Financial News

Modern Fast Food Stocks Q4 In Review: Chipotle (NYSE:CMG) Vs Peers

Let’s dig into the relative performance of Chipotle (NYSE: CMG) and its peers as we unravel the now-completed Q4 modern fast food earnings season.

Modern fast food is a relatively newer category representing a middle ground between traditional fast food and sit-down restaurants. These establishments feature an expanded menu selection priced above traditional fast food options, often incorporating fresher and cleaner ingredients to serve customers prioritizing quality. These eateries are capitalizing on the perception that your drive-through burger and fries joint is detrimental to your health because of inferior ingredients.

The 7 modern fast food stocks we track reported a mixed Q4. As a group, revenues along with next quarter’s revenue guidance were in line with analysts’ consensus estimates.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 14.9% since the latest earnings results.

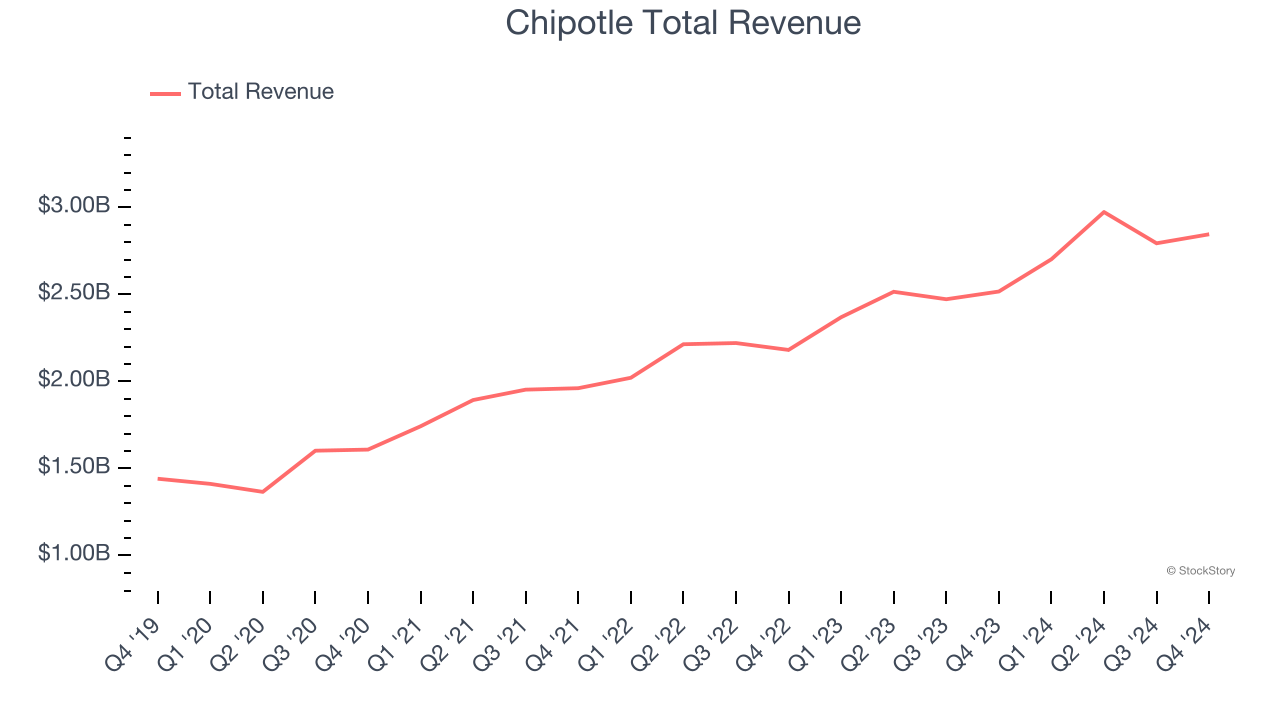

Chipotle (NYSE: CMG)

Born from a desire to offer quick meals with fresh, flavorful ingredients, Chipotle (NYSE: CMG) is a fast-food chain known for its healthy, Mexican-inspired cuisine and customizable dishes.

Chipotle reported revenues of $2.85 billion, up 13.1% year on year. This print was in line with analysts’ expectations, but overall, it was a slower quarter for the company with a slight miss of analysts’ EBITDA estimates and same-store sales in line with analysts’ estimates.

"Chipotle had another outstanding year, delivering strong transaction driven comps each quarter, expanding margins, adding over 300 new restaurants, gaining momentum in key industry leading brand metrics, making progress on many restaurant operating initiatives and building our footprint internationally," said Scott Boatwright, CEO, Chipotle.

The stock is down 16.7% since reporting and currently trades at $49.18.

Is now the time to buy Chipotle? Access our full analysis of the earnings results here, it’s free.

