Financial News

Wells Fargo: Investor Optimism Sheds Seven Years of Gains in Last Quarter

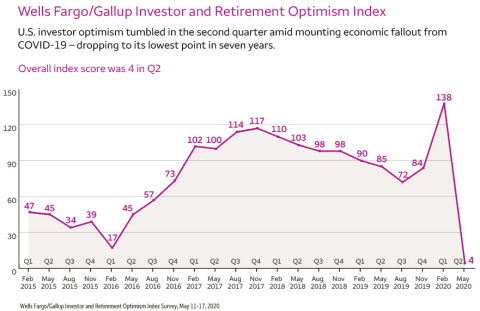

After reaching a 20-year high in the first quarter, U.S. investor optimism tumbled in the second quarter amid mounting economic fallout from COVID-19. The Wells Fargo/Gallup Investor and Retirement Optimism Index, based on interviews conducted May 11-17, is now the lowest it has been since the fourth quarter of 2013. Yet even as investors’ 12-month outlook for their own investments is down sharply, most remain optimistic about reaching their five-year investing goals.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20200624005205/en/

Wells Fargo/Gallup Investor and Retirement Optimism Index (Graphic: Business Wire)

“Investors are displaying remarkable resilience at an unprecedented time,” said Tracie McMillion, head of global asset allocation strategy for Wells Fargo Investment Institute. “Numerous trends in the poll confirm that investors view recent market disruption as episodic and temporary, not as a sign of systemic problems that will harm their investments in the long term or compel them to reallocate their assets.”

Investor optimism index suffers record decline

The Wells Fargo/Gallup Investor and Retirement Optimism Index fell 134 points this quarter to +4. This is by far the largest short-term drop for the index since its inception in 1996. Investor optimism dropped this quarter on all economic components of the index. However, consistent with the latest federal employment reports, optimism fell the most on unemployment (down 34 points), followed by economic growth (down 26 points).

On the personal items that make up the index, investors’ outlook for reaching their 12-month investment targets also fell sharply this quarter (down 32 points). At the same time, their longer-term outlook is intact, as two-thirds remain optimistic about reaching their five-year investment goals.

Fundamental confidence in stock market unshaken

Despite this quarter’s unprecedented drop in the investor index, six in 10 investors continue to say now is a good time to invest in the financial markets.

Nearly seven in 10 investors currently feel very (21%) or somewhat (48%) confident about investing in the stock market as a way to build wealth for retirement. This percentage is unchanged from a year ago. Just 8% of investors see the current stock market environment as a time to decrease their stock holdings to protect against further losses. About half say it’s a time to hold what they have and wait for the market to come back, while 35% see it as a buying opportunity.

Thinking about the market outlook for the rest of 2020, about half of investors, 51%, are optimistic that the worst is behind us; 49% say the worst is yet to come.

Impact of COVID-19 on financial and retirement security

Investors have not been unaffected by the effects of COVID-19 on the job market. As of the May survey, 27% of nonretired investors had suffered a loss of income or pay, 15% had been furloughed or temporarily laid off, and 1% had been permanently let go.

The coronavirus has also compelled one in four investors to take on more financial responsibility for family members. The largest percentage, 16%, reports providing greater financial assistance to an adult child, while 7% say they have assisted a parent, and 7% another relative.

On the plus side, the economic shutdown has caused most investors (64%) to spend less money than usual, and as a result, one-third say their savings increased during this period. A smaller percentage, 21%, say their savings decreased, while 46% say their ability to save has not changed.

Overall, about a third of all investors (32%) report that the economic disruption caused by the coronavirus has had a negative impact on their day-to-day financial security. This percentage includes 28% of retired investors and 35% of nonretired investors.

Looking ahead, 30% of employed investors say it’s very or somewhat likely they will delay the age at which they retire as a result of the recent economic downturn. A similar percentage, 29%, think it’s likely they will work more than they intended in their retirement.

The impact of the downturn has been especially pronounced on employed investors who are closer to retirement age — those aged 50 to 64. Forty percent of this group, compared with 22% of investors aged 18 to 49, says they are very or somewhat likely to work more than they intended to in retirement as a result of the market downturn. Older, nonretired investors are also more likely than those under 50 to say they will have to retire later than they originally planned.

“Feeling compelled to extend working years to offset losses is something many investors wrestle with — though it’s not always necessary,” said Dan Barry, regional president of Wells Fargo Advisors’ Gateway Region. “As history has shown, assets in a carefully constructed investment strategy often recover if you refrain from making emotional decisions. It’s about prioritizing what is most important, centering your investment strategy around these priorities, and making informed decisions.”

