Financial News

2 Reasons to Watch ITT and 1 to Stay Cautious

ITT has followed the market’s trajectory closely. The stock is down 13.8% to $127.22 per share over the past six months while the S&P 500 has lost 10.7%. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Following the drawdown, is now a good time to buy ITT? Find out in our full research report, it’s free.

Why Does ITT Spark Debate?

Playing a crucial role in the development of the first transatlantic television transmission in 1956, ITT (NYSE: ITT) provides motion and fluid handling equipment for various industries

Two Positive Attributes:

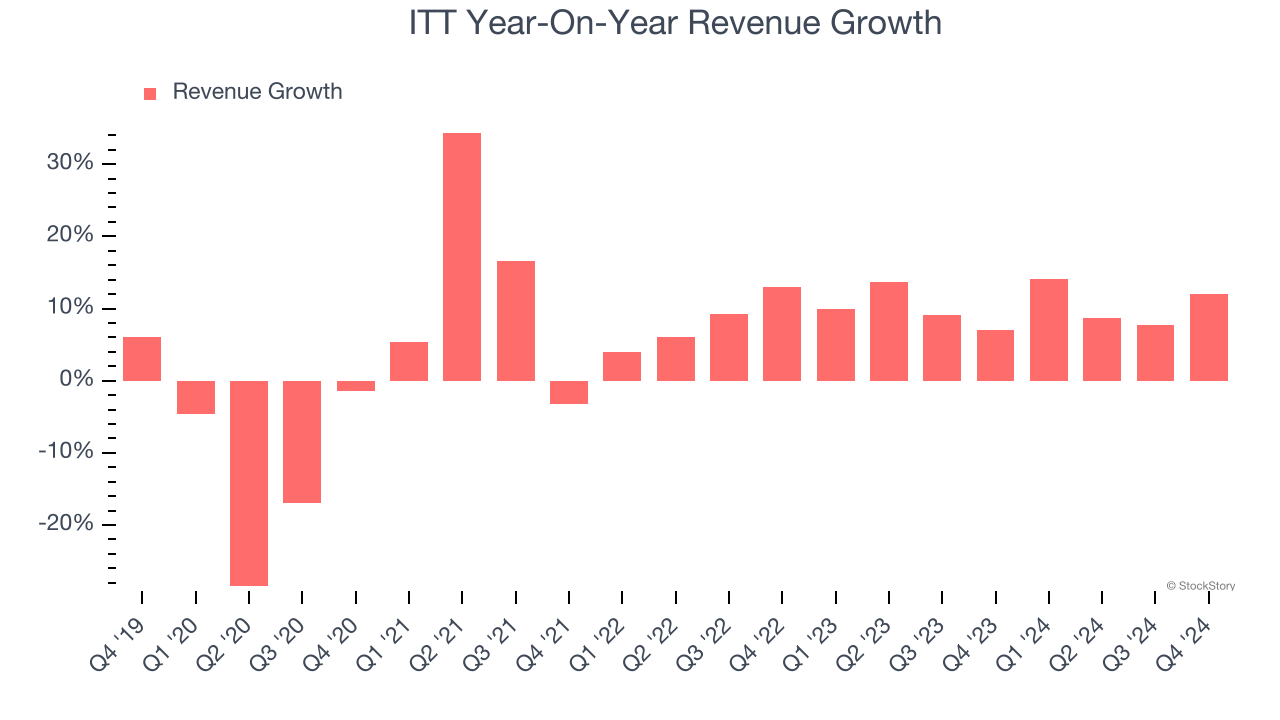

1. Encouraging Short-Term Revenue Growth

We at StockStory place the most emphasis on long-term growth, but within industrials, a stretched historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. ITT’s annualized revenue growth of 10.2% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

