Financial News

3 Reasons TFC is Risky and 1 Stock to Buy Instead

Truist Financial has been treading water for the past six months, recording a small return of 1.1% while holding steady at $45.84. The stock also fell short of the S&P 500’s 8.1% gain during that period.

Is there a buying opportunity in Truist Financial, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Truist Financial Not Exciting?

We're swiping left on Truist Financial for now. Here are three reasons there are better opportunities than TFC and a stock we'd rather own.

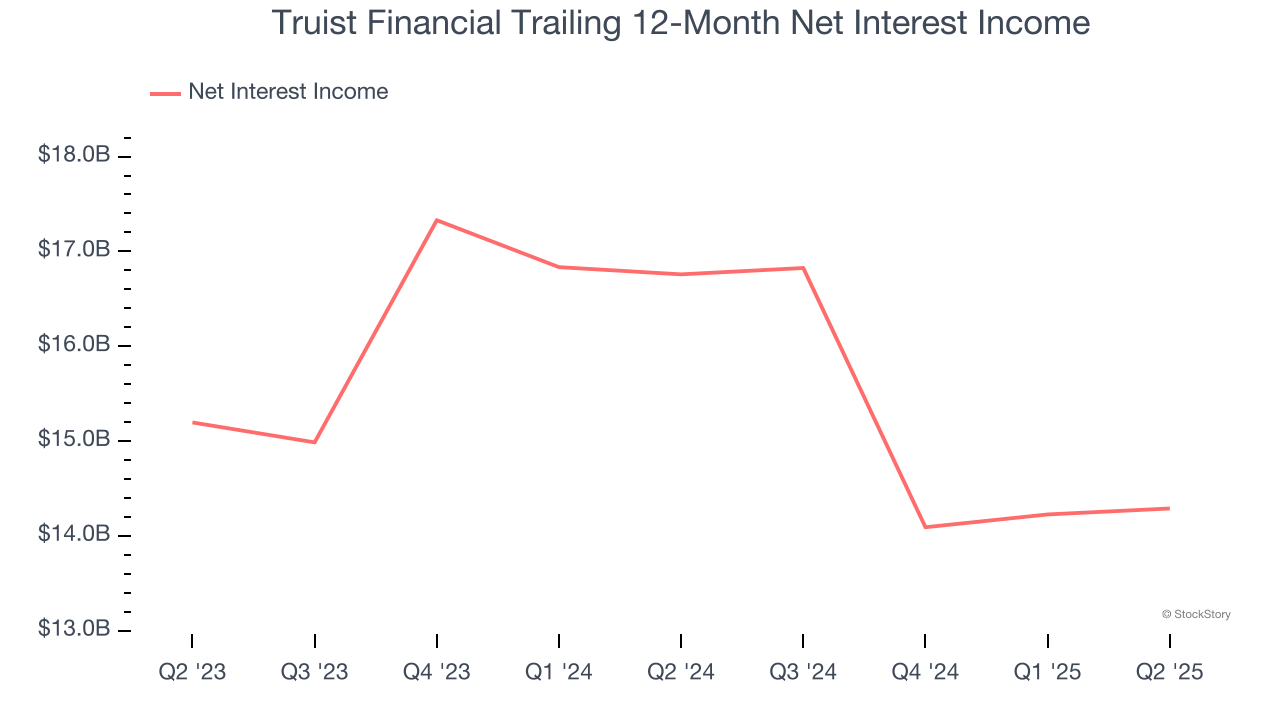

1. Net Interest Income Hits a Plateau

While bank generate revenue from multiple sources, investors view net interest income as a cornerstone - its predictable, recurring characteristics stand in sharp contrast to the volatility of one-time fees.

Truist Financial’s net interest income was flat over the last five years, much worse than the broader banking industry. This shows that lending underperformed its other business lines.

