Financial News

Askeladden Capital Shares Primary Research with AstroNova Shareholders

Former AstroNova Employees and Industry Veterans Critical of AstroNova's Dated, Unfocused Go-To-Market Strategy

AstroNova's Board Doubled Down on Key Supplier Memjet During Ongoing Quality Issue, Two Years Before Making Disastrous MTEX Acquisition To Diversify Supplier Base

Transdigm's Recently Raised Bid for Aerospace Components Company Servotronics Highlights Potential to Unlock Value at AstroNova with Better Governance

FORT WORTH, TX / ACCESS Newswire / June 3, 2025 / Dear AstroNova shareholders,

I write to you as the portfolio manager of Askeladden Capital (collectively, "we,") which on behalf of our clients is AstroNova's largest shareholder, owning approximately 9.2% of the shares outstanding. We have owned 5% or more of AstroNova since 2020. Over recent years, we have become increasingly concerned about the company's strategic direction and execution. After many attempts to engage with the company failed - and results worsened - we decided the best way to improve the company's performance was to nominate five candidates for election to AstroNova's Board of Directors at this year's Annual Meeting on July 9, 2025.

We recently published our detailed plan , based on our research dating back to 2016. Since March, we have deepened and broadened our research by conducting over 25 interviews with 18 relevant experts, including multiple print-industry executives who have reached out to us to offer their perspectives and assistance with setting AstroNova on the path to fulfilling its potential.

We heard many criticisms of AstroNova's leadership, strategy, and execution. If we had to sum it up in three quotes:

" It's easy to fall into the dinosaur approach, thinking that what worked for 30 years will continue to succeed." [1]

"The buck has to come back to the CEO and the Board, in my view. It's that speed of change, it's the execution, and then it's really getting into the details." [2]

"It really comes from the top of the company […] They're just looking at the past and remembering back in the good old days, what all went well and what w[as] successful and just copy-paste that into the future. I don't believe that does work." [3]

Individuals whom we interviewed had backgrounds including:

Managers at printhead technology providers such as Memjet and Epson who directly interacted with AstroNova (one also directly interacted with MTEX);

C-level executives and key leaders at industrial printing peers such as Domino and Markem-Imaje, who oversaw significant growth or transformation of those businesses;

Managers at AstroNova competitors such as Afinia and OKI;

A former sales representative and former sales executive at AstroNova, and a current TrojanLabel customer whom they served;

The principal of a private equity firm which thoroughly evaluated MTEX as a potential investment, as well as a former MTEX employee directly reporting to MTEX CEO Eloi Ferreira at the time of AstroNova's acquisition

We continue to identify and speak to additional experts and follow up with additional questions for several of those to whom we have spoken. Today, we would like to share some of our key research findings with other AstroNova shareholders. While certain interviews occurred via private, unrecorded conversations, many were, with participants' permission, recorded and transcribed through subscription platforms Tegus/Alphasense and In Practise . Therefore, the analysis we present here relies on and extensively cites these verifiable third-party transcripts. We encourage shareholders to review these source materials in their entirety, come to their own conclusions, and consider conducting their own interviews.

We believe that any one individual can certainly have their own biases or limitations of perspective. However, during our interviews, many patterns emerged, with multiple sources with varied perspectives sharing similar insights. We believe these patterns are worth considering.

Given the hundreds of pages of transcripts and notes, an exhaustive analysis of every aspect of AstroNova's business is impractical (this document is already over 35 pages long).

Therefore, we have chosen to share a detailed, deep-dive analysis into two specific strategic failures we perceive AstroNova's CEO and Board made in the Product Identification segment:

AstroNova's apparent historical over-reliance on printhead technology supplier Memjet, which the company doubled down on with the 2022 Astro Machine acquisition and other product development decisions. We believe this represents a critical, inexcusable, and unforgivable strategic and governance error that contributed to challenges including the 2022-2024 ink quality issues and the disastrous MTEX acquisition.

AstroNova's seeming lack of a coherent, modern sales and marketing strategy, including apparent failures in lead generation, channel management, and quality / customer support.

We believe our analysis comprehensively demonstrates that the company's incumbent Board has been asleep at the wheel, failing to address clear and critical challenges to AstroNova's business. We believe these failures provide a compelling reason for AstroNova shareholders to vote for our slate of highly qualified candidates, who have the specific and complementary expertise needed to clean up the mess created by incumbents.

SECTION 1: ASTRONOVA'S BOARD SEEMINGLY DOUBLED DOWN ON OVER-RELIANCE ON MEMJET

1.1: Background on Printhead Suppliers and AstroNova's Strategic Decisions

To understand AstroNova's Product Identification business, it is important to understand its printers on a somewhat technical level. Whether printing on labels or other media such as cardboard (corrugate) or even wood, an industrial printer system relies on multiple technological components, including:

The "printhead" - which actually deposits the ink onto the media material.

The associated ink delivery system and electronics. We believe the company and industry participants sometimes collectively refer to the printhead and these related components as the "print engine," although we believe "print engine" is a loose concept rather than a formal definition.

A material handling system, which feeds the material through the printer so that it can be printed on. For our purposes, this is largely independent of the printhead / print engine.

Of these, we believe the printhead is the most strategically important component. Why? Printers are a classic razor / razorblade business model. The overwhelming majority of the revenue and profitability comes not from the original sale of the printer, but rather from the annuity-like sales of consumables and parts over the multi-year life of the printer, which we believe is 3 - 7+ years depending on usage and maintenance. [4] If you think about the kind of printers you find in your own office, you can buy paper from many vendors, but ink from likely only one. It is similar for industrial printers: a media handling system could be compatible with media (such as labels) from many providers, but printheads are often only compatible with ink from certain providers.

AstroNova recently disclosed that 82% of its FY2025 revenues in the Product Identification segment were from recurring sources such as ink, media, and parts, driven by its installed base of 10,000+ printers, with merely 18% of FY2025 revenue attributable to hardware / the sales of new printers. [5] The ensuing chart is directly from AstroNova's Q4 FY2025 earnings presentation:

A former executive at Domino Printing (the 3,000+ employee industrial printing and coding subsidiary of Brother Limited) [6] agreed with our assessment that 70% - 80% of lifetime revenues come from consumables and parts, explaining that profitability can be even more skewed:

"In terms of profit, it's even more skewed. For example, 95% of Domino's profits in some technologies come from consumables and the aftermarket." [7]

While the exact percentage will obviously vary by specific product, annuity-like consumables revenues are clearly vitally important to manage. In this regard, printheads are critical, because ink sales comprise a significant portion of aftermarket revenue and profits.

AstroNova, as well as many other companies in the industry, does not produce its own printheads. Instead, it designs and sells products with printheads provided by third parties. While AstroNova does not work with all of the following companies, and the technology depends on the application, in general, industrial printhead vendors include Memjet, Canon, Ricoh, Sanyo, HP, Epson, and others. [8] (Certain of these companies, such as Epson and HP, sell their own printers as well, although sometimes in different market segments than the ones in which they sell printheads.) [9]

Certain printheads are only compatible with certain inks, and many printhead manufacturers "lock" their printheads to use only ink that they supply. A former manager at Epson, who worked with key AstroNova personnel such as Chief Technology Officer Mike Natalizia, explained:

"Memjet and HP both require the customer to buy the ink from them. One of the advantages that we offered to AstroNova on the Epson printheads was to offer them just the printheads with no commitment for ink. They could find their own supplier for ink. Going in that direction would allow them to bring their cost of printing down considerably because they could offer the ink at a lower price, but they could also achieve higher margins because there wouldn't be Epson or HP or Memjet putting their margin on top of the ink." [10]

AstroNova chose not to move forward with Epson technology for reasons we find questionable in light of their subsequent acquisition of MTEX - which we will return to shortly.

