Financial News

MACOM (MTSI): Buy, Sell, or Hold Post Q4 Earnings?

Over the past six months, MACOM’s shares (currently trading at $100.51) have posted a disappointing 7.4% loss while the S&P 500 was down 1.6%. This might have investors contemplating their next move.

Following the drawdown, is now the time to buy MTSI? Find out in our full research report, it’s free.

Why Does MACOM Spark Debate?

Founded in the 1950s as Microwave Associates, a communications supplier to the US Army Signal Corp, today MACOM Technology Solutions (NASDAQ: MTSI) is a provider of analog chips used in optical, wireless, and satellite networks.

Two Things to Like:

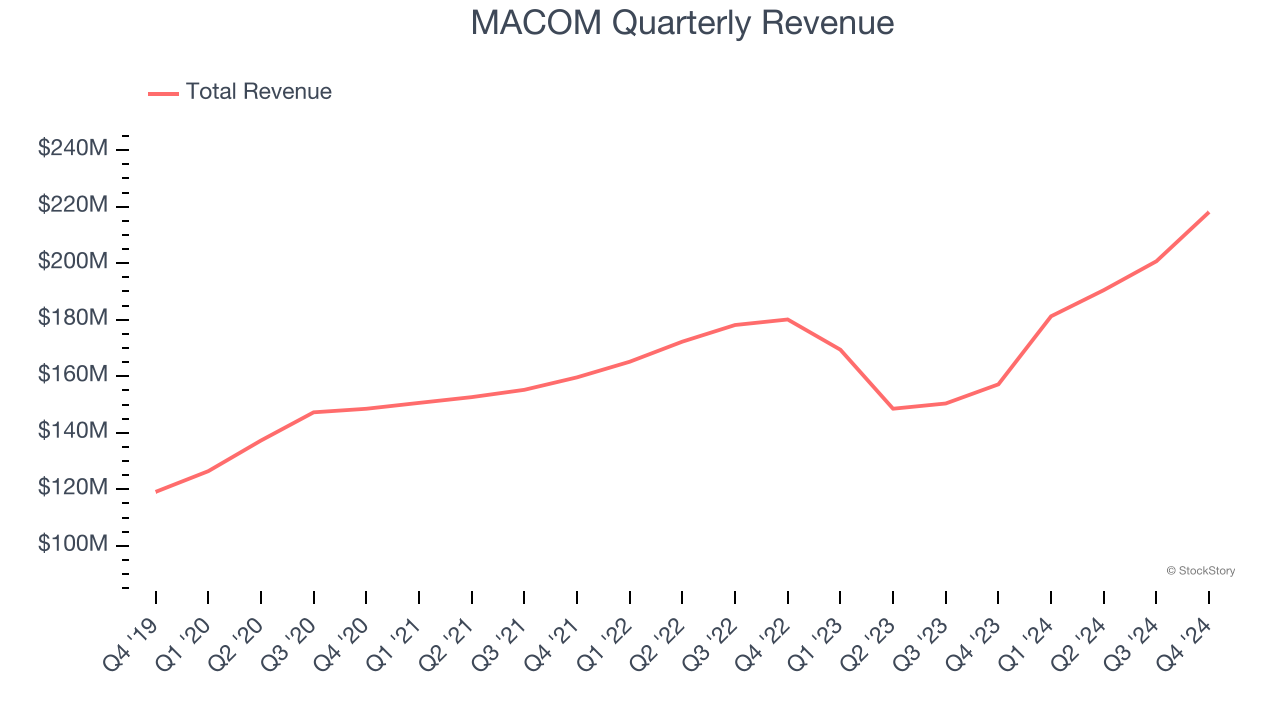

1. Long-Term Revenue Growth Shows Strong Momentum

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, MACOM’s sales grew at a solid 11% compounded annual growth rate over the last five years. Its growth surpassed the average semiconductor company and shows its offerings resonate with customers. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

