.18 billion

"The Lennox team is proud to deliver another exceptional quarter driven by the effective execution of our transformation plan," said Chief Executive Officer, Alok Maskara.

Company Overview

Based in Texas and founded over a century ago, Lennox (NYSE: LII) is a climate control solutions company offering heating, ventilation, air conditioning, and refrigeration (HVACR) goods.

HVAC and Water Systems

Many HVAC and water systems companies sell essential, non-discretionary infrastructure for buildings. Since the useful lives of these water heaters and vents are fairly standard, these companies have a portion of predictable replacement revenue. In the last decade, trends in energy efficiency and clean water are driving innovation that is leading to incremental demand. On the other hand, new installations for these companies are at the whim of residential and commercial construction volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates.

Sales Growth

A company’s long-term performance is an indicator of its overall business quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for multiple years. Unfortunately, Lennox’s 6.6% annualized revenue growth over the last five years was mediocre. This shows it couldn’t expand in any major way and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Lennox’s annualized revenue growth of 8.1% over the last two years is above its five-year trend, suggesting some bright spots.

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations because they don’t accurately reflect its fundamentals. Over the last two years, Lennox’s organic revenue averaged 7.6% year-on-year growth. Because this number aligns with its normal revenue growth, we can see the company’s core operations (not M&A) drove most of its performance.

This quarter, Lennox reported year-on-year revenue growth of 9.6%, and its $1.50 billion of revenue exceeded Wall Street’s estimates by 5.9%.

Looking ahead, sell-side analysts expect revenue to grow 6.8% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and illustrates the market thinks its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Operating Margin

Analyzing the trend in its profitability, Lennox’s annual operating margin rose by 4.4 percentage points over the last five years, showing its efficiency has improved.

This quarter, Lennox generated an operating profit margin of 20.2%, up 6.6 percentage points year on year. The increase was solid, and since its operating margin rose more than its gross margin, we can infer it was recently more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

We track the long-term growth in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth was profitable.

Lennox’s EPS grew at a remarkable 14% compounded annual growth rate over the last five years, higher than its 6.6% annualized revenue growth. This tells us the company became more profitable as it expanded.

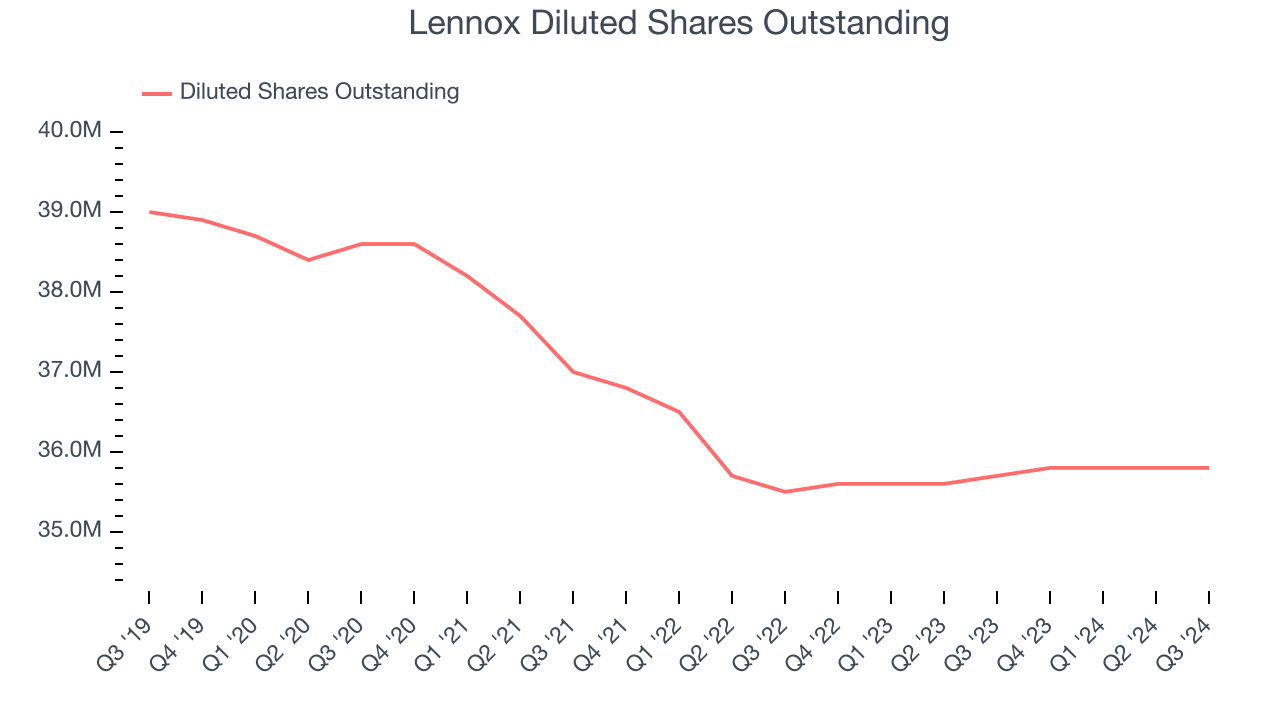

Diving into Lennox’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, Lennox’s operating margin expanded by 4.4 percentage points over the last five years. On top of that, its share count shrank by 8.2%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business. For Lennox, its two-year annual EPS growth of 22.2% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q3, Lennox reported EPS at $6.68, up from $5.37 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Lennox’s full-year EPS of $20.61 to grow by 9.7%.

Key Takeaways from Lennox’s Q3 Results

We were impressed by how significantly Lennox blew past analysts’ organic revenue and EPS expectations this quarter. We were also excited it raised its full-year EPS guidance. Zooming out, we think this quarter featured some important positives. The stock traded up 2.9% to $612 immediately following the results.

Lennox had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment.The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy.We cover that in our actionable full research report which you can read here, it’s free.

More News

View More

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the following

Privacy Policy and Terms Of Service.