As it relates to AstroNova's product portfolio, it is our understanding that AstroNova's QuickLabel product line, comprised of smaller printers for lower volume applications that cost below $10,000, have historically primarily used Canon printheads, [11] [12] although a former SVP at Memjet stated models such as the QuickLabel QL-800 used Memjet technology. [13]

Conversely, the company's higher-volume TrojanLabel products - which cost tens of thousands of dollars and use significantly more ink - have historically relied on printheads from a supplier called Memjet . We spoke to the former Senior Vice President at Memjet who managed the company's relationship with AstroNova for many years - including direct interaction with Chief Technology Officer Mike Natalizia and Chief Executive Officer Greg Woods. This SVP also managed Memjet's relationship with MTEX (we will return to his comments on MTEX later):

"[My relationship with AstroNova] started […] as […] they introduced their first product using the Memjet technology, which was the QuickLabel QL-800[…] Subsequently, I was more deeply involved with them because they acquired Trojan[Label], which was a Memjet OEM. […] there was a period of time where I was also managing what was known at the time as New Solution, which is now called MTEX. We decided at Memjet to separate the MTEX relationship in latter years because there was a fairly well-known disagreement between parties." [14]

We believe that for the TrojanLabel product line, Memjet was a sole-source supplier that AstroNova allowed itself to become over-reliant on. A manager at Epson who worked with AstroNova's technology team, including CTO Mike Natalizia, explained some of the dynamics here. In his view, AstroNova failed to develop the internal technical talent to manage some of the technology surrounding the printhead, such as the ink delivery system and associated electronics. Thus, according to the former Epson manager, AstroNova remained dependent on suppliers for providing this technology:

"They [AstroNova] said, "Hey, we can handle the media. We know how to move the media. We can just buy these print engines from Memjet or HP and then put them on top of our transports and print." Their knowledge of inkjet, how to optimize an ink, how to get it to jet properly, all the technology that goes into how to do an ink delivery system, it was all given to them by the manufacturer.

[…] because the manufacturer was supplying that technology, [the] manufacturer said, "Hey, we'll supply this at a pretty good price so you can keep your product costs low, but we're going to charge you an arm and a leg for the ink going forward." Their technology base is not very good. I'm in the business. I grade my customers on their technology ability and I would probably give them a two or three out of five points.

I think they were planning on moving in the upward direction more high end equipment range and get their cost of printing down by hiring this person, but then when they went through some hard times, ended up laying him off. To me, that was their key person as far as their inkjet technology ability, was this person who ended up leaving the company." [15]

As a brief note, we did hear some positive things about AstroNova CTO Mike Natalizia in various calls, so this should not be construed as direct criticism of him. We believe it is entirely possible (though difficult to determine from the outside) that he and his team were not allocated sufficient resources by CEO Greg Woods and the Board of Directors.

One of the first indications that AstroNova's over-reliance on Memjet was problematic arrived in calendar 2021 (which was AstroNova's FY2022, ending on January 31, 2022). At the end of FY2022, AstroNova disclosed elevated warranty costs related to an ink quality issue, which management claimed was attributable to a "supplier" delivering "poor quality product ." [16]

Our understanding from conversations with industry participants is that the supplier in question was Memjet. [17] One public source is a series of posts starting December 23, 2021 on the "PrintPlanet" forum; the first of which is:

"We have three Trojan T2C Memjet printers and back around May we started having all kinds of issues with what they are calling a crystalline ink contamination issue from the ink manufacturer." [18]

These ink quality issues were not resolved until the end of FY2024 [19] after originally surfacing at the end of FY2022, despite assurances by CEO Greg Woods that it would be a short term fix, [20] with financial disclosures referencing millions in foregone revenues and costs related specifically to this issue, which rendered customers' printers unable to print (thus reducing consumables sales for AstroNova, and according to its Form 10-K, impacting its brand perception in the market). [21] While we believe AstroNova should have addressed the quality issue more rapidly, it brings up a broader strategic question: why did the company (and its Board) believe that it was appropriate to be so dependent on one supplier?

If we had been in AstroNova's place, the quality issues related to Memjet products would have caused us to seek alternatives. Instead, while the quality issues were ongoing, AstroNova chose to double down on its Memjet exposure when it announced the purchase of Chicago-based industrial printing concern Astro Machine in August 2022; Astro Machine generated $22 million in trailing twelve-month revenue and was purchased for approximately $17 million. [22]

Company management mentioned to us at the time that Astro Machine used Memjet technology, which we recently re-confirmed with former employees of both Epson [23] and Memjet, with the former SVP from Memjet referring to Astro Machine as a:

"… very large Memjet customer. They had looked at, I think, some other technologies and some other parts of their business, but Memjet was the predominant product that they had in their range." [24]

Meanwhile, the Memjet-related ink issues continued to persist. We believe this bears repeating: CEO Greg Woods - and AstroNova's Board - decided that while experiencing a major quality issue related to Memjet-based TrojanLabel machines , it was a good idea to increase AstroNova's exposure to Memjet via a sizable acquisition . Nobody forced AstroNova to do this; they could instead have identified and acquired a business that had exposure to a different print engine and the relevant technical expertise. The decision to increase Memjet exposure was an intentional choice by CEO Greg Woods and the Board.

Outside of M&A, AstroNova could also have allocated more funds towards internal product development efforts. On this note, let us return to the Epson story - which we believe is directly relevant to AstroNova's 2024 decision to purchase MTEX. We previously mentioned that Epson offered AstroNova an "unlocked" printhead, where AstroNova could utilize multiple ink suppliers - similar to the benefits AstroNova is touting as part of the MTEX deal. Why did AstroNova choose not to go down this path? The former manager at Epson shares his view:

"It's a pretty sizable development to move to a new technology, especially piezo. Piezo is much more complicated. Memjet, for example, makes it pretty easy. They supply the printhead ink system, the electronics, everything goes in. You just take this unit and you put it on top of the media handling equipment that in a lot of cases is made by AstroNova or TrojanLabel […] we did not offer a print bar or print unit that could do that.

Plus the cost of the printheads is probably in the range of 10X the cost to get similar performance or similar characteristics. The added cost […] what that does is affects your entry cost, the customer's entry costs. They're in the mid-market range and the customers are looking at say a $50,000, $75,000, maybe $50,000-$100,000 printing system to print labels. It's relatively slow.

If they moved up to the piezo printheads that we were offering, the equipment would cost probably in the $200,000-$300,000 or it could be $300,000, say 3X the entry cost, but it would be faster and it would be more productive and the total cost of printing would be lower because the ink costs would be lower. Making that investment and moving into a different market space was a big decision for them." [25]

It certainly seems reasonable for AstroNova to be cautious about spending a lot of money to develop far more expensive equipment that would take them into a different market segment. Indeed, as should be intuitive, all experts we spoke to agreed that the customer base for $300,000+ machines is very different than the customer base for sub-$100,000 machines. An existing TrojanLabel customer told us that an up-front printer price exceeding six figures would be too expensive for his business. [26]

However, it seems to us that AstroNova subsequently threw caution to the wind and made a big investment which turned out quite poorly. Rather than building out an internal engineering organization that could solve these challenges, in May 2024, AstroNova announced the acquisition of Portugal-based MTEX for $18.7 million in cash, with the assumption of $3.4 million in debt. [27] As we will discuss later, MTEX offers large, expensive machines; we believe that AstroNova's lack of experience selling such high-priced products has contributed to MTEX's struggles.

The strategic rationale for the MTEX acquisition, as articulated on the recent April 2025 earnings call, is that MTEX's technology will allow AstroNova to diversify its supplier base (by which we believe they mean Memjet). As CEO Greg Woods explained:

"In fact, together with MTEX, we have developed new, highly disruptive print engine technology. This technology allows our products to use a broader range of inks that can be multi-sourced, which we believe will dramatically lower our ink costs and reduce our dependence on the limited set of suppliers on which we have had to rely." [28]

We believe that acquiring MTEX or developing a solution in-house with a supplier such as Epson were not the only options that AstroNova had. A former executive at Domino explained to us that technology access has become far more democratized over the past decade, with a number of Asian integrators who can design products using different printheads and ink systems, at a lower cost than in-house development:

"A significant change in the last 10 years, maybe less, is the rise of integrators in the marketplace. These aren't the traditional names; they're using print heads from Ricoh, Sanyo, and others, and providing an ink system that works with those print heads. They're adding lower-value components themselves.