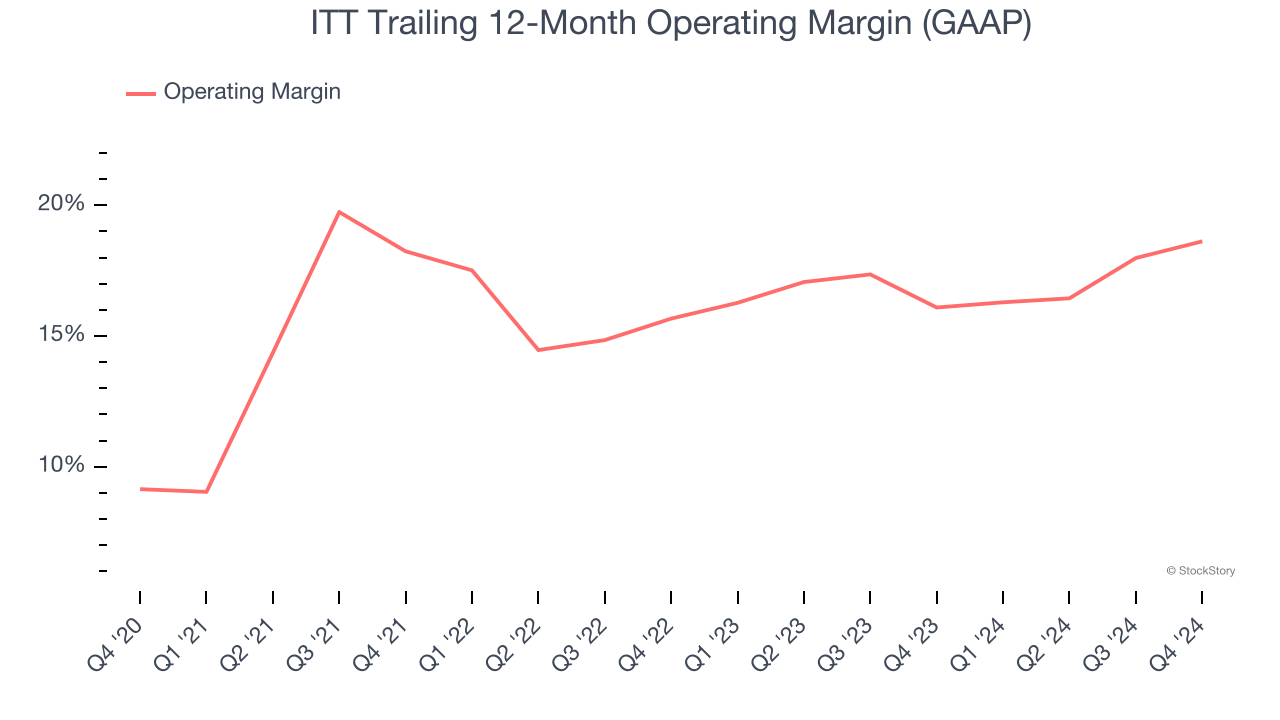

2. Operating Margin Rising, Profits Up

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Analyzing the trend in its profitability, ITT’s operating margin rose by 9.5 percentage points over the last five years, as its sales growth gave it operating leverage. Its operating margin for the trailing 12 months was 18.6%.

One Reason to be Careful:

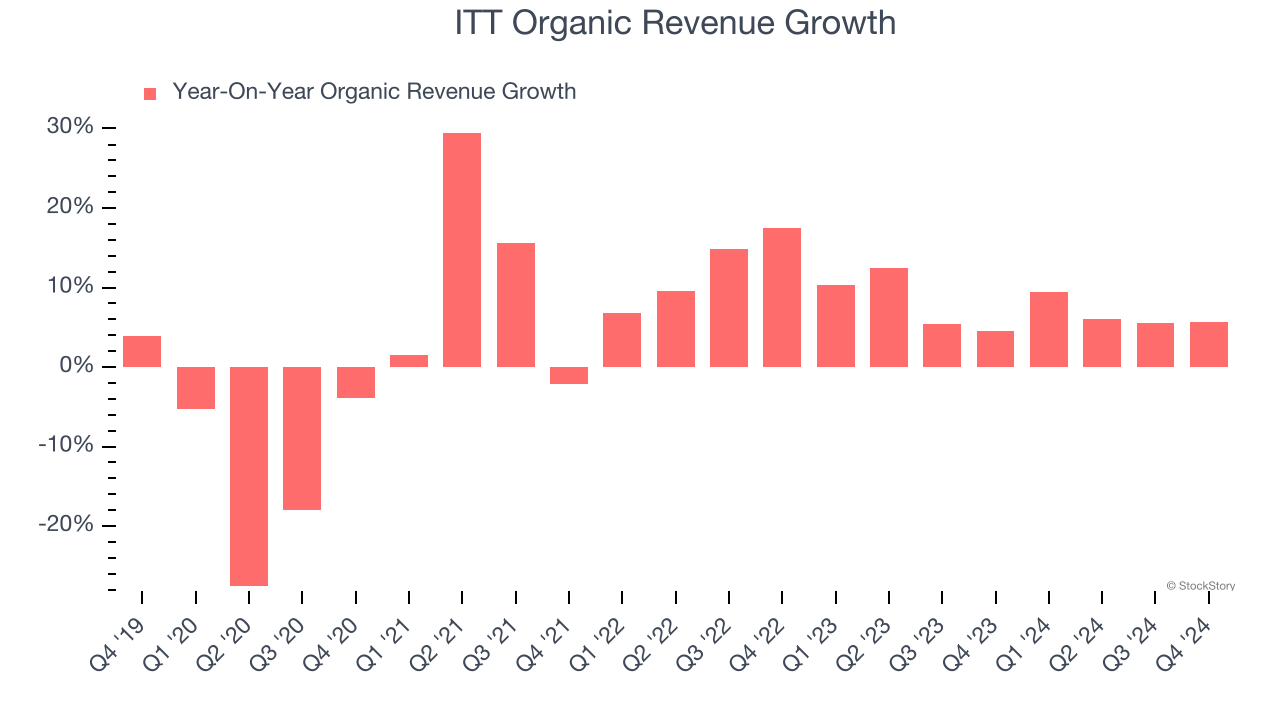

Slow Organic Growth Suggests Waning Demand In Core Business

Investors interested in Gas and Liquid Handling companies should track organic revenue in addition to reported revenue. This metric gives visibility into ITT’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, ITT’s organic revenue averaged 7.4% year-on-year growth. This performance slightly lagged the sector and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

Final Judgment

ITT’s positive characteristics outweigh the negatives. With the recent decline, the stock trades at 19.7× forward price-to-earnings (or $127.22 per share). Is now a good time to buy? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than ITT

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.

More News

View More

Recent Quotes

View More

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.