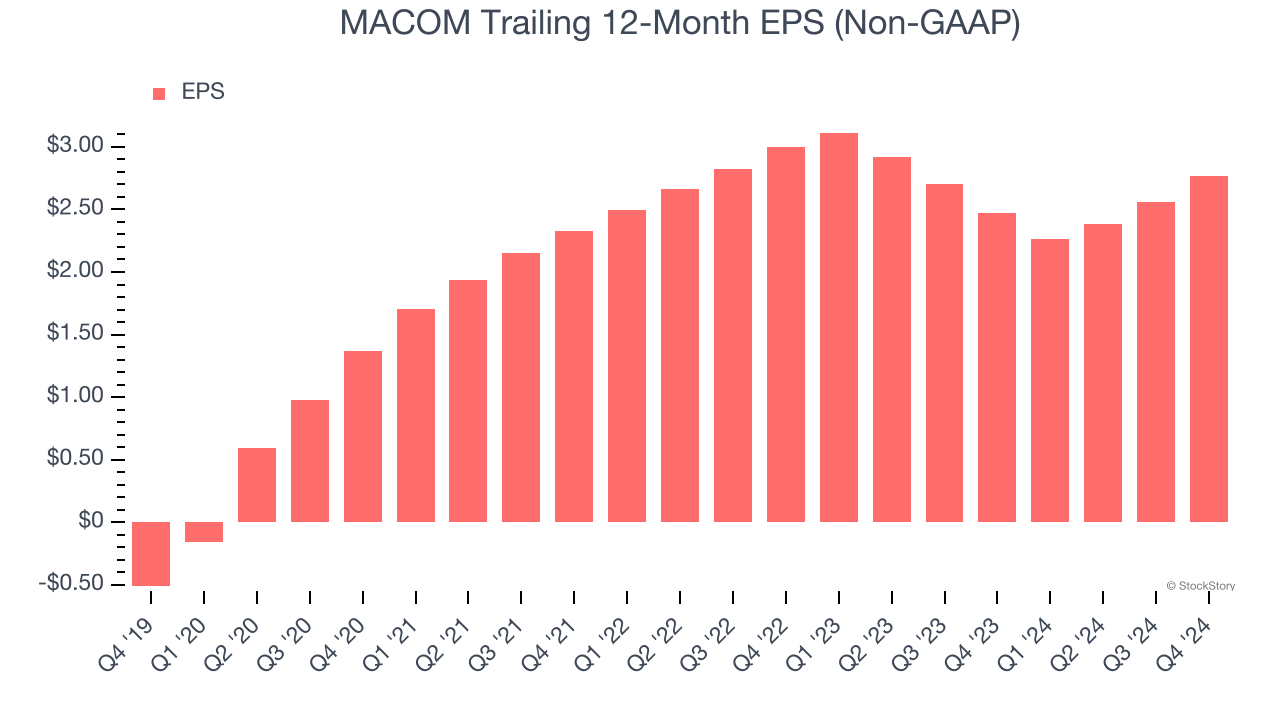

2. Outstanding Long-Term EPS Growth

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

MACOM’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

One Reason to be Careful:

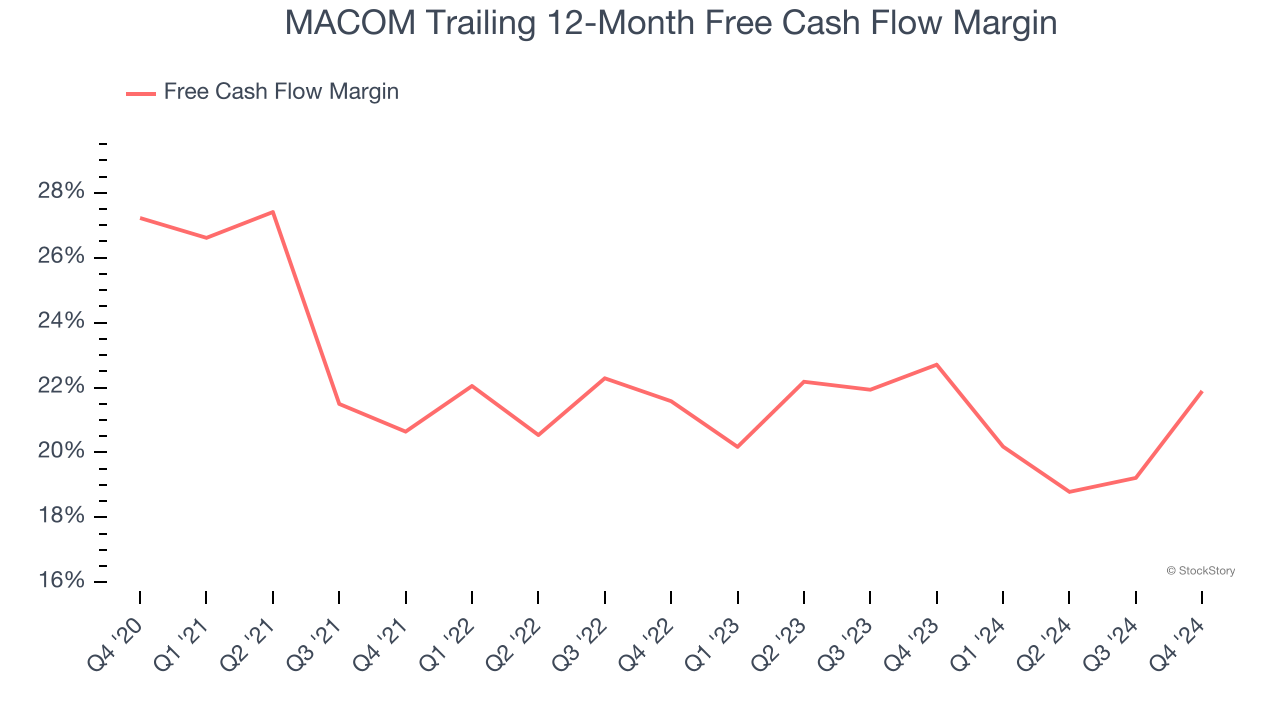

Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, MACOM’s margin dropped by 5.3 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. MACOM’s free cash flow margin for the trailing 12 months was 21.9%.

Final Judgment

MACOM has huge potential even though it has some open questions. After the recent drawdown, the stock trades at 27.8× forward price-to-earnings (or $100.51 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than MACOM

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.

More News

View More

Recent Quotes

View More

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.