Financial News

Lyft (NASDAQ:LYFT) Misses Q1 Sales Targets, But Stock Soars 7.6%

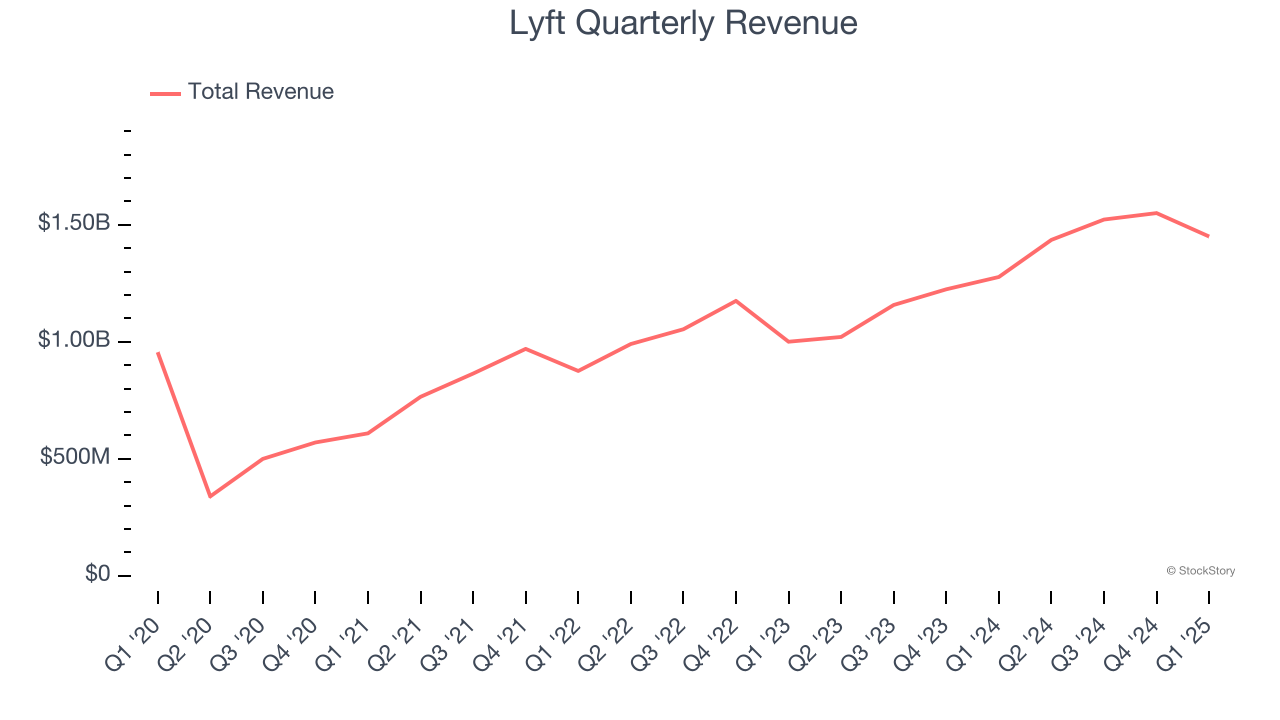

Ride sharing service Lyft (NASDAQ: LYFT) missed Wall Street’s revenue expectations in Q1 CY2025, but sales rose 13.5% year on year to $1.45 billion. Its GAAP profit of $0.01 per share was $0.03 above analysts’ consensus estimates.

Is now the time to buy Lyft? Find out by accessing our full research report, it’s free.

Lyft (LYFT) Q1 CY2025 Highlights:

- Revenue: $1.45 billion vs analyst estimates of $1.47 billion (13.5% year-on-year growth, 1.3% miss)

- EPS (GAAP): $0.01 vs analyst estimates of -$0.02 ($0.03 beat)

- Adjusted EBITDA: $106.5 million vs analyst estimates of $92.39 million (7.3% margin, 15.3% beat)

- EBITDA guidance for Q2 CY2025 is $122.5 million at the midpoint, in line with analyst expectations