Many Far Eastern integrators are now involved in the business. Domino has used some of them, and the cost to develop something with them as an integrator is much less than doing it in-house. Even Indian businesses are now involved in this. I was talking to a company in the Netherlands while I was still at Domino, which was acquired by an Indian company. It's interesting to see how access to these technologies has changed. It used to be dominated by Western European and North American businesses using Japanese technology, but that's no longer the case. […]

There's a company in Vietnam called Mylan that does this integration and will brand it however you want. Domino has worked with Mylan for one of their technologies, although not in the space that AstroNova is working in. Mylan is flexible and agnostic regarding which printhead they use, with access to various suppliers. Their expertise lies in the backend of the equipment, such as the ink system and software integration." [29]

In fact, MTEX's technology wasn't even purely internal. A former sales leader at MTEX - reporting directly to CEO Eloi Ferreira at the time of AstroNova's acquisition - explained that MTEX's designs were a collaboration between MTEX and a Chinese supplier. [30]

"The print head was purchased from a Chinese supplier. As I understand, the design was a collaboration between MTEX's team and the Chinese team to develop the final product."

Both this MTEX employee and a former Memjet employee [31] confirmed to us that MTEX, like AstroNova, historically utilized Memjet technology. MTEX - unlike AstroNova - chose to partner with a new supplier to design products based on a different printhead. This leads us to question why AstroNova needed MTEX in the first place - why could they have not worked directly with this Chinese supplier (or another supplier, of the many referenced by the Domino executive) to design a product based on different printhead technology?

1.2: The MTEX Acquisition Debacle: Consequences for AstroNova Shareholders

AstroNova followed a seemingly incoherent strategic path, doubling down on Memjet exposure with the Astro Machine deal in 2022 - during an ongoing quality issue with its Memjet-based TrojanLabel printers - then less than two years later, acquiring MTEX in an apparent attempt to diversify away from Memjet. We believe that the MTEX acquisition was poorly conceived, with insufficient due diligence, and a poor integration plan - which have all combined to cause severe value destruction for AstroNova shareholders; ALOT shares declined by almost 50% in the year following the acquisition of MTEX. [32]

Let's analyze five separate problems with the MTEX acquisition.

Problem 1: The MTEX acquisition has been financially disastrous. MTEX was expected to profitably contribute $8 - $10 million in revenue during FY2025 [33] , but only contributed $4.2 million, with an operating loss of $16.9 million, including a goodwill impairment of $13.4 million. [34] At the end of FY2025, AstroNova also announced the discontinuation of 70% of MTEX's product portfolio, described as " low-profit ." [35]

As a result of the lower earnings and increased debt due to the MTEX acquisition, the company breached its debt covenants and suffered an event of default under its credit facility during the quarter ended January 31, 2025 (thus forcing AstroNova to seek a waiver from its lender, which was subsequently granted). [36] If lenders had not agreed to modify terms, AstroNova could potentially have been forced to seek rescue financing on unfavorable terms.

As of the end of FY2025, AstroNova had only $3.3 million in availability at year-end on the company's $25 million revolving credit facility, leaving the company with limited liquidity to navigate a volatile macroeconomic environment. [37] We believe that putting the balance sheet at such risk represents an inexcusable failure of governance by incumbent directors at AstroNova.

Problem 2: We believe due diligence was rushed. In a private conversation subsequent to the MTEX deal, CEO Greg Woods told us that the timing of the Drupa trade show and AstroNova's belief in the presence of a competing bidder for MTEX caused "extra pressure" and resulted in AstroNova "accelerat[ing] some things we typically wouldn't accelerate" in their due diligence.

The former SVP at Memjet further noted issues with MTEX that were understood in the industry, but despite which AstroNova paid a rich price for MTEX anyway:

"The purchase price paid by AstroNova for MTEX, I compare that with the solidity of the Astro Machine business, which was a similar order of magnitude purchase price [… MTEX… ] was significantly less mature, the fact that one minute, MTEX is making an ATOM, Trojan two Compact competitor, then moves into an overprinter, then starts selling UV cabinets for clothing during COVID, to then switch back to trying to extend into more expensive, higher markets in terms of the packaging segment, it seemed like a very rich price, given that less maturity and with a very fluid product portfolio. […]

Just one last thing to mention about MTEX. I think there was also a lot of disquiet in the marketplace in terms of their ability, that they grew very fast and then to support products. There were a number of situations where I heard from OEMs and resellers who would struggle to get post-sales support when there were issues with the technology.

When it's one or two, that can be very much a customer-specific scenario. When you get a little bit more of a regular point of feedback around that, then it raises some more questions. I think I've read some online comments about the support experience. I think that was another area that was questionable for me around their potential ability. [38]

The former MTEX sales leader shared perspective on these reliability and support issues as well:

"We had many situations with small problems in the machines, like a small piece or accessory. However, the printer itself was very robust. […]

Regarding the hardware printheads, that's another story. Printer printheads require constant maintenance and sometimes even need replacing. Due to the learning curve, clients were doing things wrong and ruining their own printheads. This was a big problem for the clients and MTEX, and we were losing money. As a result, the printheads required a lot of maintenance." [39]

We question what sort of due diligence was performed by AstroNova's Board prior to the acquisition, and why the Board agreed to pay such a robust purchase price despite these apparently foreseeable issues. Moreover, in light of these potential reliability issues, we believe that AstroNova's rollout of new products based on MTEX technology may face skepticism from customers. We discussed AstroNova's new products with an existing TrojanLabel customer and asked if he would want to be an early adopter. His response:

"Not particularly. I prefer to see that it's working first. A business of my size doesn't have the resources to deal with those kinks. New technology often means you're essentially beta testing it for someone else. I've learned my lesson and been burned several times in the past. I always wait a bit to ensure the kinks are ironed out before committing." [40]

Problem 3: Is MTEX's technology special, and does its business model match AstroNova's?

While AstroNova continues to tout the benefits of MTEX's technology, [41] the company's financial disclosures show that MTEX's revenues and profitability have been far below expectations since the acquisition. [42] We believe that shareholders should pay more attention to the cold, hard facts - i.e., MTEX's poor financial results during AstroNova's ownership - rather than management's promises about what MTEX will contribute in the future.

A former sales director at AstroNova offered his opinion of MTEX's technology. He further questioned how MTEX's business model fit into AstroNova's technology:

"It gave AstroNova the access to an alternative print technology, but I won't perceive this print technology as specifically good. I don't think it is really. It was a different vendor, different ink technology, different printer technology. Other than that, I don't see any big advantages over the print technology that already exists from the likes of Canon or OKI or whatever. It's basically very cheap. It's more of a desktop-style printhead from HP MTEX was using in their machine.[…]

I'm not really surprised it went […] that bad. What I honestly don't understand from the beginning really is that the business model of MTEX was really different from the one AstroNova was having. AstroNova always tried and did sell the hardware at a good margin. Not a superior margin, but at a healthy margin and made even more margin out of the recurrent revenue stream.

[…] While MTEX was completely different, they tried to make money in the first place on the hardware, but sold the ink extremely cheap. In reality, they didn't even care where the customers bought their ink." [43]

A former sales leader at MTEX reporting directly to MTEX CEO Eloi Ferreira echoed the last point to some degree. While he did state that MTEX was focused on consumables sales in the long term, he confirmed MTEX would sometimes offer the first year of ink free to incentivize hardware purchases. [44] In his own words:

"At the beginning of the business with any client or distributor, ink was an advantage of doing business with MTEX. MTEX would provide as many kits of ink as needed to start. After the first year, we would start making money from the consumables because the machines don't use a lot of ink compared to other solutions.