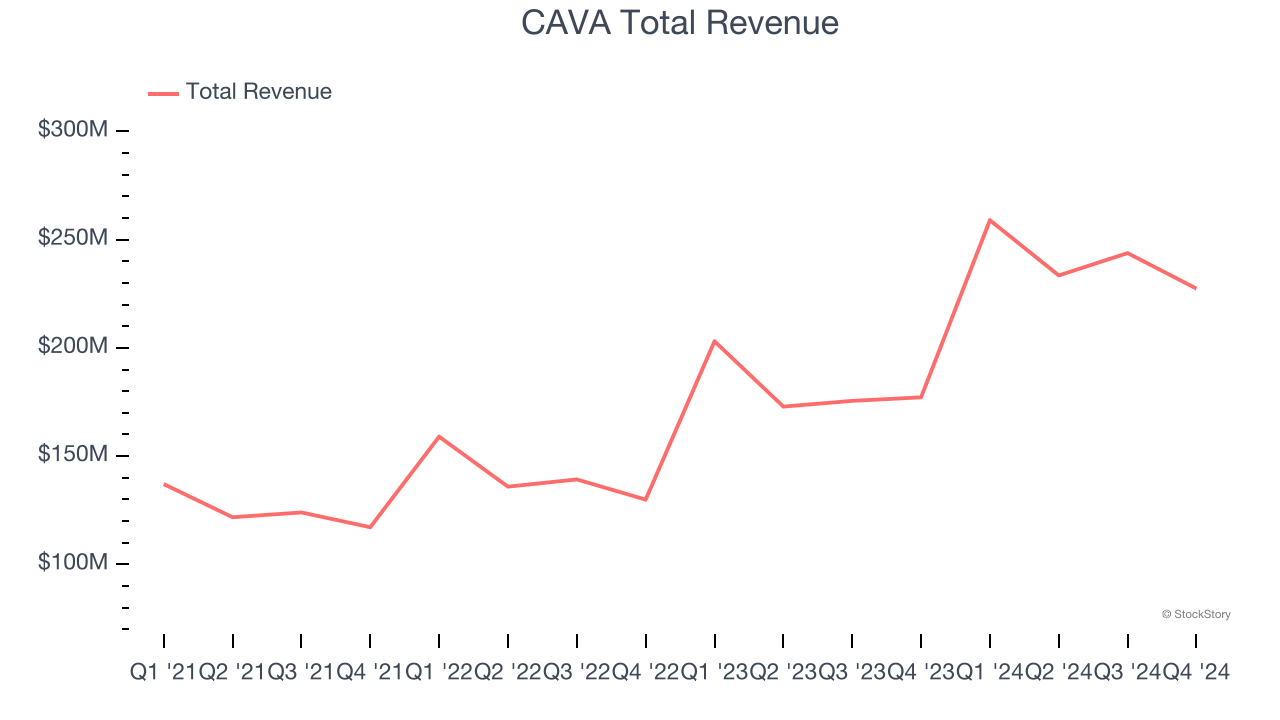

Best Q4: CAVA (NYSE: CAVA)

Starting from a single Washington, D.C. location, CAVA (NYSE: CAVA) operates a fast-casual restaurant chain offering customizable Mediterranean-inspired dishes.

CAVA reported revenues of $227.4 million, up 28.3% year on year, outperforming analysts’ expectations by 2.2%. The business had a very strong quarter with a solid beat of analysts’ EPS and same-store sales estimates.

CAVA achieved the biggest analyst estimates beat and fastest revenue growth among its peers. Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 17.9% since reporting. It currently trades at $81.51.

Is now the time to buy CAVA? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Sweetgreen (NYSE: SG)

Founded in 2007 by three Georgetown University alum, Sweetgreen (NYSE: SG) is a casual quick service chain known for its healthy salads and bowls.

Sweetgreen reported revenues of $160.9 million, up 5.1% year on year, in line with analysts’ expectations. It was a softer quarter as it posted a significant miss of analysts’ EBITDA estimates.

Sweetgreen delivered the weakest full-year guidance update in the group. Interestingly, the stock is up 7.8% since the results and currently trades at $25.

Read our full analysis of Sweetgreen’s results here.

Potbelly (NASDAQ: PBPB)

With a unique origin story where the company actually started as an antique shop, Potbelly (NASDAQ: PBPB) today is a chain known for its toasty sandwiches.

Potbelly reported revenues of $116.6 million, down 7.3% year on year. This result was in line with analysts’ expectations. Overall, it was a very strong quarter as it also produced an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

Potbelly had the slowest revenue growth among its peers. The stock is down 21.4% since reporting and currently trades at $9.29.

Read our full, actionable report on Potbelly here, it’s free.

Shake Shack (NYSE: SHAK)

Started as a hot dog cart in New York City's Madison Square Park, Shake Shack (NYSE: SHAK) is a fast-food restaurant known for its burgers and milkshakes.

Shake Shack reported revenues of $328.7 million, up 14.8% year on year. This number met analysts’ expectations. Taking a step back, it was a mixed quarter as it underperformed in some other aspects of the business.

The stock is down 22.1% since reporting and currently trades at $86.51.

Read our full, actionable report on Shake Shack here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.

More News

View More

Recent Quotes

View MoreQuotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.