Financial News

Environmental and Facilities Services Stocks Q4 Teardown: Rollins (NYSE:ROL) Vs The Rest

As the craze of earnings season draws to a close, here’s a look back at some of the most exciting (and some less so) results from Q4. Today, we are looking at environmental and facilities services stocks, starting with Rollins (NYSE: ROL).

Many environmental and facility services are non-discretionary (sports stadiums need to be cleaned after events), recurring, and performed through longer-term contracts. This makes for more predictable and stickier revenue streams. Additionally, there has been an increasing focus on emissions and water conservation over the last decade, driving innovation in the sector and demand for new services. Despite these tailwinds, environmental and facility services companies are still at the whim of economic cycles. Interest rates, for example, can greatly impact commercial construction projects that drive incremental demand for these services.

The 13 environmental and facilities services stocks we track reported a slower Q4. As a group, revenues were in line with analysts’ consensus estimates.

While some environmental and facilities services stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 1.2% since the latest earnings results.

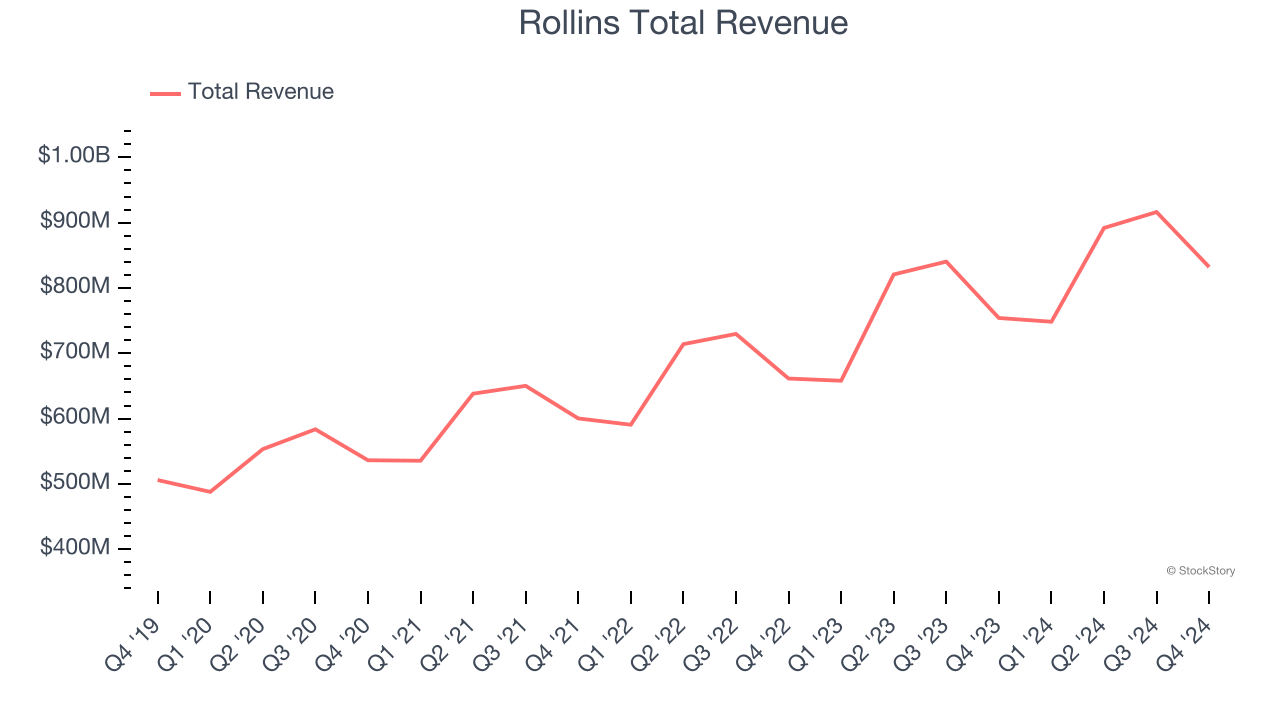

Rollins (NYSE: ROL)

Operating under multiple brands like Orkin and HomeTeam Pest Defense, Rollins (NYSE: ROL) provides pest and wildlife control services to residential and commercial customers.

Rollins reported revenues of $832.2 million, up 10.4% year on year. This print exceeded analysts’ expectations by 1.5%. Despite the top-line beat, it was still a slower quarter for the company with a miss of analysts’ adjusted operating income and EPS estimates.

The stock is up 8% since reporting and currently trades at $53.99.

Is now the time to buy Rollins? Access our full analysis of the earnings results here, it’s free.