I wouldn't say that the consumables were the main point of revenue, at least not from my perspective. Consumables were affordable and durable, and the machines used a small amount of ink for the market unless we had clients printing almost 24/7. Consumables were not significant for the packaging, at least."

The former SVP at Memjet echoed the last point, and also pointed out that MTEX's machines are much larger and more expensive than AstroNova's. As he discusses in the quote below, AstroNova has entered a new market segment in which they have limited experience, with a much higher up-front price point than their traditional QuickLabel and TrojanLabel product lines, that leaves them competing with much larger and more sophisticated global players such as HP:

"That's a market that, I think, AstroNova appear[s] to have wanted to access more of by buying MTEX, because they have a wider range, larger, more substantial equipment that gets into that upwards of several hundred thousand dollars. The question in my mind, and I don't have the answer, so I'm just going to mention it, those markets sound lucrative, but you start to get into the competitive space of some other print technologies and other bigger OEMs, with more sales organization, operational in the street, more resources, and more, I think, competent competitors, multiple competitors, some of those being the likes of Konica Minolta.

Certainly, even when you look at HP's label, the HP Indigo, the HP label business is one which, if you look at their numbers and you start looking at some of the analyst reports, is a market where they don't see as much growth. […] My question is, at the above $200,000, you start to become more of a competitor target for big billion-dollar OEMs who have a long history in the print-for-pay market, long-established relationships, many cases more reason to care to be really successful, and to stop others taking food out of their revenue stream.

I also am unsure, as to just because you're selling a larger, more expensive piece of capital goods, if that automatically translates into a significantly more lucrative revenue stream on the ink side. When you start to look at those overprinters, the volume may be higher, but actually the coverage of ink is normally less than when you start looking at those desktop printers, even benchtop printers." [45]

It seems to us that acquiring MTEX creates the same challenges that seemed to dissuade AstroNova from developing products around Epson's unlocked piezo printhead technology, i.e., moving into a different market segment with much higher prices. We believe that the very different sales processes and cycles relating to much larger and more expensive machines, against much more sophisticated and experienced competition, as well as the seemingly less meaningful contribution of lucrative ink revenues, may explain AstroNova's struggles to generate revenues and profitability from the MTEX business.

Problem 4: Lack of Integration Plan at MTEX

An MTEX employee who reported directly to MTEX CEO Eloi Ferreira explained that despite being a leader at MTEX, he was not given an opportunity to develop relationships with key AstroNova personnel:

"I didn't have much opportunity to spend time with AstroNova's leadership. Honestly, I only saw them a couple of times and exchanged a few words." [46]

He referenced a number of post-acquisition challenges, including:

AstroNova not building relationships directly with him or many other key employees, instead operating through CEO Eloi Ferreira (who is now involved in arbitration with the company, according to AstroNova's FY2025 Form 10-K),

AstroNova failing to understand, plan for, or address the cultural differences between MTEX's base in Porto in Northern Portugal and AstroNova's East Coast US culture.

AstroNova failing to understand, plan for, or address the integration of an entrepreneurial company into public-company processes and procedures.

In his own words:

"I think what happened was a clash between workflow and work cultures. From my perspective, MTEX, before AstroNova, had its hands in too many areas. We were trying to launch products in labeling, DTF packaging, and innovating in flexible packaging. It was a lot of different projects starting, investing, and developing simultaneously. We tried to cover everything in terms of printing, and that was fine before AstroNova because MTEX could make decisions independently. They could choose to pause one product, project, investment, or development and assign the workforce according to their needs.[…]

MTEX wasn't ready to embrace it fully. They believed they were prepared, but honestly, the American way of working-fast-paced and organized-wasn't aligned with MTEX workflow and culture. The team wasn't prepared for the challenge at that time. We were caught off guard and couldn't keep up with marketing, production, manufacturing, and development. That's what happened from my perspective.[…]

This pressure and change in customer service led many customers to pause projects or rush purchases, creating a chain reaction. Clients were rushed to make payments to start production, but the production site wasn't ready to handle the volume, causing delays in deliveries and full payments for machines. […]

I don't think they were aware of the labor culture in Portugal, especially in the north. From my perspective, they didn't care. It was just about meeting targets. They would ask, "Can you do it?" and we would say, "Yes, we can." In the end, you saw the results."

Problem 5: AstroNova's CEO and Board got themselves into this mess in the first place.

There is obviously strategic merit in diversifying one's supplier base - on this point, we and AstroNova's incumbents seem to agree. However, we thoroughly disagree with incumbents on the correct fashion in which to achieve this.

First - as we discussed - AstroNova's management and Board doubled down on Memjet technology in 2022, spending $17 million to acquire Astro Machine and its over $20 million in revenues while already facing unresolved quality issues with Memjet-based products . Today, management argues that MTEX and its non-Memjet technology is critical to the future of AstroNova - so why did they double down on Memjet technology merely three years ago, and less than two years before acquiring MTEX?

Second - shareholders should ask how and why a small company in Portugal, on a comparatively shoestring budget, managed to work with a third-party supplier to develop technology that AstroNova, with all of its resources, could not? In FY2025, MTEX reported less than $5 million in revenues with operating losses, compared to the overall Product Identification segment's >$100 million in revenues and positive operating profits (excluding MTEX results and the goodwill impairment charge). [47] (In a recurring theme, we later cite the Memjet SVP who notes that Afinia, with far less resources than AstroNova, seemed to be outcompeting it in areas such as social media lead generation and channel partnerships.) [48]

We believe AstroNova's inability to organically develop products based on non-Memjet technology speaks to dysfunction in the CEO and Board's allocation of resources, with an apparent dearth of technical talent leaving AstroNova overly dependent on external suppliers.

We believe that this pattern of events suggests that incumbent directors were not asking the right questions, evaluating the right metrics, or holding the CEO accountable for the strategic decisions he was making. Approving the Astro Machine acquisition, which doubled down on Memjet exposure - then within two years approving the MTEX acquisition, designed to decrease the very same Memjet exposure they had recently increased - speaks to a lack of coherent strategic vision and long-term planning on the part of AstroNova's Board.

SECTION 2: DECLINING ORGANIC REVENUES IN ASTRONOVA'S PRODUCT IDENTIFICATION SEGMENT, AND POTENTIAL CAUSES THEREOF

Our second major area of analysis is the poor organic performance of AstroNova's Product Identification segment. While CEO Greg Woods has grown this business through acquisition, our analysis of AstroNova's financial disclosures - as well as our discussions with former AstroNova employees, a customer, and numerous industry participants familiar with the business - suggests that Mr. Woods has done a poor job of managing the Product Identification business, leading to declining organic revenues.

2.1: Factual Background - Review of Recent Results

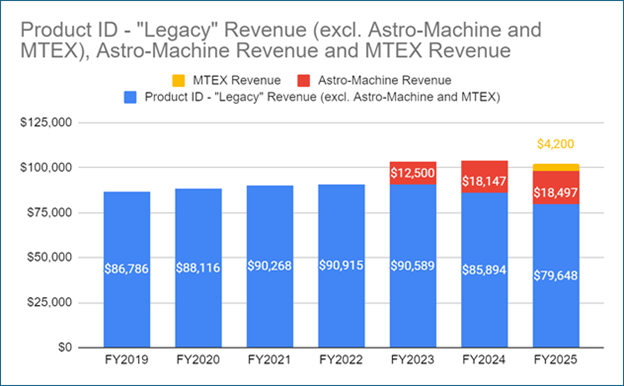

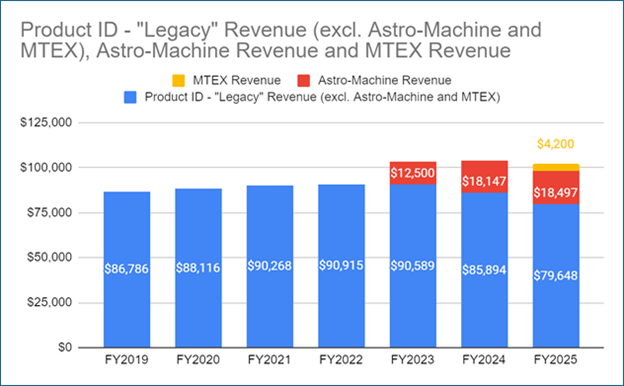

Let's start with a brief review of indisputable facts, sourced directly from AstroNova's own disclosures. Investors who carefully study these disclosures will find that acquisitions have masked organic decline in Product Identification segment revenues when recent results are compared to pre-pandemic levels. Excluding contributions from acquisitions, revenues in the "legacy" business appear to have peaked in FY2022 and declined every year since.