2008-2009 downturn may have helped strengthen investors’ nerves

Three in four investors say they were invested in the stock market in 2008, another year of significant market turmoil. Fewer than half of these investors (42%) say they are more concerned about today’s market downturn than they were about the downturn in 2008. Rather, the majority feel the same level of concern (28%) or less concern (30%).

At the same time, four in 10 investors, including 46% of those who were invested in the market in 2008, say they have gotten better about shrugging off market volatility. Another 31% say they were not bothered by market volatility before. One in four say they are bothered as much today as they were during the 2008-2009 downturn.

Saving and financial planning are top lessons learned from COVID-19

A majority of investors (64%) say setting aside more money in an emergency fund is a change they would make to their financial or investing strategy as a result of the coronavirus. Close to half say they are very or somewhat likely to spend more time creating a long-term financial plan.

“Whether it is the coronavirus or any other catalyst, market downturns are inevitable. It is a matter of when, not if they will happen,” said Barry. “Having a comprehensive, long-term investment plan is critical to effectively weathering market downturns and preparing for the ‘what if’s’ of retirement,” Barry said.

Read the Wells Fargo Investment Institute Midyear Outlook: Recession, Recovery and Resilience.

Watch a Wells Fargo Stories video with McMillion about the survey findings.

About the Wells Fargo/Gallup Investor and Retirement Optimism Index

Results for this Wells Fargo/Gallup Investor and Retirement Optimism Index are based on a Gallup Panel™ web study completed by 1,076 U.S. investors, aged 18 and older, from May 11-17, 2020. The Gallup Panel is a probability-based, longitudinal panel of U.S. adults who Gallup selects using random-digit-dial phone interviews that cover landline and cellphones. Gallup also uses address-based sampling methods to recruit Panel members. The Gallup Panel is not an opt-in panel. The sample for this study was weighted to be demographically representative of the U.S. adult population, using the most recent Current Population Survey figures. For results based on this sample, one can say that the maximum margin of sampling error is ±5 percentage points at the 95% confidence level. Margins of error are higher for subsamples.

In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error and bias into the findings of public opinion polls.

For this study, the American investor is defined as an adult in a household with stocks, bonds, or mutual funds of $10,000 or more, either in an investment account or in a self-directed IRA or 401(k) retirement account. About two in five U.S. households have at least $10,000 in such investments. The sample consists of 67% nonretirees and 33% retirees. Of total respondents, 40% reported annual incomes of less than $90,000; 60% reported $90,000 or more. The median age of the nonretired investor is 45 and the retiree is 69. The Wells Fargo/Gallup Investor and Retirement Index is an enhanced version of Gallup’s Index of Investor Optimism, which provides the historical trend data.

The Investor and Retirement Optimism Index has an adjusted baseline score of 100 from when it was established in October 1996. It peaked at +152 in January 2000, at the height of the dot-com boom, and hit a low of -81 in February 2009.

About Wells Fargo

Wells Fargo & Company (NYSE: WFC) is a diversified, community-based financial services company with $1.9 trillion in assets. Wells Fargo’s vision is to satisfy our customers’ financial needs and help them succeed financially. Founded in 1852 and headquartered in San Francisco, Wells Fargo provides banking, investment and mortgage products and services, as well as consumer and commercial finance, through 7,400 locations, more than 13,000 ATMs, the internet (wellsfargo.com) and mobile banking, and has offices in 32 countries and territories to support customers who conduct business in the global economy. With approximately 260,000 team members, Wells Fargo serves one in three households in the United States. Wells Fargo & Company was ranked No. 30 on Fortune’s 2020 rankings of America’s largest corporations. News, insights and perspectives from Wells Fargo are also available at Wells Fargo Stories.

Additional information may be found at www.wellsfargo.com | Twitter: @WellsFargo.

Investment and insurance products: | ||||

NOT FDIC-Insured | NO Bank Guarantee | MAY Lose Value | ||

Wells Fargo Advisors is a trade name used by Wells Fargo Clearing Services, LLC, Member SIPC, a registered broker-dealer and non-bank affiliate of Wells Fargo & Company.

Wells Fargo Investment Institute, Inc. is a registered investment adviser and wholly-owned subsidiary of Wells Fargo Bank, N.A., a bank affiliate of Wells Fargo & Company.

View source version on businesswire.com: https://www.businesswire.com/news/home/20200624005205/en/

Contacts:

Allison Chin-Leong, 212-214-6674

allison.chin-leong@wellsfargo.com

Desari Mueller, 314-327-9615

desari.mueller@wellsfargoadvisors.com

Stock quotes supplied by Barchart

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the following

Privacy Policy and Terms and Conditions.