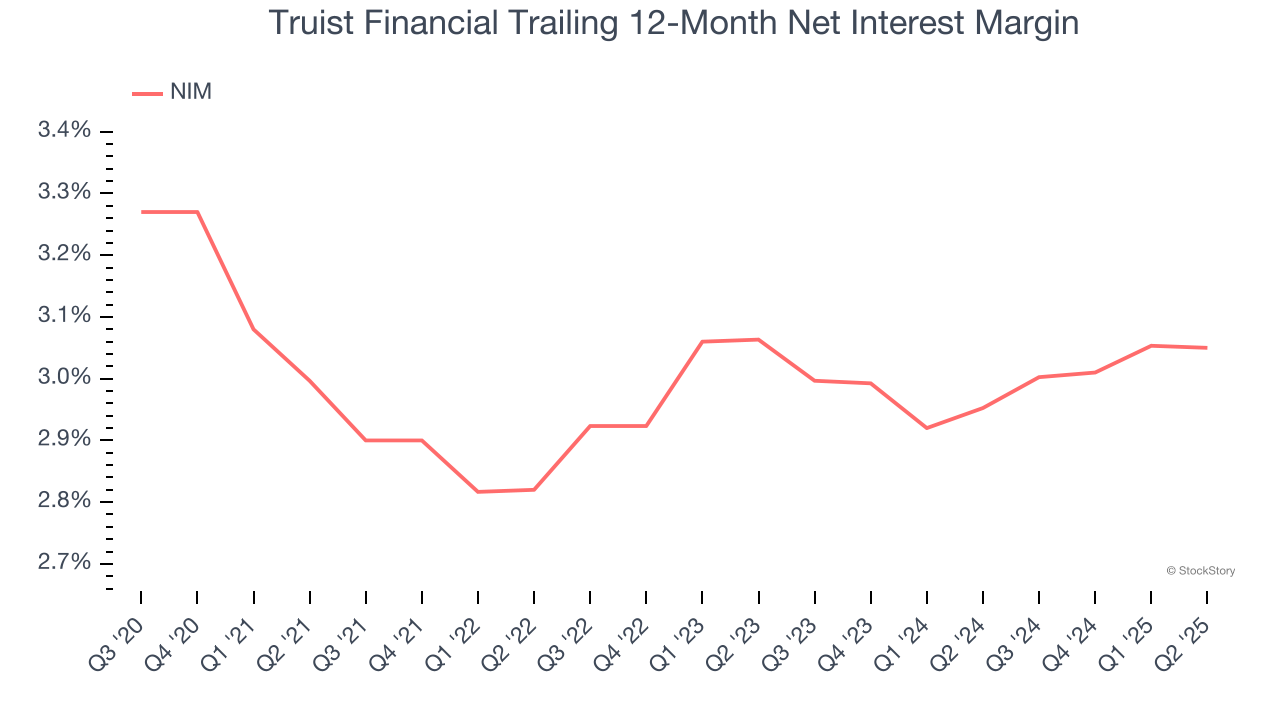

2. Low Net Interest Margin Reveals Weak Loan Book Profitability

Net interest margin (NIM) represents the unit economics of a bank by measuring the profitability of its interest-bearing assets relative to its interest-bearing liabilities. It's a fundamental metric that investors use to assess lending premiums and returns.

Over the past two years, we can see that Truist Financial’s net interest margin averaged a weak 3%, meaning it must compensate for lower profitability through increased loan originations.

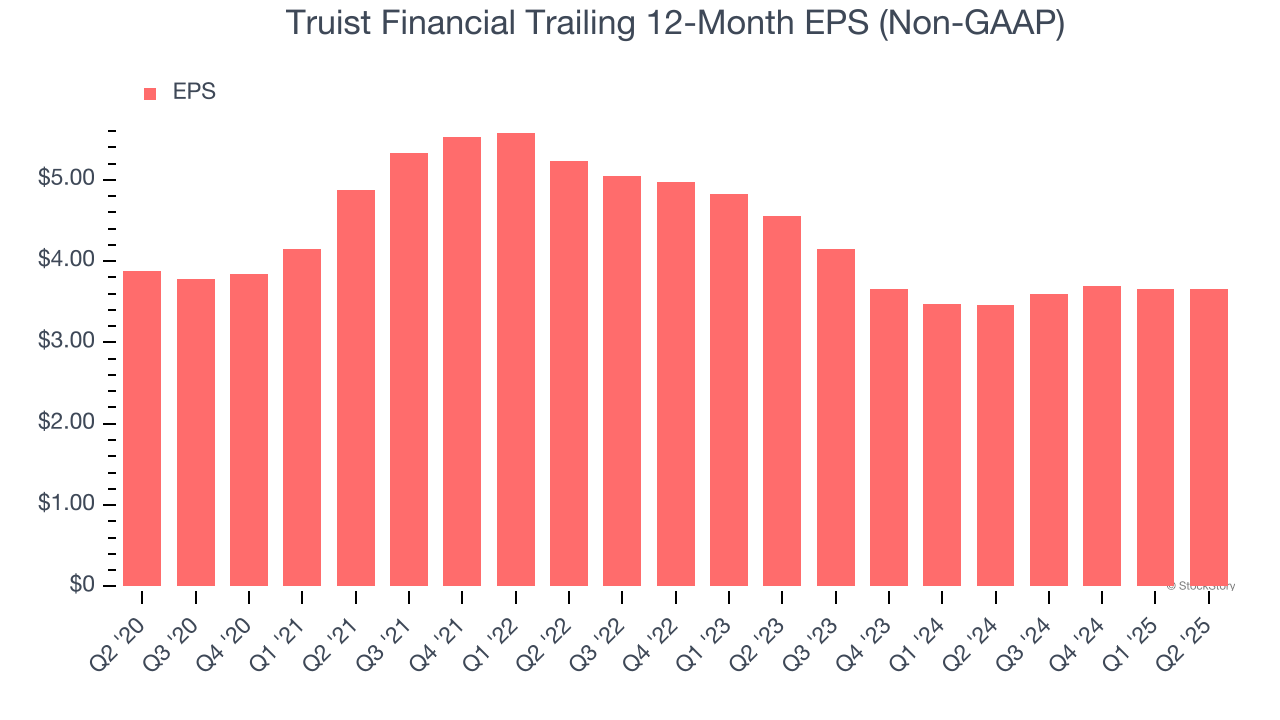

3. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Truist Financial, its EPS declined by 1.2% annually over the last five years while its revenue grew by 2.3%. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Truist Financial’s business quality ultimately falls short of our standards. With its shares lagging the market recently, the stock trades at 1× forward P/B (or $45.84 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're pretty confident there are superior stocks to buy right now. We’d suggest looking at a top digital advertising platform riding the creator economy.

High-Quality Stocks for All Market Conditions

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

More News

View More

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the following

Privacy Policy and Terms Of Service.