|

Product ID - Total Revenue (Thousands USD) |

Astro Machine Revenue |

MTEX Revenue |

Revenue, Excl. Astro Machine and MTEX |

Comments [49] |

FY2019 |

$86,786 |

|

|

$86,786 |

|

FY2020 |

$88,116 |

|

|

$88,116 |

|

FY2021 |

$90,268 |

|

|

$90,268 |

|

FY2022 |

$90,915 |

|

|

$90,915 |

|

FY2023 |

$103,089 |

$12,500 |

|

$90,589 |

Astro Machine acquired in August 2022 for $17.1 million in cash and included for partial year. Company cited ~$22 million in trailing twelve month revenue for Astro Machine. |

FY2024 |

$104,041 |

$18,147 |

|

$85,894 |

Astro Machine included for full year. Actual revenue of $18.1 million is roughly 18% below the $22 million management discussed at the time of the acquisition. |

FY2025 |

$102,345 |

$18,497 |

$4,200 |

$79,648 |

MTEX acquired in May 2024 for a total enterprise value of 24.3 million euros and included for partial year. Company guided to $8 to $10 million in additional revenue for the remainder of FY25. Actual MTEX results of $4.2 million are less than half of the midpoint of original expectations at the time of acquisition. Astro Machine included for full year. |

AstroNova Product ID segment revenues, excluding acquired Astro Machine and MTEX revenues |

|

|

|

|

FY2025 vs FY2022, absolute |

|

|

|

-12.4% |

FY2025 vs FY2019, absolute |

|

|

|

-8.2% |

The following chart, sourced from the company's own Form 10-K disclosures, summarizes revenue progression for Astro Machine, MTEX, and the PI segment excluding those acquisitions.

In FY2019 (ended January 31, 2019), the Product Identification segment reported $86.8 million in revenues. In August 2022 (part of FY2023), AstroNova acquired Astro Machine and disclosed to investors that Astro Machine had approximately $22 million in revenue over the prior twelve months. [50] In May 2024 (part of FY2025), AstroNova announced the acquisition of MTEX, expected to add $8 to $10 million in revenue over the remainder of the fiscal year. [51]

Therefore, simple addition implies that with no organic growth for the legacy AstroNova business or any of the acquired units, the Product Identification segment should have reported ~$87 + ~$22 + ~$9 million in revenues, or approximately $118 million in FY2025 revenue. Instead, actual revenues for FY2025 were merely $102.3 million - a gap of over $15 million.

When one separates the disclosed performance of acquired businesses from the disclosed performance of AstroNova's legacy business, it appears that the legacy business (excluding Astro Machine and MTEX) experienced less than 5% cumulative organic growth from FY2019 - FY2022, and have since shrunk over 12% since the FY2022 peak, leaving revenues 8% below where they were in FY2019. Moreover, the revenue levels of both Astro Machine and MTEX are significantly below where they were expected to be at the time of acquisition, despite CEO Greg Woods claiming at the time of each acquisition that it was a strongly growing business:

(1) "In addition, Astro Machine has a track record of strong performance. Its relationships with market-leading customers have enabled Astro Machine to deliver consistent revenue and earnings growth. […] it's been growing very nicely. It had a very good 2019, still up a little bit in 2020. 2021 and 2022 have been up pretty sharply. The business has been growing. We dug into the financials really pretty deeply over the last six years. And except for a little down step in 2020, as a result of the surge of COVID, it's been growing pretty, pretty nicely. We've set a very strong track record of steady improvements over quite a number of years." [52]

(2) "MTEX provides us with complementary market adjacencies in our Product Identification segment that expands our addressable markets and broadens our global footprint, opening up significant top and bottom line growth opportunities. […] By combining the strength of our technology and go-to-market teams, we expect to see MTEX execute its aggressive growth objectives." [53]

This decline is even worse in "real," i.e., inflation-adjusted terms, when taking into account the substantial inflation that the global economy has experienced since 2019. According to a calculator by the U.S. Bureau of Labor Statistics [54] , a consumer would have to spend $127.45 in April 2025 to have the same buying power as a consumer spending $100 in January 2019. While it is impossible to practically determine the exact extent to which inflation has affected AstroNova's specific goods and services, the company has cited " risks from inflation and increasing market prices of certain components, supplies, and raw materials, which are incorporated into our end products or used by our suppliers to manufacture our end products." [55] Therefore, in real, inflation-adjusted terms, AstroNova has suffered an even greater decline in revenues in the Product Identification segment.

Let us now investigate some of the qualitative factors that may have contributed to these declining revenues, based on our extensive industry research.

2.2: Top of Funnel: Broken Lead-Generation Process Over-Reliant on Trade Shows

We believe that AstroNova's Product Identification segment has been heavily reliant on trade shows to generate leads, and has failed to evolve and adapt to a changing post-pandemic environment. CEO Greg Woods himself stated on the Q1 FY2021 earnings call that pandemic-related disruption to trade shows reduced new printer sales:

"[the] PI [Product Identification] segment relies heavily on trade show participation, in-person sales calls and product demos to generate demand. […] trade shows and other key marketing events […] have either been canceled, delayed until late in the year or changed to a virtual format. These market realities have negatively impacted our new printer sales." [56]

Mr. Woods frequently references trade shows. In May 2015, on the Q1 FY2016 earnings call, he referenced "the growing number of trade shows we attend each year." [57] In fact, our research tool (AlphaSense) indicates that the term "trade show" or specific names of shows such as Drupa, PackEXPO, Interpack, or Labelexpo have been used on dozens of calls:

FY2015 - Q1, Q2, Q3, Q4 calls

FY2016 - Q1, Q2

FY2017 - Q3, Q4

FY2018 - Q1, Q2, Q3, Q4

FY2019 - Q1, Q2, Q3, Q4

FY2020 - Q1, Q2, Q3, Q4, also three investor conference presentations

FY2021 - Q1, Q3, Q4, also three investor conference presentations

FY2022 - Q2, Q3, also six investor conference presentations

FY2023 - three investor conference presentations

FY2024 - Q1, Q2, Q3, also two investor conference presentations

FY2025 - Q1, Q2, and MTEX acquisition call

We believe that while trade shows and exhibitions were a valuable lead generation tool pre-COVID, and still have a role to play today, the world has changed and become far more digital, requiring a rebalancing - i.e., being more particular about which trade shows to attend, and how much is spent there, freeing up dollars to allocate to other marketing channels.

Unfortunately, AstroNova does not appear to have evolved or modernized its strategy. A former AstroNova sales manager, who was on the front lines with customers for twelve years, explained that AstroNova leadership shot down his attempt to modernize the lead generation process:

"I was vocal about the lack of leads, as we relied on exhibitions, which were shut down due to Covid-19. When exhibitions resumed, attendance was low. We hired an external agency for leads, but the results were poor. I advocated for online search engine optimization to improve our Google ranking, arguing that high-intent keywords would generate good leads. […]

I also did some cold calling, and we had another agency doing cold calling for us, which provided some leads, but the results were negligible. This led me to believe that we need to be where people are looking. That's the start, middle, and finish of this story. We need to be where people are looking.