- Operating Margin: -2%, up from -4.9% in the same quarter last year

- Free Cash Flow Margin: 19.4%, up from 9% in the previous quarter

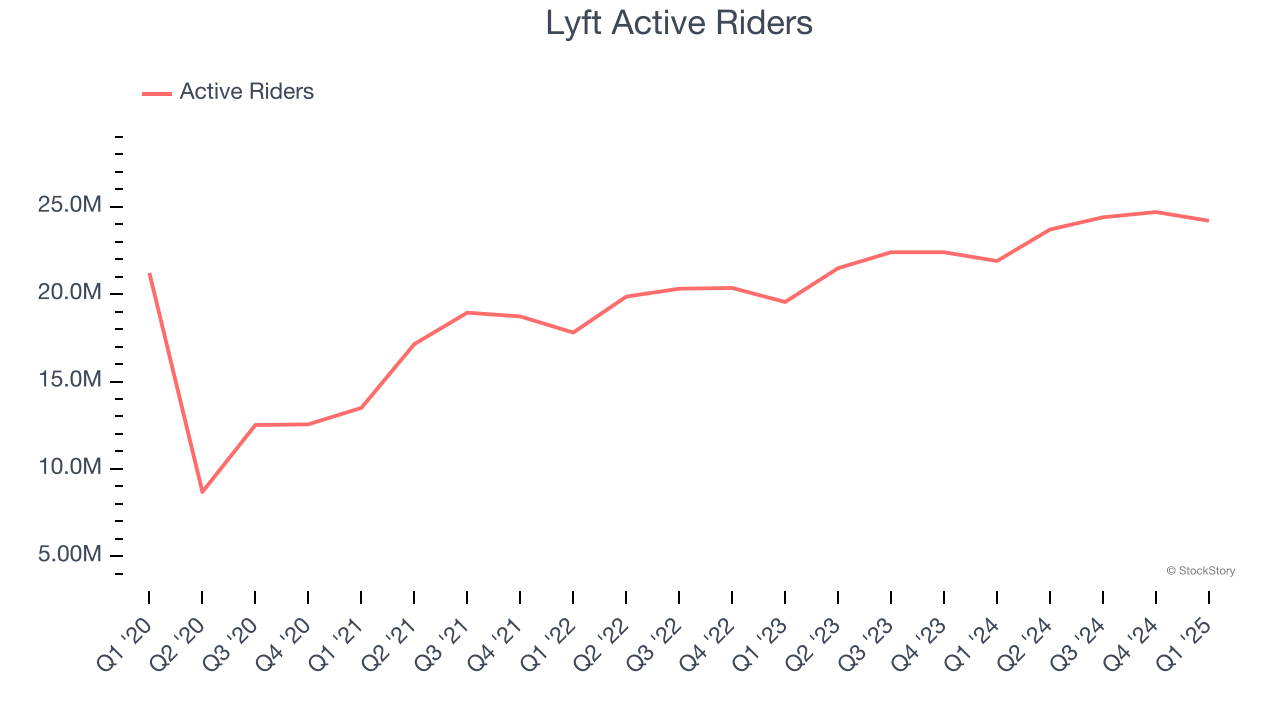

- Active Riders: 24.2 million, up 2.3 million year on year

- Market Capitalization: $5.30 billion

Company Overview

Founded by Logan Green and John Zimmer as a long-distance intercity carpooling company Zimride, Lyft (NASDAQ: LYFT) operates a ridesharing network in the US and Canada.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last three years, Lyft grew its sales at an impressive 19.7% compounded annual growth rate. Its growth beat the average consumer internet company and shows its offerings resonate with customers, a helpful starting point for our analysis.

This quarter, Lyft’s revenue grew by 13.5% year on year to $1.45 billion but fell short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 12.5% over the next 12 months, a deceleration versus the last three years. Despite the slowdown, this projection is above average for the sector and indicates the market is baking in some success for its newer products and services.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Active Riders

User Growth

As a gig economy marketplace, Lyft generates revenue growth by expanding the number of services on its platform (e.g. rides, deliveries, freelance jobs) and raising the commission fee from each service provided.

Over the last two years, Lyft’s active riders, a key performance metric for the company, increased by 10.1% annually to 24.2 million in the latest quarter. This growth rate is solid for a consumer internet business and indicates people are excited about its offerings.

