Financial News

3 Reasons to Sell CHD and 1 Stock to Buy Instead

Church & Dwight currently trades at $105.68 per share and has shown little upside over the past six months, posting a small loss of 3%. The stock also fell short of the S&P 500’s 6.1% gain during that period.

Is now the time to buy Church & Dwight, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.We're cautious about Church & Dwight. Here are three reasons why CHD doesn't excite us and a stock we'd rather own.

Why Is Church & Dwight Not Exciting?

Best known for its Arm & Hammer baking soda, Church & Dwight (NYSE: CHD) is a household and personal care products company with a vast portfolio that spans laundry detergent to toothbrushes to hair removal creams.

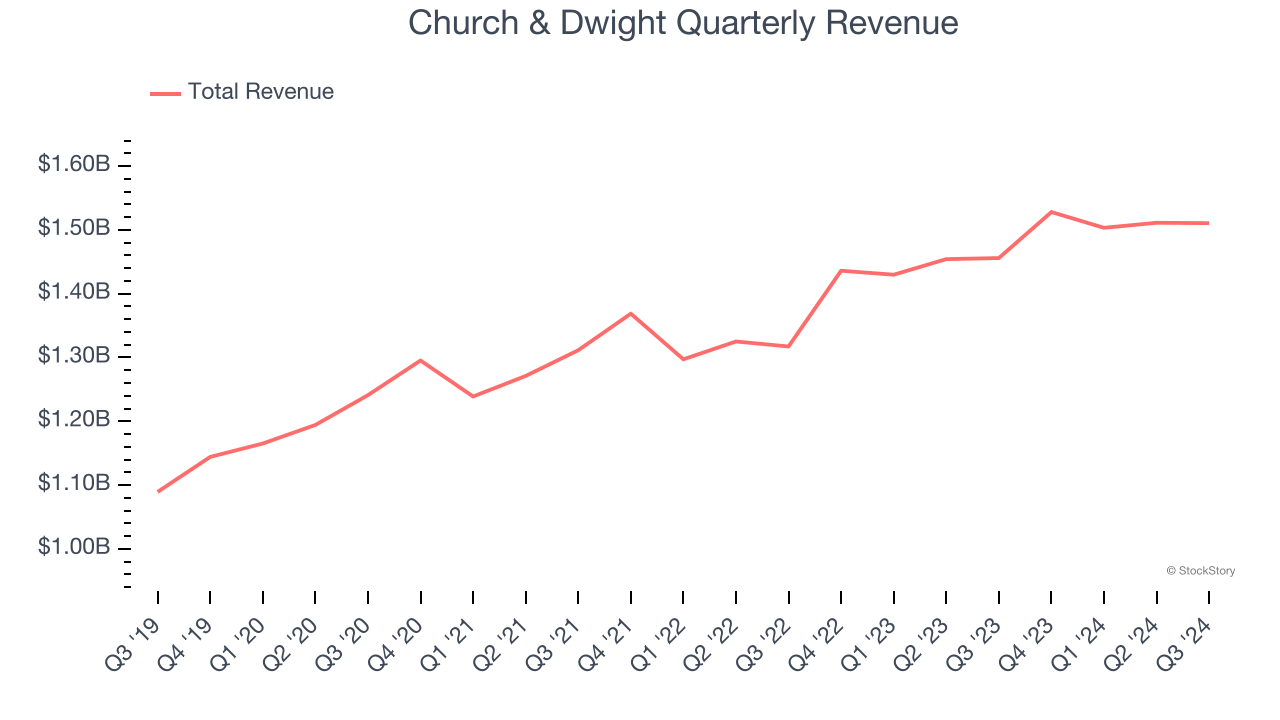

1. Long-Term Revenue Growth Disappoints

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Church & Dwight’s 5.8% annualized revenue growth over the last three years was mediocre. This fell short of our benchmark for the consumer staples sector.