Yes, you could go to exhibitions, but nine times out of 10, if you're a business wanting to print your own labels, what are you going to do in this day and age? You're going to Google it, right? […]

[My manager] and I both interviewed a candidate on Upwork [with experience in SEO or "search engine optimization"]. We pushed it, and it happened, but we were up against a marketing person […] [who] was the one stopping all of this. It was challenging because we weren't allowed to proceed, and the marketing lady [locally] […] was on board, saying we needed to be where people are." [58]

According to the sales manager, his vocal advocacy for modernizing the lead-generation approach may have contributed to the company's decision to eliminate his role:

"I think I ruffled some feathers, and they decided to make me redundant. I had the choice to return to media sales or take my severance. I chose the severance and moved on." [59]

We spoke to this individual's manager as well - the sales director for a major geographic region. He echoed similar sentiments and noted what he perceived as a lack of basic marketing analytics such as calculation of the cost per lead and the conversion rate:

"I think A) trade shows are outdated […] they're not just outdated, they are also extremely expensive when you're looking at the cost per lead really, just because you have all the cost of the booth, you have the travel expenses of the reps, and all that stuff. It's fairly expensive for the few number of leads you can generate. […]

In a nutshell, it was not just me, it was also our VP [of] Sales saying exactly the same thing. He put quite some emphasis on getting batch budgets allocated to SEO, SEA [search engine advertising], and so on, but it was never really done in a consequent[ial] manner. At the end, it always was "Well, no, we had so much success in the past with the trade shows. Let's do that right." You wouldn't believe how often I heard the sentence, "Well, now since the world has opened up again, we should go more to trade shows. Just do what we have always done successfully." It was really an endless discussion. I think you named it. It really comes from the top of the company really, I have to say that. […]

I think one thing AstroNova is not really good at is really monitoring the efficiency of their marketing tools. I think it's still today, probably. You can ask that question directly, but I'm pretty sure no one knows how much a lead cost generated from online versus trade shows and how successful they are, what the closing rates are and so on. I think no one really cares. They're just looking at the past and remembering back in the good old days, what all went well and what were successful and just copy-paste that into the future. I don't believe that does work." [60]

A former executive at Domino Printing echoed this insight for the industry writ large, calling trade shows the "dinosaur approach." He discussed Domino's success in reallocating some trade show spend to channels such as social media and thought leadership:

"[Trade shows] are quite old-fashioned, aren't they? I used to dislike trade shows. It's all digital marketing now. It's easy to fall into the dinosaur approach, thinking that what worked for 30 years will continue to succeed. Social media platforms like LinkedIn and Facebook are good for generating new leads. It might be outside AstroNova's comfort zone, but in Indonesia, I was amazed at how WhatsApp and LinkedIn are used as business tools. We redirected a lot of the marketing spend from a big booth at the Jakarta show into social media and thought leadership across the business." [61]

There are a number of nuances here; for example, we do believe that industry-specific trade shows for new/emerging industries are still a valuable way to introduce labeling solutions to customers who may not have an existing labeling solution. We further believe that having some presence at large print-industry trade shows is an important branding endeavor.

However, we think large, expensive booths at print-industry shows such as Drupa represent a low-ROI use of shareholder capital. Indeed, we earlier discussed AstroNova's FY2025 Product Identification revenue shortfall in both the "legacy" business and the acquired MTEX business. Reported revenue declines stand in stark contrast to CEO Greg Woods' excitement on the Q1 FY2025 earnings call in June 2024 about Drupa:

"The large combined AstroNova MTEX booth at Drupa was the perfect venue to showcase the broad range of groundbreaking products and solutions. Congratulations to our marketing teams for pulling out all the stops […] Since the Drupa show opened on May 28, attendees have been flocking to the booth to see the AQUAFLEX in action, along with the other new products from MTEX and AstroNova. We collected hundreds of high quality leads as well as several orders at the show. We even closed deals to sell some of the printers right off the floor in our booth, including the two you see in slide 6." [62]

These "leads" and "deals" failed to drive growth in FY2025, so perhaps the time and effort spent at Drupa was unproductive. If AstroNova is slow to adapt to decade-old best practices such as search engine optimization and social media marketing - and the Board has failed to prioritize modernization - it speaks poorly to incumbent Board members' ability to assess and adapt to important evolving threats and trends such as cybersecurity and artificial intelligence.

2.3: Lack of Clear Customer, Market, and Channel Segmentation: Incoherent Go-To-Market Strategy

As discussed in Section 1, AstroNova's product portfolio now ranges from small tabletop models that cost a few thousand dollars and serve low-volume applications, all the way up to models costing hundreds of thousands of dollars targeting high-volume applications.

It is intuitively obvious that the optimal approach for selling a sub-$5,000 table-top printer to a small or medium business will be vastly different from selling a $300,000 machine to a larger organization. A former Senior Vice President at Memjet bluntly observed that AstroNova appeared "not quite sure what they are" and lacked the "clear, focused strategy" that allowed companies such as Afinia to outcompete AstroNova despite far fewer resources. He also observed that AstroNova was sometimes competing with its own resellers:

"AstroNova wasn't able to cover the whole U.S. market, European market, or Asia market. Let's just say Europe and the U.S., and introducing coverage through partners, if it's either a reseller channel or some form of channel to the market, that's the way.

I think if you look at Afinia as a small, privately owned business and look at where they operate, they have a smaller portfolio of products. […] [T]hey do a really good job of only working with resellers. It's because they have a very clear, focused strategy. That's what I didn't see at AstroNova. They tried to go through the channel, that didn't work. They tried again, and I think they are struggling to grow because they're not quite sure what they are. Do we direct-sell? Do we direct-sell, and do we also sell, for example, through resellers where we don't have coverage? If we do that, do we have a very clear separation so that our resellers don't think we're trying to take the lucrative deals off the table directly? I think that's the feedback I heard from resellers, right or wrong. Their commentary was, "Hey, I'm not really sure if these guys are supporting me long-term because I just see too much. They're doing it one minute and then not the next."

I think adopting new methods to generate demand was moving away from trade shows. Using social media in a much more dynamic way, I think that was something slow to be done, and it didn't seem like there was somebody really owning that clearly at AstroNova, other than Greg wanting to own the marketing strategy side of things. I think their ability to grow a reseller channel has been compromised. They've struggled to really, even as a public company, with the resources they've got, outcompete on the channel marketing skills of somebody like an Afinia, as an example." [63]

A former Managing Director of OKI Europe provided further context on several ways in which AstroNova's channel sales approach left much to be desired. He discussed a bizarre situation in which AstroNova purchased white-labeled printers from OKI Japan, then sold them in Europe at prices lower than OKI themselves were selling the same product, at the same time as AstroNova was trying to partner with OKI to develop client accounts, working with OKI sales reps who then switched the customer back to higher-priced product from OKI, cutting out AstroNova:

"[L]et's say if an OKI salesperson sold the product for 100, AstroNova would go into the same dealership, if they had a contract, and sell the product for roughly €70 or dollars, about 30% below the pricing Europe was used to. […]

The idea was that AstroNova would open larger accounts with our product and their other products, and then take our sales rep to the customer to assist. But it's a no-brainer; that wasn't really set up properly because our sales rep would try to switch the customer to an OKI original product. So, the AstroNova guy never took us anywhere, and the OKI guys were trying to defend against AstroNova." [64]

It is difficult to know exactly where to start criticizing this completely dysfunctional go-to-market strategy, which seems like a waste of time and resources for everyone involved. More broadly, this Managing Director at OKI was critical of what he perceived as AstroNova's over-reliance on a direct sales approach and underdevelopment of broad, deep channel-partner relationships. He referenced something that has parallels to the poor cultural fit at MTEX - different geographies in Europe have different languages and cultures, and thus having a local partner can be critical to success:

"To me, AstroNova is a company trying to implement a direct approach model in Europe. This might work for certain business segments, but Europe is more channel-oriented, relying on third parties like dealers, resellers, and distributors. I'm not sure if AstroNova will succeed in this market. In my 30 years in the printing business, I've learned that the majority of business is conducted through the channel. […]

Different markets may require different strategies, especially since AstroNova's product isn't disruptive and doesn't dominate the market. You need to adapt to the channel, even if it's direct. In another country, you need someone you can trust and listen to. As a European and native German, I see a stark contrast between sales channels in Germany and Italy. Italian sales channels are much smaller, reflecting their GDP, which is one-third of Germany's. Can the strategy be the same? Yes, but it must be adapted. In my opinion, AstroNova could improve in this area. […]

Europe is much more fragmented. When I think about copier resellers I visited with Lexmark in the US, they are massive. In Germany, even the biggest copier resellers are not half the size. This means you need more resellers to achieve the same revenue momentum. You can't just send one person to a reseller to discuss a deal or warehouse stock and then leave. You need to ensure that this reseller isn't competing against others. You need more strategic thinking in such a marketplace to attract a specific reseller to achieve their goals." [65]

In addition to better managing its channel partner relationships, we also believe that as a smaller, niche player in industrial printing, AstroNova should do a better job of identifying and targeting the most profitable customer segments. Some background is relevant. AstroNova's products have historically succeeded by offering customers a solution for "short runs."

