Financial News

JLL (NYSE:JLL) Reports Q3 In Line With Expectations

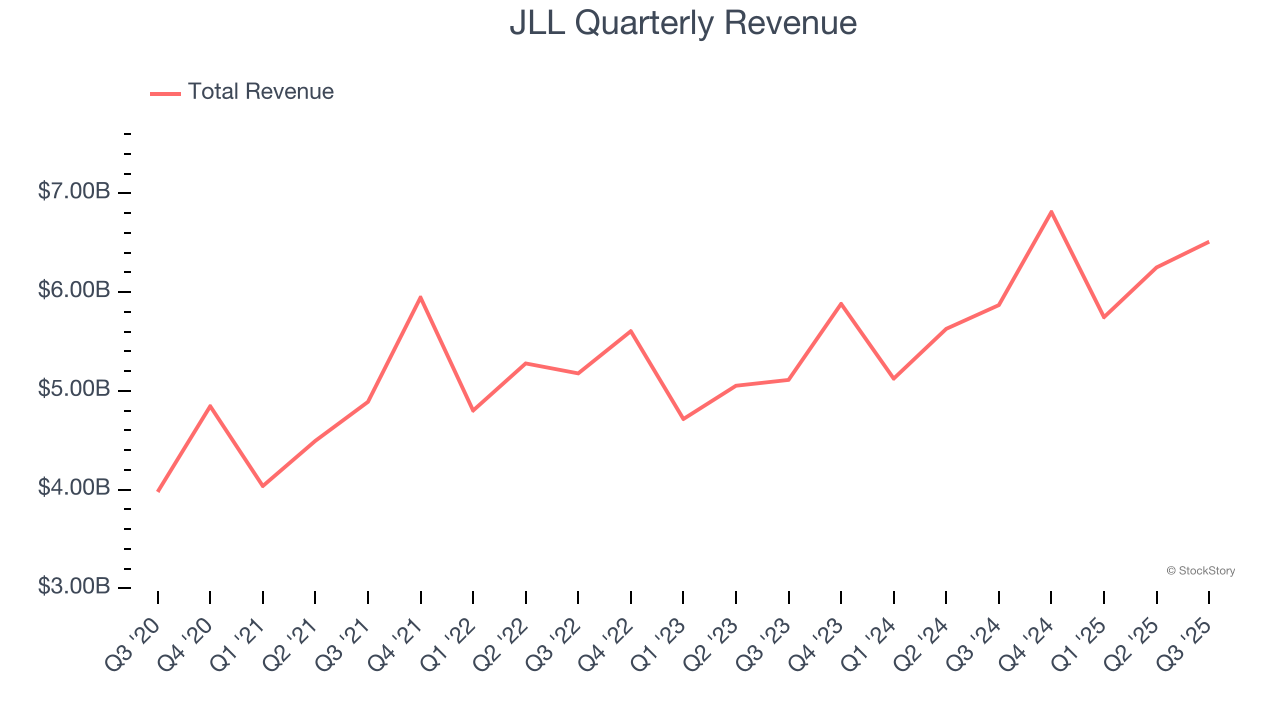

Real estate firm JLL (NYSE: JLL) met Wall Streets revenue expectations in Q3 CY2025, with sales up 10.9% year on year to $6.51 billion. Its non-GAAP profit of $4.50 per share was 5.5% above analysts’ consensus estimates.

Is now the time to buy JLL? Find out by accessing our full research report, it’s free for active Edge members.

JLL (JLL) Q3 CY2025 Highlights:

- Revenue: $6.51 billion vs analyst estimates of $6.54 billion (10.9% year-on-year growth, in line)

- Adjusted EPS: $4.50 vs analyst estimates of $4.27 (5.5% beat)

- Adjusted EBITDA: $347.3 million vs analyst estimates of $346.8 million (5.3% margin, in line)