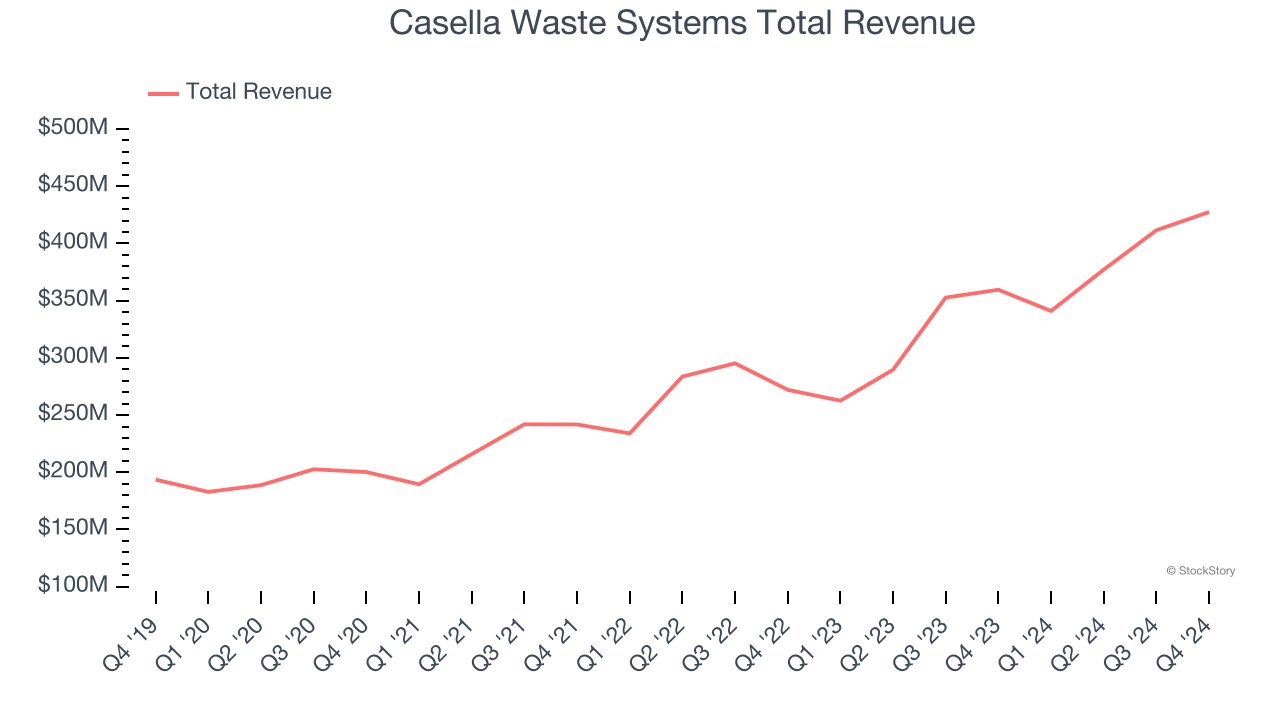

Best Q4: Casella Waste Systems (NASDAQ: CWST)

Starting with the founder picking up garbage with a pickup truck he purchased using savings from high school, Casella (NASDAQ: CWST) offers waste management services for businesses, residents, and the government.

Casella Waste Systems reported revenues of $427.5 million, up 18.9% year on year, outperforming analysts’ expectations by 2.3%. The business had an exceptional quarter with an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

Casella Waste Systems scored the fastest revenue growth and highest full-year guidance raise among its peers. The market seems content with the results as the stock is up 4.7% since reporting. It currently trades at $111.79.

Is now the time to buy Casella Waste Systems? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Perma-Fix (NASDAQ: PESI)

Tackling hazardous waste challenges since 1990, Perma-Fix (NASDAQ: PESI) provides environmental waste treatment services.

Perma-Fix reported revenues of $14.7 million, down 35.3% year on year, falling short of analysts’ expectations by 6.9%. It was a disappointing quarter as it posted a significant miss of analysts’ EBITDA and EPS estimates.

Perma-Fix delivered the weakest performance against analyst estimates and slowest revenue growth in the group. Interestingly, the stock is up 37.9% since the results and currently trades at $9.99.

Read our full analysis of Perma-Fix’s results here.

Waste Management (NYSE: WM)

Headquartered in Houston, Waste Management (NYSE: WM) is a provider of comprehensive waste management services in North America.

Waste Management reported revenues of $5.89 billion, up 13% year on year. This number surpassed analysts’ expectations by 0.9%. More broadly, it was a slower quarter as it logged a significant miss of analysts’ adjusted operating income and EPS estimates.

The stock is up 10.8% since reporting and currently trades at $232.43.

Read our full, actionable report on Waste Management here, it’s free.

Clean Harbors (NYSE: CLH)

Established in 1980, Clean Harbors (NYSE: CLH) provides environmental and industrial services like hazardous and non-hazardous waste disposal and emergency spill cleanups.

Clean Harbors reported revenues of $1.43 billion, up 6.9% year on year. This result met analysts’ expectations. Zooming out, it was a mixed quarter as it also produced an impressive beat of analysts’ EPS estimates but full-year EBITDA guidance missing analysts’ expectations.

The stock is down 13.7% since reporting and currently trades at $195.21.

Read our full, actionable report on Clean Harbors here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.

More News

View More

Recent Quotes

View MoreQuotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.