Historically, large commercial printers used analog machines that required physical plates, so it was impossible for them to cost-effectively service small label runs. Long runs work fine for a producer of a high-volume, low-mix product like cornflakes or flour, where customers need millions of identical labels. But for low-volume, high-mix products - for example, a craft brewery, small winery, or local ice-cream maker with many rotating flavors - this model was impractical. According to numerous people we interviewed, including a former Sales Director at AstroNova, AstroNova's QuickLabel and TrojanLabel product lines were early movers in the short-run space and successfully addressed an untapped market opportunity. [66]

Unfortunately, this sales leader (as well as others) mentioned that the industry has become more competitive; for example, the advent of digital printers has allowed certain traditional commercial printers, as well as new web shops, to more cost-effectively service short-run orders, and others have developed products addressing AstroNova's market segments. [67] As the former SVP at Memjet put it:

"The market dynamic, I think, is a bit sharper and has moved on. I think that's one of the areas which has created competitive pressure." [68]

A TrojanLabel customer confirmed the increasingly competitive environment:

"There's more competition and companies can meet our needs. […] AstroNova recently showed me a new printer, but it didn't seem special. I haven't delved deeply into it to be honest. […] Afinia contacted me recently about a new printer they're launching." [69]

Despite the increased competition, we believe the industry overall is growing. The former SVP at Memjet, as well as a former executive at Domino, suggested growth rates of 4 - 6% or higher, although it varies by segment, geography, and many other factors. [70] Nonetheless, the industry's positive organic growth rate contrasts with the previously-discussed organic revenue declines that AstroNova has suffered in the past several years.

Our conversations lead us to believe that there are numerous opportunities which AstroNova could take better advantage of to drive organic growth. The first is segmenting their markets into different industries, or "vertical markets," and trying to become a leader for those specific applications, rather than simply applying a generic marketing strategy. A former executive at much larger peer Domino Printing explained how Domino utilized solutions-based selling in vertical markets to achieve substantial success - and "double or triple" margins - by becoming the de-facto standard for specific applications of individual customer segments:

"Domino has been incredibly successful in certain niche sectors over the years. For example, 20 years ago in the UK, we got involved in potato bagging. It was retailer-driven when a supermarket asked potato farmers to include traceability codes to show customers the county their potatoes came from.

We capitalized on that, and soon, other retailers followed. This became a multi-million-pound business annually, with excellent margins, selling to potato farmers. […]

By differentiating yourself and becoming a specialist, you can double or triple your margins. Domino was very successful in the tobacco sector, despite it not being politically correct. We became the de facto standard, with the big four tobacco manufacturers seeking our advice on legislation compliance. This pushed Domino's development of certain technologies, strengthening our position and margins." [71]

Our plan includes utilizing tools such as "voice of customer" to drive targeted new product introduction and marketing, in line with this best practice the Domino executive describes. Similarly, the former SVP at Memjet discussed how one AstroNova salesperson on the West Coast achieved strong results through a focus on the cannabis market, including social media investment, but subsequently left because of a lack of organizational support:

"I spoke to some of the higher-performing sales folks, one particular person out on the West Coast who was very, very successful before they left the business because they felt that there wasn't really a career development path for them. They really tapped into the growth of the cannabis market. They happen to be in the right geography, but they started doing some of their own very simple social media. I think that's an area of investment which seemed to pass by on AstroNova." [72]

We believe a second path to improving revenue growth and margin performance is through a different approach to quality and customer service, which we will discuss below.

2.4: Quality and Customer Service: Viewing Labels Through A "Low Cost, High Cost of Failure" Lens

In the industrial sector, we (Askeladden) have historically sought out companies that fit into a mental model we call "low cost, high cost of failure." We like to find companies which sell an inexpensive component that is nevertheless mission-critical to customers, such that if the component fails (or is not available), customers suffer extremely high costs that dwarf the cost of the component in question.

We believe that labels fit neatly into this model. (We note that much but not all of AstroNova's Product Identification business is attributable to labels - some is attributable to printing on other media types such as cardboard - but a full analysis of every product line would be beyond the scope of this analysis, so we choose to focus here on labels.) The cost of an individual label is measured in pennies, representing a tiny fraction of the cost of goods such as a bottle of wine, a carton of ice cream, or a bag of coffee. Imagine a $20 bottle of wine or an $7 carton of ice cream: if the label costs a few pennies more or less, it would not substantially affect the price of the end product, or the profit margins of the producer.

However, without that few-cent label - a relatively de minimis expense - the product cannot be sold. Imagine a bottle of wine, or a bottle of medicine, without a label. Consumers will not be able to identify the product. Regulatory requirements such as nutritional information or pharmaceutical disclosures will not be met, and so on. Without a label, a product would not be accepted by any retail partner, nor could it be sold to a consumer directly.

A TrojanLabel customer to whom we spoke agreed with our assessment that labels are a low-cost, high-cost-of-failure product. He referenced how during one of their peak sales periods - the lead-up to Christmas and the holidays - his business was severely impacted by a quality failure on the part of AstroNova. His business " had to shut down production for a week because we didn't have labels." [73]

This customer stated that with his large variety of individual products and preferred just-in-time inventory management practices, he had evaluated web-shops that could produce labels for him, but he still finds substantial value in doing things in-house:

"The biggest problem is lead times. I want things now, not in two weeks. That drives our business model to do it in-house, just in time."

The week we were speaking to him, he once again faced quality issues with AstroNova label media. A recent large batch of labels were misaligned on the roll of backing material (rendering them unusable). Simultaneously, the roll did not have sufficient tension for the printer to unwind it. The customer explains how this has become a "high cost of failure" situation for his business:

"We've been having increasing problems with AstroNova recently. In fact, just 20 minutes before you called, I was dealing with an [existential] problem due to an AstroNova issue. We have 400,000 unusable labels and nothing left for next week. Imagine having a warehouse that's about to shut down. […]

[This issue] first surfaced a year and a half or two years ago, got fixed, and then randomly unfixed again […] This has happened multiple times. Now, I'm left with no labels, and I have a busy warehouse behind me. I'm in trouble. Next week, I have nothing to print. I don't know what we're going to do or how we'll figure that out over the weekend." [74]

The customer told us that he was fortunately not impacted by the FY2022 - FY2024 ink quality issues we discussed earlier in this document, but he did state that "day-to-day minor printing errors" are commonplace:

"We're used to dealing with white lines now. It's annoying, to be honest, because it requires unnecessary time. My team checks the rolls every few minutes to prevent large streaks, which would waste the entire run. Over the years, we've learned what works and when to clean it.

We only call AstroNova for more extensive problems, like when the printer isn't working, won't switch on, or shows unfamiliar errors. For day-to-day minor printing errors, we accept them as part of the machine's limitations."