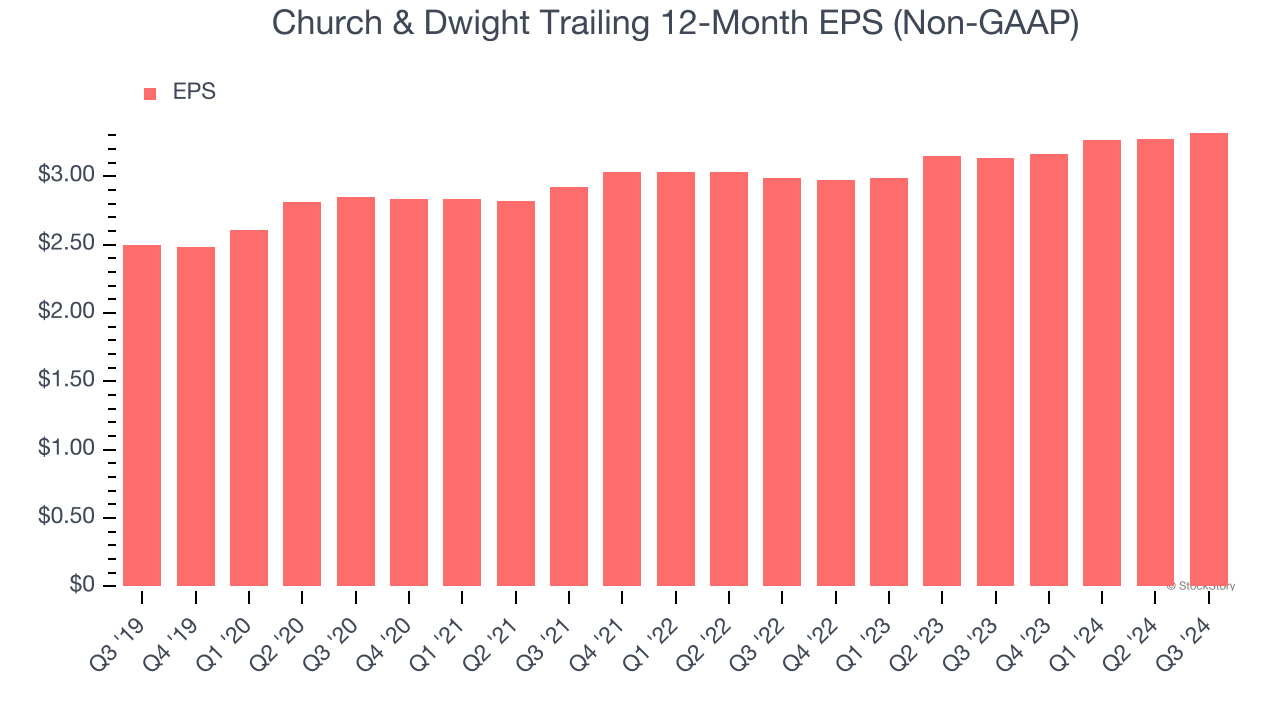

2. EPS Barely Growing

Analyzing the change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Church & Dwight’s EPS grew at an unimpressive 4.4% compounded annual growth rate over the last three years, lower than its 5.8% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

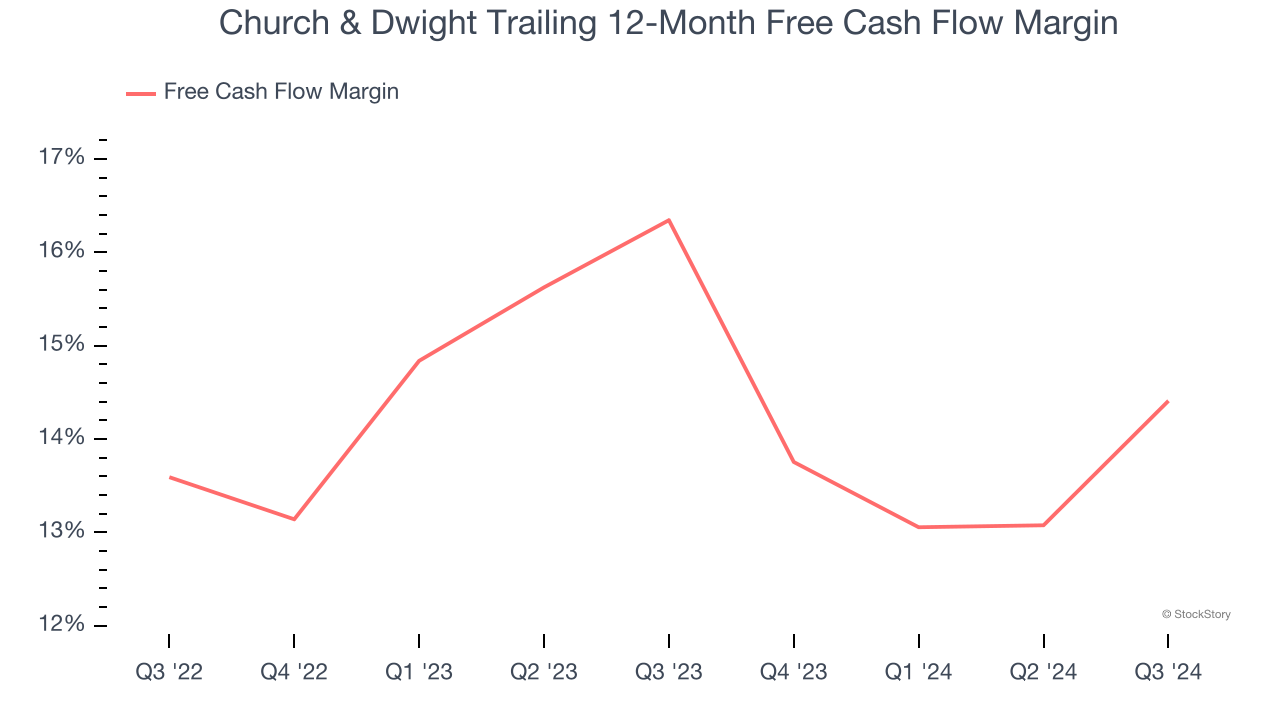

3. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Church & Dwight’s margin dropped by 1.9 percentage points over the last year. If its declines continue, it could signal higher capital intensity. Church & Dwight’s free cash flow margin for the trailing 12 months was 14.4%.

Final Judgment

Church & Dwight isn’t a terrible business, but it isn’t one of our picks. With its shares trailing the market in recent months, the stock trades at 29× forward price-to-earnings (or $105.68 per share). This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere. Let us point you toward MercadoLibre, the Amazon and PayPal of Latin America.

Stocks We Like More Than Church & Dwight

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.

More News

View More

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the following

Privacy Policy and Terms Of Service.