Financial News

Prospect Capital (NASDAQ:PSEC) Posts Q2 Sales In Line With Estimates

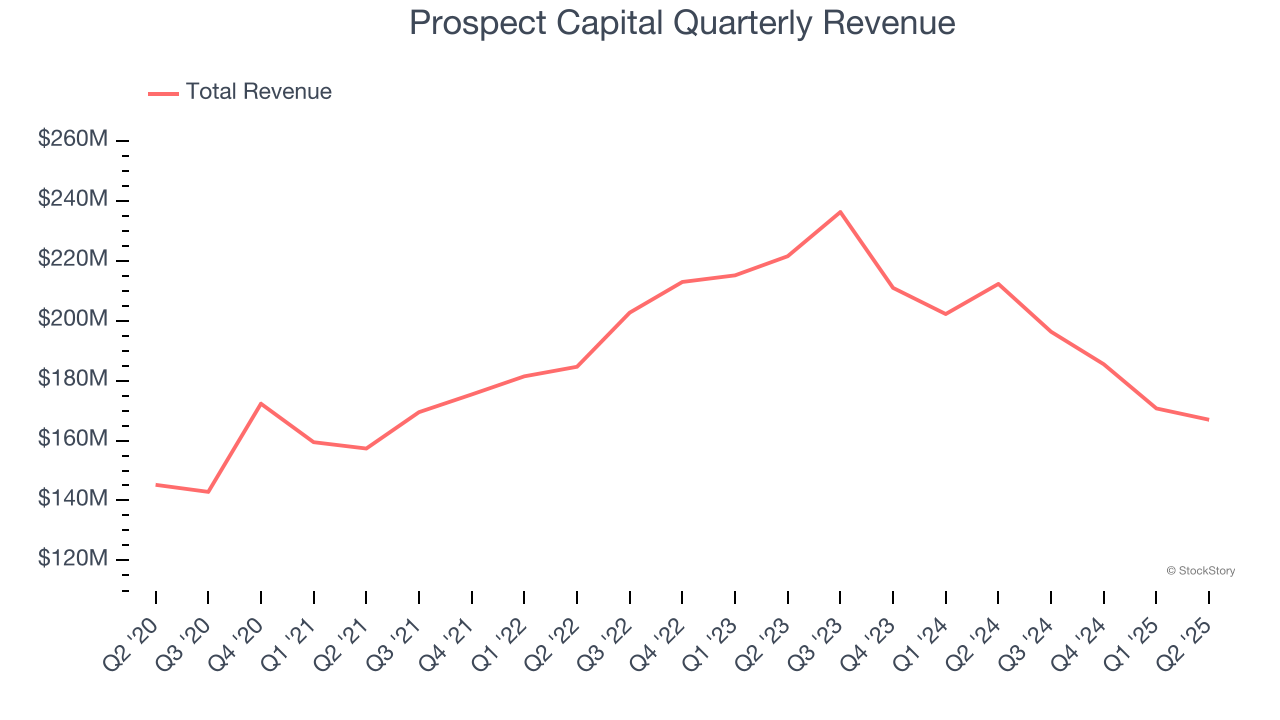

Business development company Prospect Capital (NASDAQ: PSEC) met Wall Street’s revenue expectations in Q2 CY2025, but sales fell by 21.3% year on year to $166.9 million. Its non-GAAP profit of $0.17 per share was 33.9% above analysts’ consensus estimates.

Is now the time to buy Prospect Capital? Find out by accessing our full research report, it’s free.

Prospect Capital (PSEC) Q2 CY2025 Highlights:

- Revenue: $166.9 million vs analyst estimates of $167.1 million (21.3% year-on-year decline, in line)

- Adjusted EPS: $0.17 vs analyst estimates of $0.13 (33.9% beat)