The customer had positive feedback for his local sales and support team, but explained that things broke down whenever he needed to escalate an issue up the chain:

"I view AstroNova as fine until there's a problem. When there's a problem, my assumption, whether fair or not, is that I'm not going to get any help. […]

It's definitely gotten worse. The woman [here locally] is good. She's very capable and will deal with the problems, but she often has to escalate issues, and that's where the chain of communication seems to break down. In the past, when I first dealt with AstroNova, there were multiple people [locally], but they've all left. Back then, I had a few contacts I got to know who had strong relationships with the [regional] teams. Now it just seems like this poor lady is on her own, and I haven't been able to speak to any of the [regional leaders] in a long time."

The customer did tell us that price matters to him - costs do add up given the quantity of labels he prints - but also told us that if he was in AstroNova's position, he would have raised prices, which he said AstroNova has not done to a material degree. Based on our conversation, he appears to be considering replacing his TrojanLabel machine with a competing product in the next few years. He explains his evaluation of competitors is due less to price and more to his lack of a relationship with AstroNova, and the many quality and reliability issues he has faced:

"I'm a loyalty-based buyer and value the relationships with my suppliers. I return to good ones even if I pay more because, in business, ups and downs happen. Honestly, I don't have a relationship with AstroNova. I'd cherish one and do more business with them if I did. But without that relationship, there's no loyalty to rely on when problems occur […]

They sent an incorrect supply, and the previous batch was unusable. We've gone from 400,000 to zero labels in a matter of days. Situations like this are stressful and pose a major risk. Can I afford for this to happen again? Incidents like this incentivize business owners to explore other options. It doesn't mean I'm necessarily going to switch, but […] these are the factors that drive people to look at alternatives. […] Everyone's competing for my business. I haven't had to look so far, but I am aware there are new models in the market. For me, it's about the right time to make that move."

While this is just one customer experience, it is echoed by others to whom we have spoken. For example, this customer referenced conversations with his sales representative - the 12-year tenured AstroNova sales manager we previously quoted. The customer explained:

"I think he [the sales representative] had a lot of frustration with AstroNova, as I remember it. Every time we called, it was me complaining, and he'd say, "Don't worry, you're not the only one today."

The former sales representative's frustration was evident when we spoke to him - he was clearly very passionate about AstroNova's business and the customers he served, but expressed to us that we were the first people, other than his wife, to take his concerns seriously:

"This is the first time I've had a chance to express my frustration in two or three years. My wife has heard this story repeatedly. I'm not trying to undermine anyone; I [was] with the company for 12 years. I love[d] what I d[id], but they need to make changes. I [was] tired and unsure of what to do." [75]

In addition to the publicly-disclosed 2022-2024 ink quality issues, a former quality manager at AstroNova - who has subsequently been hired at two other companies as a VP/Director of Operations - explained his frustration with AstroNova's quality culture. In the quote below, he discusses quality concerns that we believe primarily refer to the Aerospace side of the business (rather than Product Identification). However, with that caveat, his comments on AstroNova's cultural lack of focus on quality certainly fit the fact pattern we have been discussing:

"At the end of every month, every quarter, if there were quality issues, they certainly did their best but when it came down to making a shipment for revenue, that was priority and that was the culture. […] If it was not functioning, they wouldn't ship it but if it was functioning even marginally, it was a shipment, it was going. […] As I explained, I'm not there anymore, that's why. That's a big part of it." [76]

We believe this apparent short-term focus on maximizing current-month revenues at the expense of quality is misguided and a poor way to do business. We believe that AstroNova should take advantage of its enviable position of being a low-cost, high-cost of failure product. As a smaller, niche player, AstroNova does not have to serve all customers or market segments, the way a billion-dollar company might. Rather, it can pick and choose which customers to serve. We believe that the subset of customers who are less focused on an incremental penny or two of cost per label - who instead value a long-term partnership and the peace of mind that comes with a reliable supply of quality labels - are likely to be far more profitable.

Particularly given its annuity-like revenue stream of consumables, we believe that AstroNova should be focused on delighting its customers, delivering an unparalleled quality and service experience, with a fanatical focus on customer support. Labels are not the core business for most of AstroNova's customers, but they are a critical component that can hold up production and prevent sales of tens or hundreds of thousands of units - potentially worth millions of dollars. We believe that AstroNova should implement best practices utilized by other annuity-like businesses, such as software subscriptions, to measure their lifetime customer value and maximize retention and customer satisfaction to drive repeat hardware purchases and an extension of the lifetime of the lucrative installed base. This is why we have used the term "solutions-based selling" - we believe AstroNova should not think of themselves as selling a label printer; they should think of themselves as the sector-specific label experts, selling customers a solution to their labeling needs, so that those customers can focus on their core business and never have to worry about labels again.

Being a low-cost provider can certainly be a good business strategy. However, in the case of AstroNova, we believe that a differentiation strategy is superior to a price-focused strategy for several reasons. First, AstroNova does not have a proprietary low-cost source of ink; it is not a manufacturer of ink. Instead, it relies on third party ink providers, which other industry participants could also purchase from. Therefore, if AstroNova competes on price, it may attract more transactional customers who will leave for competitors if those competitors offer lower prices. Second, as a smaller, niche player, AstroNova likely does not have the economies of scale and negotiating power enjoyed by large global companies such as HP or Domino.

Conversely, as we mentioned, even Domino has seen success by focusing on differentiation within product niches: "By differentiating yourself and becoming a specialist, you can double or triple your margins." [77] We believe that if AstroNova builds customer trust and loyalty - as described by the TrojanLabel customer - then competitors will have a hard time overcoming customers' long-term relationship with AstroNova. We believe a certain segment of customers will prioritize reliability for a relatively low-cost but mission-critical component (labels), even if a competitor develops a lower-cost or technologically-superior product, or is simply willing to accept lower margins to undercut AstroNova and steal business.

SECTION 3: WHO CAN BETTER ADDRESS THESE PROBLEMS - INCUMBENTS, OR ASKELADDEN'S NOMINEES?

We believe that this extensive analysis should demonstrate to shareholders that AstroNova's CEO and Board of Directors have made many questionable strategic decisions that have contributed to the poor financial results and shareholder value destruction that has occurred in recent years.

Shareholders should then ask: who is most capable of addressing and resolving these issues? The incumbent CEO and Board that created the mess in the first place? Or a carefully selected team, nominated by AstroNova's largest shareholder, which offers specific, relevant, and complementary expertise to address the challenges that our company faces today?

3.1: Incumbent Directors

AstroNova's incumbent Board is comprised of six directors. Of these, all but Mr. Nevin and Mr. Michas have served as Board members for at least 7 years, thereby overseeing the company's failed strategy:

CEO Greg Woods. CEO Greg Woods is the architect of the company's current strategy, which has clearly served shareholders poorly. From February 1, 2014 (when Mr. Woods became CEO) through May 15, 2025 (the record date of this year's Annual Meeting), AstroNova shares have experienced a total return of negative 28%. We believe that it is absolutely critical for Mr. Woods to be removed from the Board and replaced with someone who can more objectively evaluate Mr. Woods' decisions.

Lead Independent Director Richard Warzala. Mr. Warzala has also been a director since 2017. While Mr. Warzalahas recent executive experience at Allient (ALNT), Mr. Warzala and Mr. Woods both worked at Buffalo, NY based American Precision Industries (API) in the mid to late 1990s, through its subsequent acquisition by Danaher. Mr. Woods' final role was President, API Controls while Mr. Warzala's was President, API Motion. [78] [79] We believe that Mr. Warzala's relationship with Mr. Woods, dating back to the 1990s, represents a potential conflict of interest, and may reduce the extent to which Mr. Warzala exercises objective judgment to hold Mr. Woods accountable for his poor performance.

Mitchell Quain. Mr. Quain has been a director since 2011 and was thus part of the Board that appointed Mr. Woods CEO. According to AstroNova's proxy materials, [80] Mr. Quain does not appear to have held any direct operating roles since the COVID pandemic. Given the rapid evolution and digitization of many industries during this time, we believe Mr. Quain may lack hands-on knowledge of key, important trends affecting businesses today.