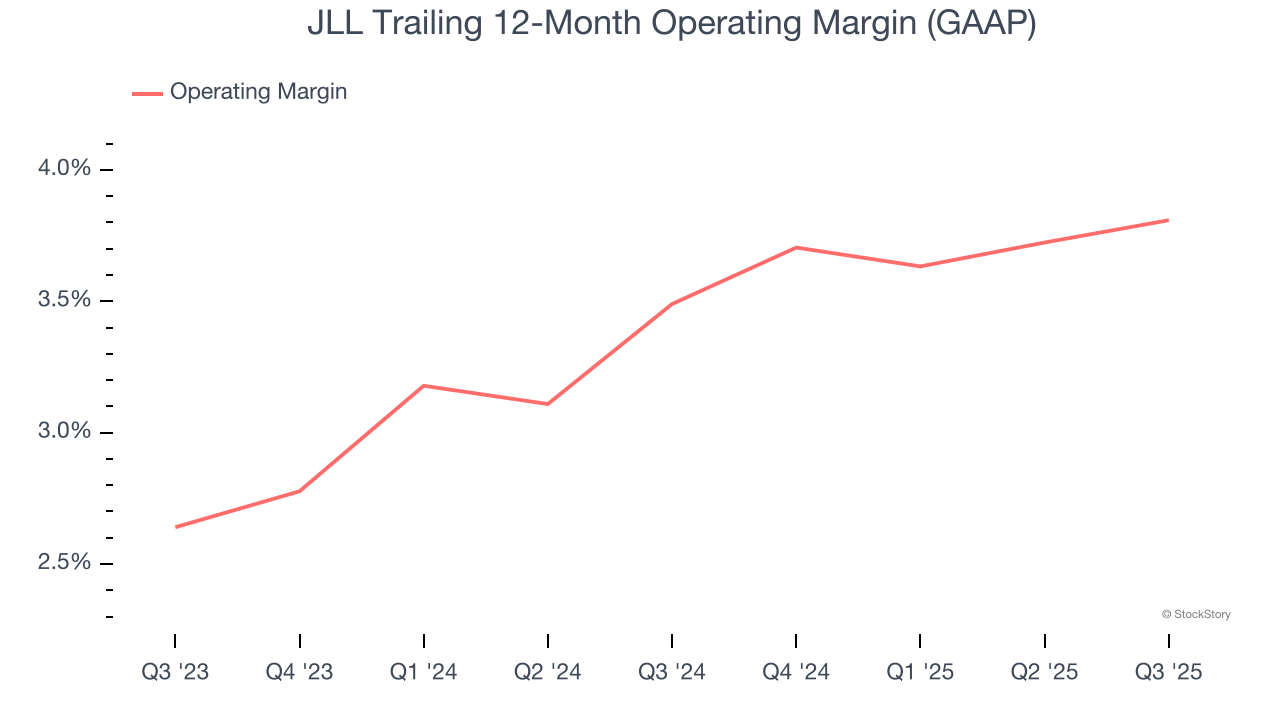

- Operating Margin: 4.2%, in line with the same quarter last year

- Free Cash Flow Margin: 8.7%, up from 3.7% in the same quarter last year

- Market Capitalization: $14.17 billion

"JLL achieved strong top and bottom-line results as well as impressive free cash flow generation in the third quarter, led by an acceleration in transactional revenue and ongoing momentum in our resilient businesses. The strength of JLL's diversified platform is reflected in our eight consecutive quarters of double-digit Adjusted EPS growth," said Christian Ulbrich, JLL CEO.

Company Overview

Founded in 1999 through the merger of Jones Lang Wootton and LaSalle Partners, JLL (NYSE: JLL) is a company specializing in real estate advisory and investment management services.