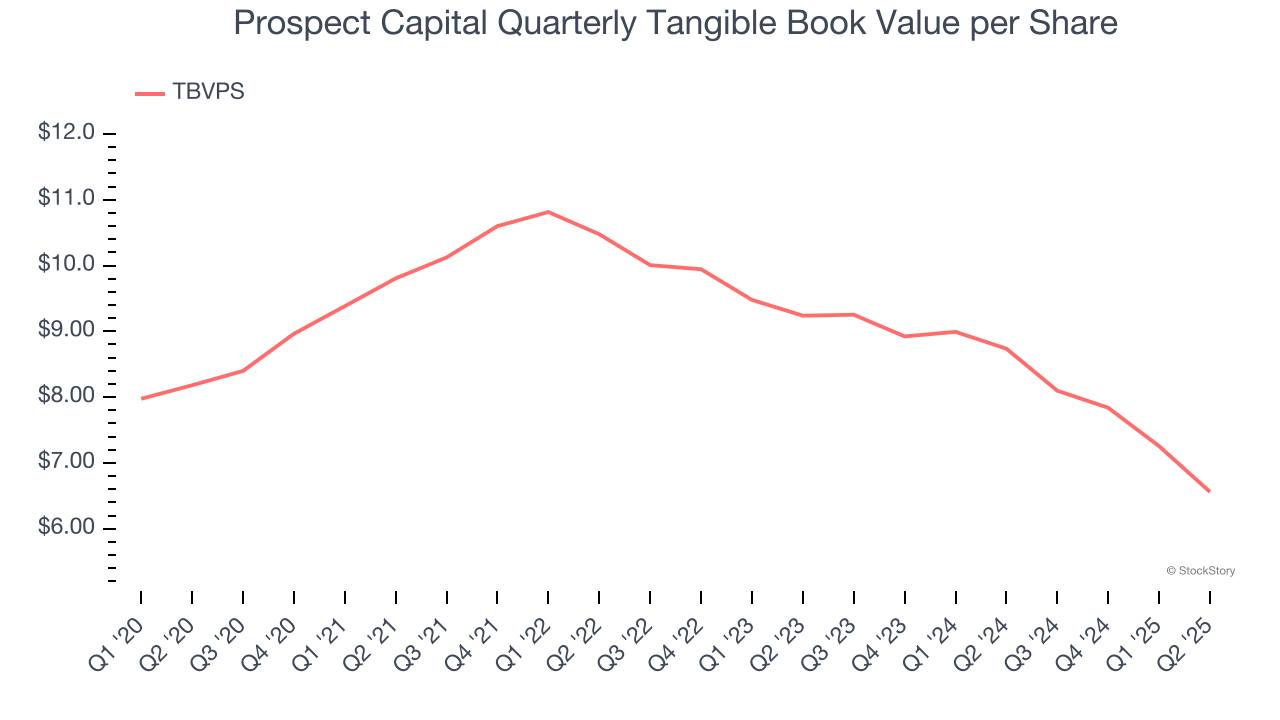

- Tangible Book Value per Share: $6.56 (24.9% year-on-year decline)

- Market Capitalization: $1.29 billion

Company Overview

Operating as one of the largest publicly traded business development companies in the United States, Prospect Capital (NASDAQ: PSEC) provides debt and equity financing to middle-market companies across various industries.

Revenue Growth

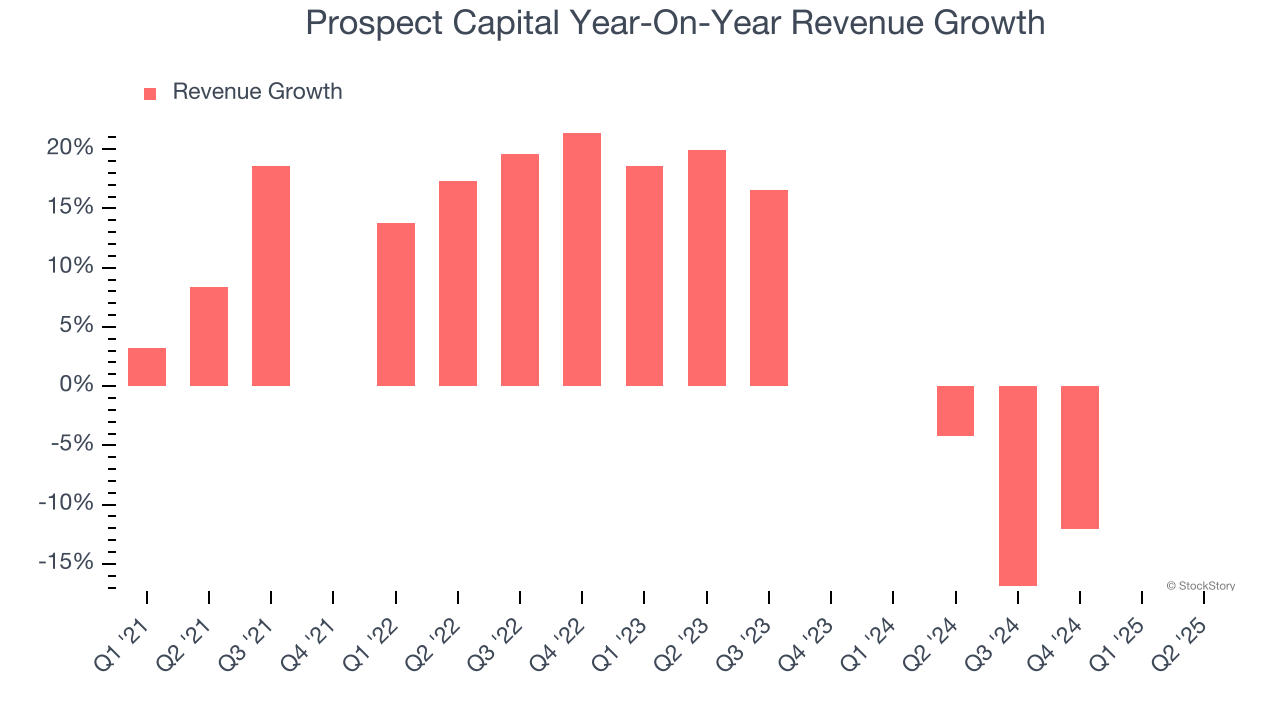

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions. Regrettably, Prospect Capital’s revenue grew at a sluggish 2.4% compounded annual growth rate over the last five years. This fell short of our benchmarks and is a poor baseline for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Prospect Capital’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 8.1% annually.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Prospect Capital reported a rather uninspiring 21.3% year-on-year revenue decline to $166.9 million of revenue, in line with Wall Street’s estimates.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Tangible Book Value Per Share (TBVPS)

Financial institutions manage complex balance sheets spanning various financial activities. Valuations reflect this complexity, emphasizing balance sheet quality and long-term book value compounding across multiple revenue streams.

When analyzing this sector, tangible book value per share (TBVPS) takes precedence over many other metrics. This measure isolates genuine per-share value and provides insight into the institution’s capital position across diverse operations. On the other hand, EPS is often distorted by the diverse nature of operations, mergers, and various accounting treatments across different business units. Book value provides clearer performance insights.

Prospect Capital’s TBVPS declined at a 4.3% annual clip over the last five years. A turnaround doesn’t seem to be in sight as its TBVPS also dropped by 15.7% annually over the last two years ($9.24 to $6.56 per share).

Key Takeaways from Prospect Capital’s Q2 Results

It was good to see Prospect Capital beat analysts’ EPS expectations this quarter. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 1.4% to $2.89 immediately after reporting.

Prospect Capital put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.

More News

View More

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the following

Privacy Policy and Terms Of Service.