Financial News

J. M. Smucker (NYSE:SJM) Reports Q2 In Line With Expectations

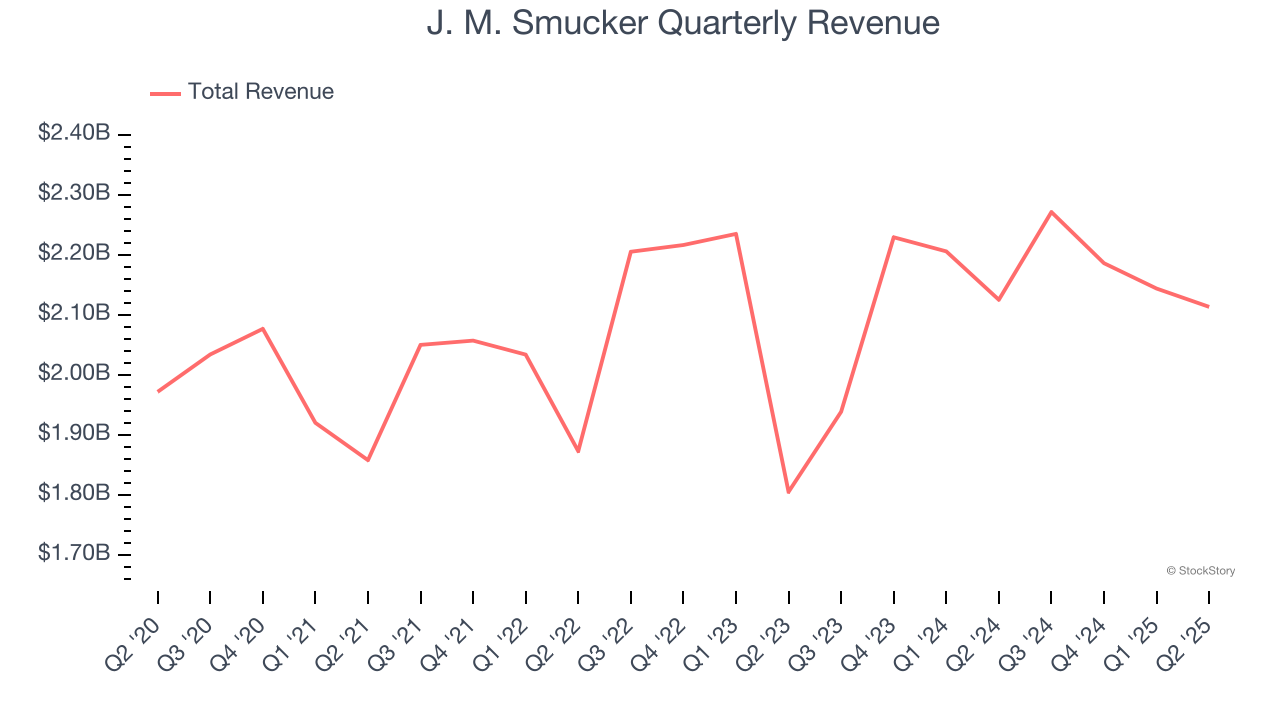

Packaged foods company J.M Smucker (NYSE: SJM) met Wall Street’s revenue expectations in Q2 CY2025, but sales were flat year on year at $2.11 billion. Its non-GAAP profit of $1.90 per share was 1.4% below analysts’ consensus estimates.

Is now the time to buy J. M. Smucker? Find out by accessing our full research report, it’s free.

J. M. Smucker (SJM) Q2 CY2025 Highlights:

- Revenue: $2.11 billion vs analyst estimates of $2.12 billion (flat year on year, in line)

- Adjusted EPS: $1.90 vs analyst expectations of $1.93 (1.4% miss)

- Adjusted EBITDA: $178.9 million vs analyst estimates of $436.9 million (8.5% margin, 59% miss)

- Management reiterated its full-year Adjusted EPS guidance of $9 at the midpoint

- Operating Margin: 2.2%, down from 16.4% in the same quarter last year

- Free Cash Flow was -$94.9 million, down from $49.2 million in the same quarter last year