Revenue Growth

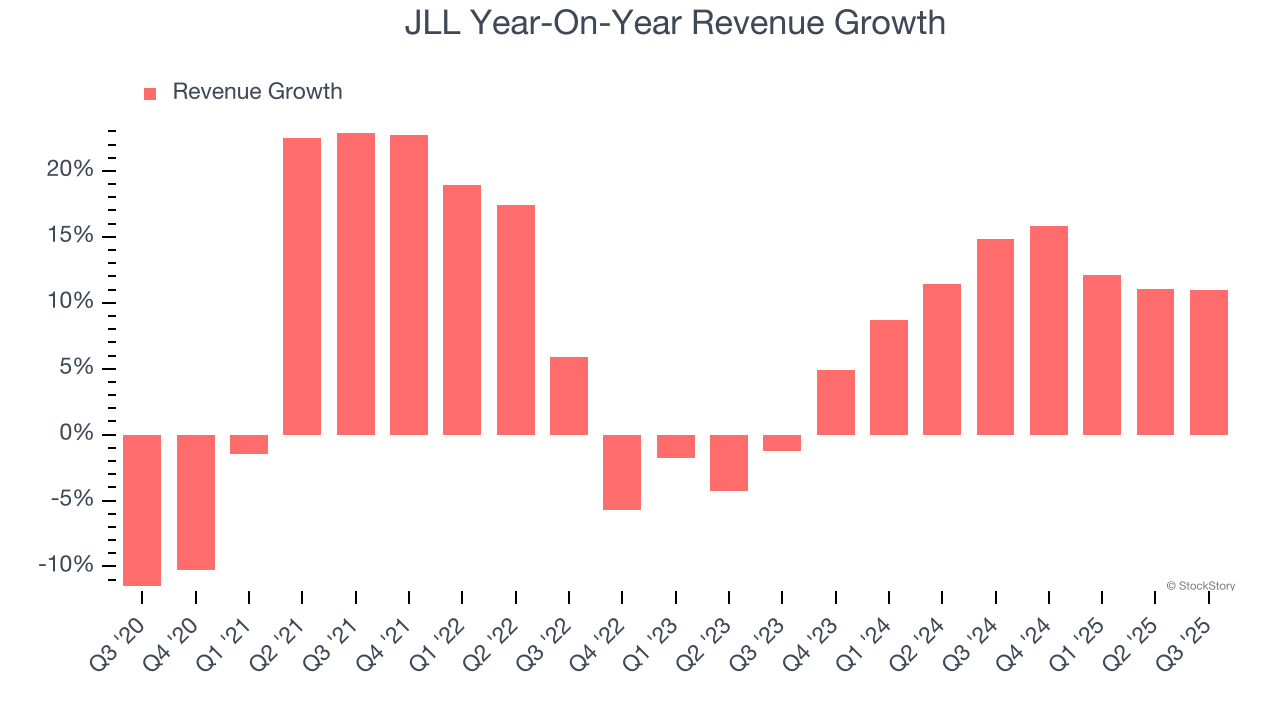

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, JLL grew its sales at a sluggish 8.1% compounded annual growth rate. This fell short of our benchmark for the consumer discretionary sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. JLL’s annualized revenue growth of 11.2% over the last two years is above its five-year trend, but we were still disappointed by the results.

This quarter, JLL’s year-on-year revenue growth was 10.9%, and its $6.51 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 9.5% over the next 12 months, a slight deceleration versus the last two years. This projection is underwhelming and implies its products and services will see some demand headwinds.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Operating Margin

JLL’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 3.7% over the last two years. This profitability was lousy for a consumer discretionary business and caused by its suboptimal cost structure.

This quarter, JLL generated an operating margin profit margin of 4.2%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

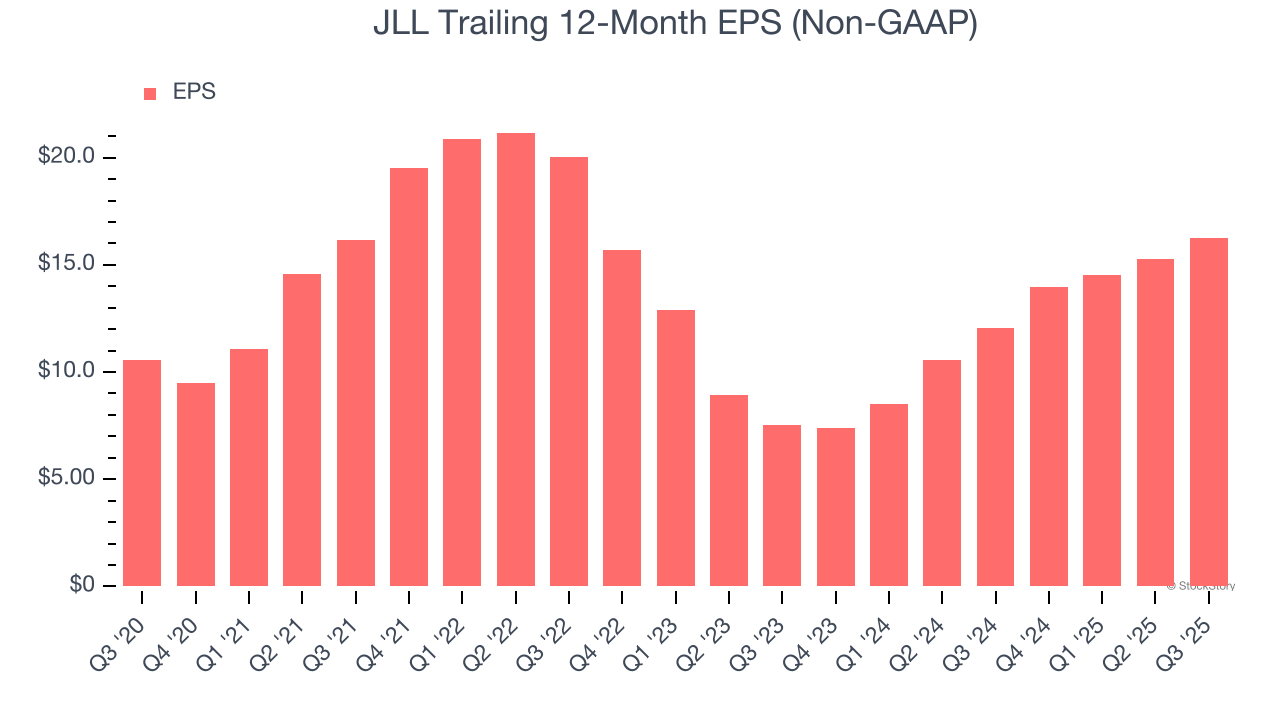

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

JLL’s unimpressive 9.1% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

In Q3, JLL reported adjusted EPS of $4.50, up from $3.50 in the same quarter last year. This print beat analysts’ estimates by 5.5%. Over the next 12 months, Wall Street expects JLL’s full-year EPS of $16.26 to grow 15.7%.

Key Takeaways from JLL’s Q3 Results

It was good to see JLL beat analysts’ EPS expectations this quarter.Zooming out, we think this was a decent quarter. The stock remained flat at $297 immediately after reporting.

So do we think JLL is an attractive buy at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

More News

View More

Recent Quotes

View MoreQuotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.