Financial News

3 High-Yield Values Ready To Rebound

High yields are attractive but can be a red flag for investors. Marketbeat.com’s list of High Yield stocks has many names that cannot sustain their high yields, have already cut their distributions, or are on track to do so, but not all are in this category. Names like Enbridge (NYSE: ENB), US Bancorp (NYSE: USB), and Whirlpool (NYSE: WHR) are paying high yields partly because their share prices have moved lower, but that movement is not because of their operational quality, and it is an opportunity today. Another reason they pay high yields and are on this list is because they are high-quality capital-returning companies with healthy cash flow. More importantly, none need to cut or suspend their payments, and all are in a position to rebound.

Enbridge: 7% Yield Getting Bought By The Institutions

There is cause for concern among Enbridge’s investors. The company faces competition from the Trans Mountain Pipeline, which is expected to begin operations next year. The mitigating factor is a new tolling scheme that has been agreed to in principle; the new scheme provides an incentivized system that aims to keep customers using the Enbridge Mainline system and Enbridge investing in capacity and operational quality. Until then, the company continues outperforming its consensus estimates and is generating large amounts of cash.

The last earnings report sparked several analysts' comments to the effect core strength was apparent and incremental expansion was expected. The takeaway is that 6 analysts rate the stock at Hold, and they see at least 13% of upside for the market. This is compounded by an active institutional community buying the stock on balance for the last year. The important detail in the data is that institutions have bought at a pace greater than 3:1 compared to selling and have their ownership up to 50%. Enbridge next reports earnings in early August.

The stock isn’t expected to post a significant rally but is trading at the bottom of a long-term trading range. A move to the top of the range could add as much as 30% to the price action.

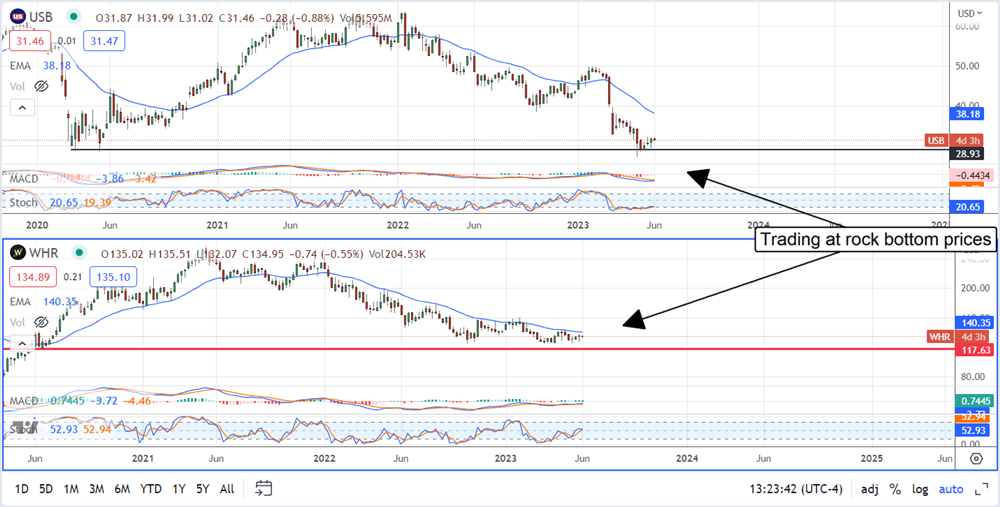

US Bancorp: The Baby Got Thrown Out With The Bathwater

Shares of US Bancorp are down 33% from earlier in the year due to fear of a banking crisis. The fear is not misplaced, but it has caused an overreaction in the market that put USB’s dividend yield around 6%. The payout is only 50% of the earnings, and the earnings outlook has been trimmed since the first of the year. This leaves the company in a solid position to continue paying the distribution and outperform its expectations.

The 18 analysts rating the stock have produced enough downgrades to make it 1 of Marketbeat.com’s Most Downgraded Stocks but take that with a grain of salt. The stock is still rated at Moderate Buy, and there is about 50% upside based on the consensus figure. Even the newest targets, which are the lowest, assume about 17% of upside from the $31.50 price action. USB stock has also seen a large increase in institutional and insider buying since the price imploded.

Whirlpool: Ready To Sparkle In Q2

Whirlpool shares are down due to a marked decline in the expectations for revenue and earnings. The opportunity is that consensus figures are well below last year’s levels despite lingering strength in the consumer and home construction markets. The stock also pays more than 5.0% in yield, making its 8.5X multiple all the more attractive.

The analyst data is mixed, the consensus rating is Hold with a price target trending lower than last year, but the most recent and the bulk of the 2023 activity has the consensus moving higher. Assuming that Q2 results are better than the consensus, the upswing in the price target should turn into a trend. The institutional activity is also mixed but favors an upswing in price action. On balance, the institutional activity is even over the last 12 months, but a noticeable shift to the buy-side occurred in Q1 2023 and is ongoing in Q2.

If you believe this article contains misleading, harmful, or spam content, please let us know.

Report this articleMore News

View More

Recent Quotes

View MoreQuotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.