In Q1, Lyft added 2.3 million active riders, leading to 10.5% year-on-year growth. The quarterly print isn’t too different from its two-year result, suggesting its new initiatives aren’t accelerating user growth just yet.

Revenue Per User

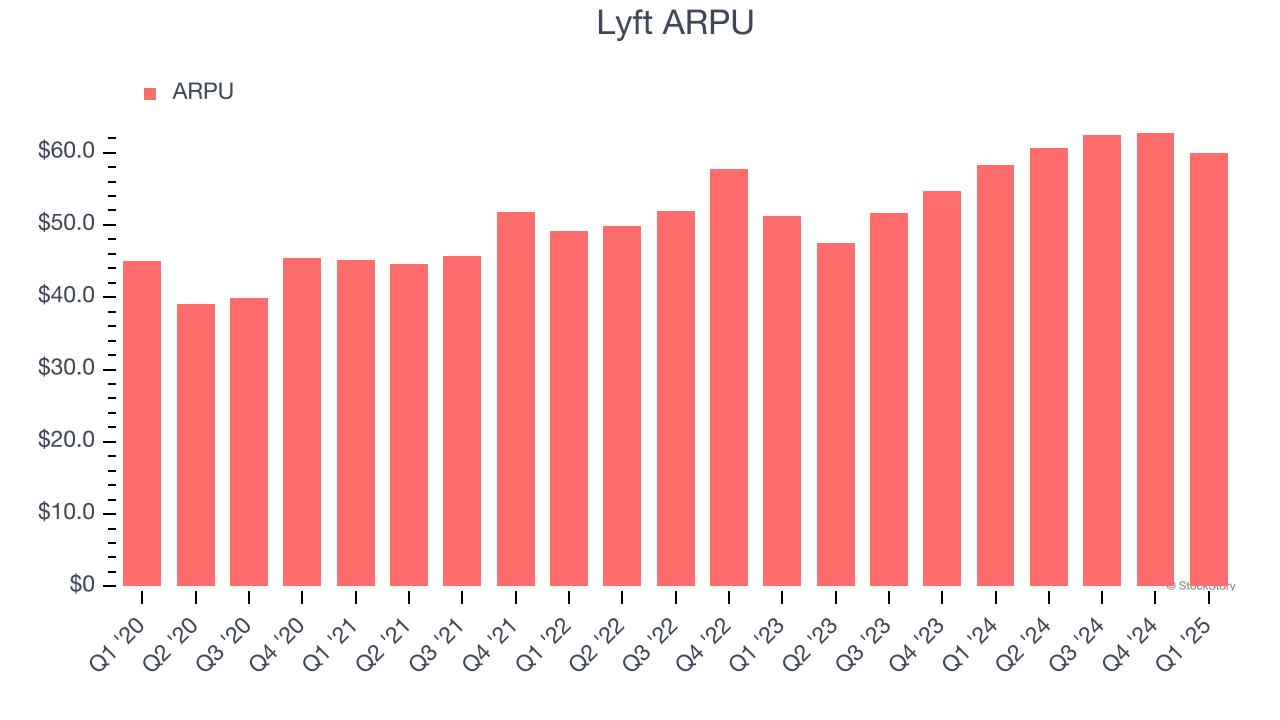

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns in transaction fees from each user. This number also informs us about Lyft’s take rate, which represents its pricing leverage over the ecosystem, or "cut" from each transaction.

Lyft’s ARPU growth has been impressive over the last two years, averaging 8.7%. Its ability to increase monetization while quickly growing its active riders reflects the strength of its platform, as its users continue to spend more each year.

This quarter, Lyft’s ARPU clocked in at $59.92. It grew by 2.8% year on year, slower than its user growth.

Key Takeaways from Lyft’s Q1 Results

We were impressed by how significantly Lyft blew past analysts’ EPS and EBITDA expectations this quarter. We were also glad it expanded its number of users. On the other hand, its revenue slightly missed. Still, we think this was a solid quarter due to the better-than-anticipated profitability. The stock traded up 7.6% to $14 immediately after reporting.

Is Lyft an attractive investment opportunity at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

More News

View More

Recent Quotes

View MoreQuotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.