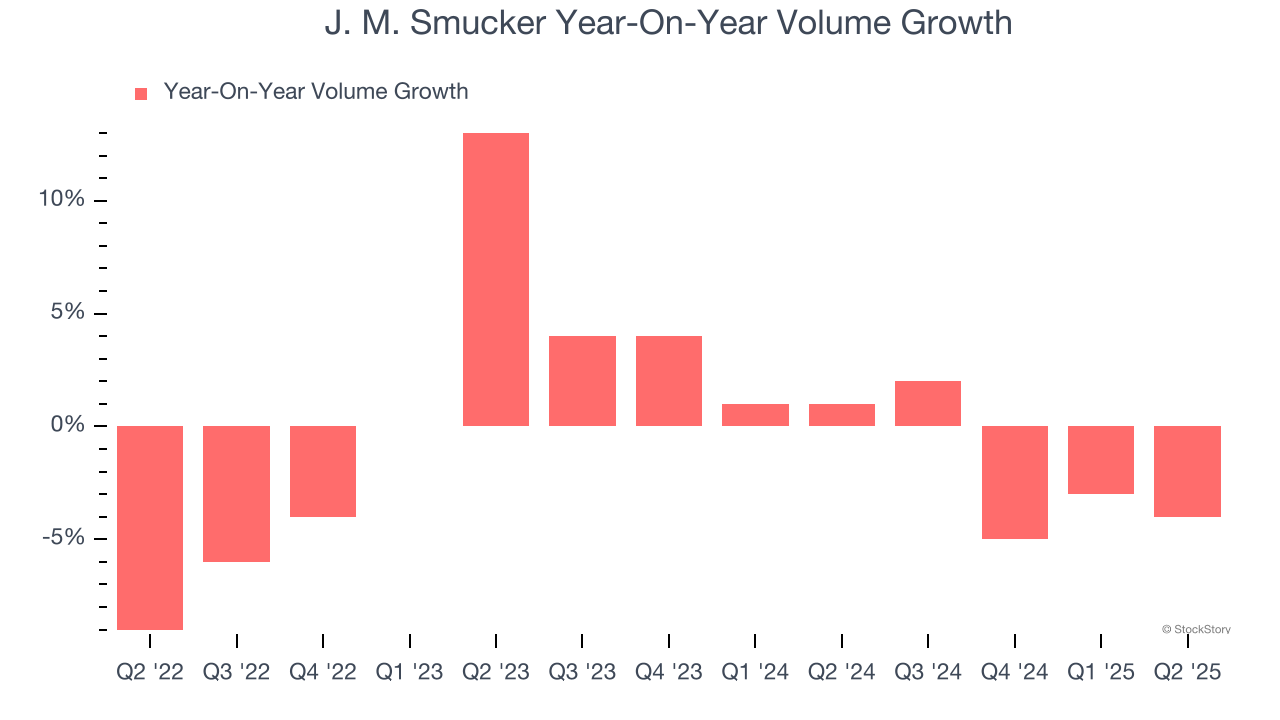

- Sales Volumes fell 4% year on year (1% in the same quarter last year)

- Market Capitalization: $11.8 billion

"Our first quarter results exceeded our expectations and reflect the continued momentum of the business. Our teams demonstrated agility throughout the organization, and though the external environment continues to be dynamic we are successfully managing what we can control," said Mark Smucker, Chief Executive Officer and Chair of the Board.

Company Overview

Best known for its fruit jams and spreads, J.M Smucker (NYSE: SJM) is a packaged foods company whose products span from peanut butter and coffee to pet food.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $8.71 billion in revenue over the past 12 months, J. M. Smucker is one of the larger consumer staples companies and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because there are only a finite number of major retail partners, placing a ceiling on its growth. To accelerate sales, J. M. Smucker likely needs to optimize its pricing or lean into new products and international expansion.

As you can see below, J. M. Smucker’s 2.8% annualized revenue growth over the last three years was sluggish. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

This quarter, J. M. Smucker’s $2.11 billion of revenue was flat year on year and in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 4.1% over the next 12 months, similar to its three-year rate. Although this projection indicates its newer products will fuel better top-line performance, it is still below average for the sector.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

J. M. Smucker’s quarterly sales volumes have, on average, stayed about the same over the last two years. This stability is normal because the quantity demanded for consumer staples products typically doesn’t see much volatility.

In J. M. Smucker’s Q2 2026, sales volumes dropped 4% year on year. This result represents a further deceleration from its historical levels, showing the business is struggling to move its products.

Key Takeaways from J. M. Smucker’s Q2 Results

We struggled to find many positives in these results. Its EBITDA missed and its gross margin fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 4.9% to $105 immediately following the results.

J. M. Smucker’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.

More News

View More

Recent Quotes

View MoreQuotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.