Financial News

Micron’s Monster 161% YTD Rally Isn’t a Reason to Sell

Micron’s (MU) monster 161% year-to-date surge might seem like a signal to lock in profits. However, the tailwinds from artificial intelligence (AI)-driven demand and solid earnings growth potential indicate that the rally in MU stock is far from over.

The company is benefiting from rising demand for memory and storage products as data center operators expand the infrastructure behind AI. As this demand accelerates and investments in AI infrastructure rise, Micron’s earnings outlook continues to strengthen, making its valuation look far more reasonable than its stock chart might suggest.

Further, the supply backdrop remains tight while demand is robust. This is an ideal combination for sustaining higher prices across memory products. Strong pricing will translate into healthier margins and stronger profits, supporting further stock gains.

Strong AI Demand to Push Micron’s Earnings Higher

Micron is likely to benefit from growing demand for its advanced memory products across data center, PC, and mobile markets. The company is witnessing strong demand for its high-value products, especially in the data center end market, where High Bandwidth Memory (HBM), high-capacity DIMMs, and LP server DRAM are driving its growth.

Further, Micron’s data center SSD business reached record revenue and market share in fiscal 2025, and the company expects this strength to continue into 2026 as AI workloads demand both faster and larger storage solutions. Tight industry supply and strong pricing across DRAM markets are likely to enhance profitability, while a more favorable backdrop in NAND is likely to drive healthier margins.

Looking ahead, the growth in AI servers remains the biggest tailwind. Demand growth here is very strong. Moreover, Micron will also benefit from a rebound in traditional enterprise servers. The growing demand from AI and traditional will continue to support its DRAM revenue.

HBM remains the key growth catalyst for Micron. In HBM, its market share is expected to expand in the coming quarters as it ramps next-generation HBM4. The company has already shipped HBM4 samples offering industry-leading bandwidth and is preparing customized versions of HBM4E, which are expected to command higher margins. Its customer roster has expanded to six major buyers, and most of Micron’s HBM3E supply for calendar 2026 is already under pricing agreements. Discussions for HBM4 supply are ongoing and are expected to conclude soon.

Beyond HBM, server-grade LPDDR5 posted more than 50% sequential growth and hit a record high in revenue last quarter, indicating that AI-related memory demand is broadening. On the storage side, AI inference workloads are pushing data centers toward higher-performance NAND. Micron is gaining share with its latest products. With HDD shortages expected to boost further NAND adoption, the near-term outlook looks favorable for Micron.

Even consumer markets are turning into incremental drivers for Micron. PC demand is improving thanks to the end-of-life of Windows 10 and the rise of AI-enabled PCs. In mobile, more AI-ready smartphones are increasing DRAM content per device, providing a solid growth platform.

Overall, Micron is positioned for record revenue and earnings in fiscal 2026. With AI accelerating demand across every major end market and Micron executing well on technology leadership and supply agreements, its stock could trend higher.

MU Stock Is a Compelling Bet in the AI Space

Micron’s explosive YTD performance isn’t a reason to sell the stock. It reflects the company’s solid fundamentals and a strong demand environment. With AI driving unprecedented demand for advanced DRAM, HBM, and high-performance storage, Micron is likely to deliver solid growth. Tight industry supply, improving pricing, and leadership in next-generation products like HBM4 give Micron a solid base for margin expansion and earnings growth.

Trading at roughly 12.5 times forward earnings, Micron looks inexpensive for a company on track for substantial growth. Analysts expect MU’s earnings per share to jump more than 115% in fiscal 2026, indicating that the current rally could sustain.

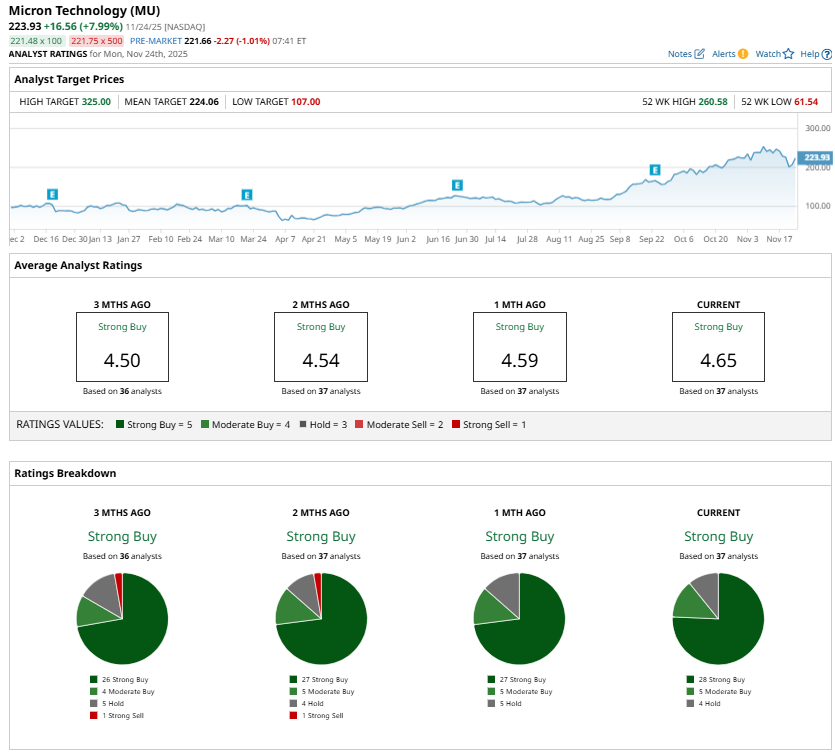

Analysts are upbeat on MU stock and maintain a “Strong Buy” consensus rating.

On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

More News

View More

Recent Quotes

View More

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.