Financial News

Bowlero (NYSE:BOWL) Exceeds Q3 Expectations, Stock Soars

Upscale bowling alley chain Bowlero (NYSE: BOWL) beat Wall Street’s revenue expectations in Q3 CY2024, with sales up 14.4% year on year to $260.2 million. The company’s full-year revenue guidance of $1.26 billion at the midpoint came in 1.2% above analysts’ estimates.

Is now the time to buy Bowlero? Find out by accessing our full research report, it’s free.

Bowlero (BOWL) Q3 CY2024 Highlights:

- Revenue: $260.2 million vs analyst estimates of $249.5 million (4.3% beat)

- EBITDA: $62.94 million vs analyst estimates of $61.03 million (3.1% beat)

- The company slightly lifted its revenue guidance for the full year to $1.26 billion at the midpoint from $1.25 billion

- EBITDA guidance for the full year is $410 million at the midpoint, in line with analyst expectations

- Operating Margin: 5%, up from 2.4% in the same quarter last year

- EBITDA Margin: 24.2%, up from 22.9% in the same quarter last year

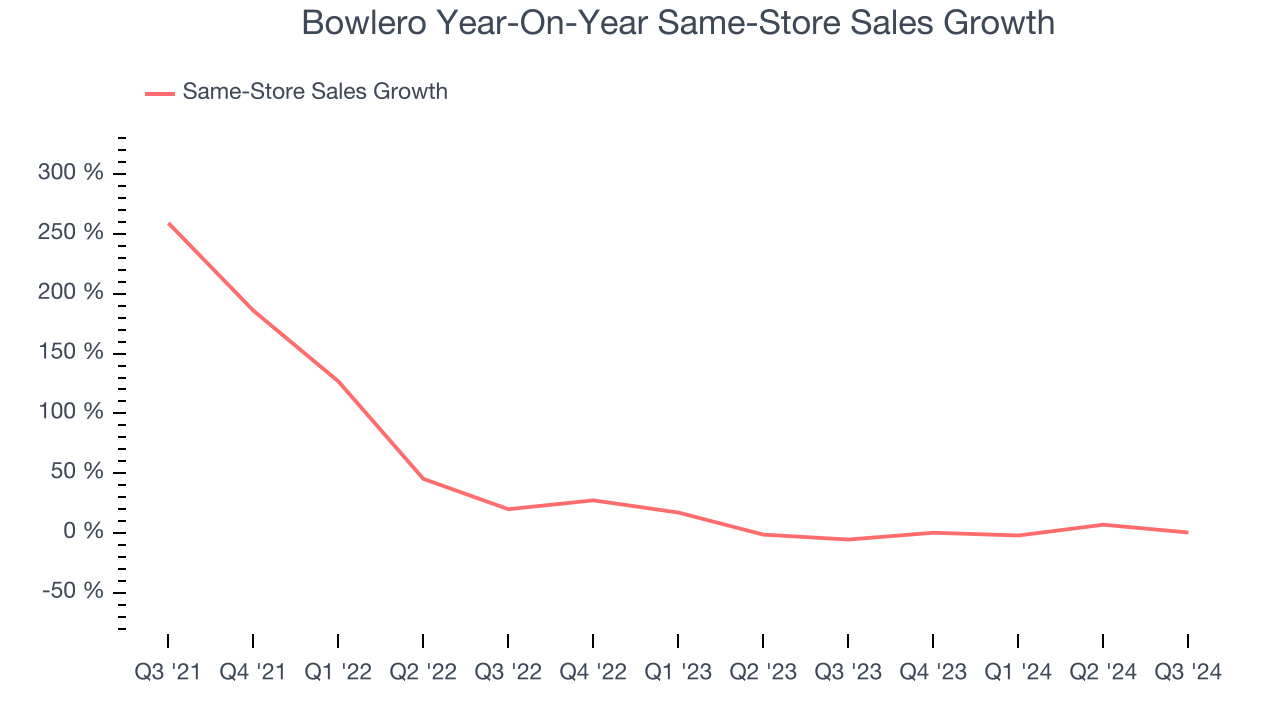

- Same-Store Sales were flat year on year (-5.5% in the same quarter last year)

- Market Capitalization: $1.53 billion

Company Overview

Operating over 300 locations globally, Bowlero (NYSE: BOWL) is a contemporary bowling company merging classic lanes with entertainment and deluxe food offerings.

Leisure Facilities

Leisure facilities companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted their spending from "things" to "experiences". Leisure facilities seek to benefit but must innovate to do so because of the industry's high competition and capital intensity.

Sales Growth

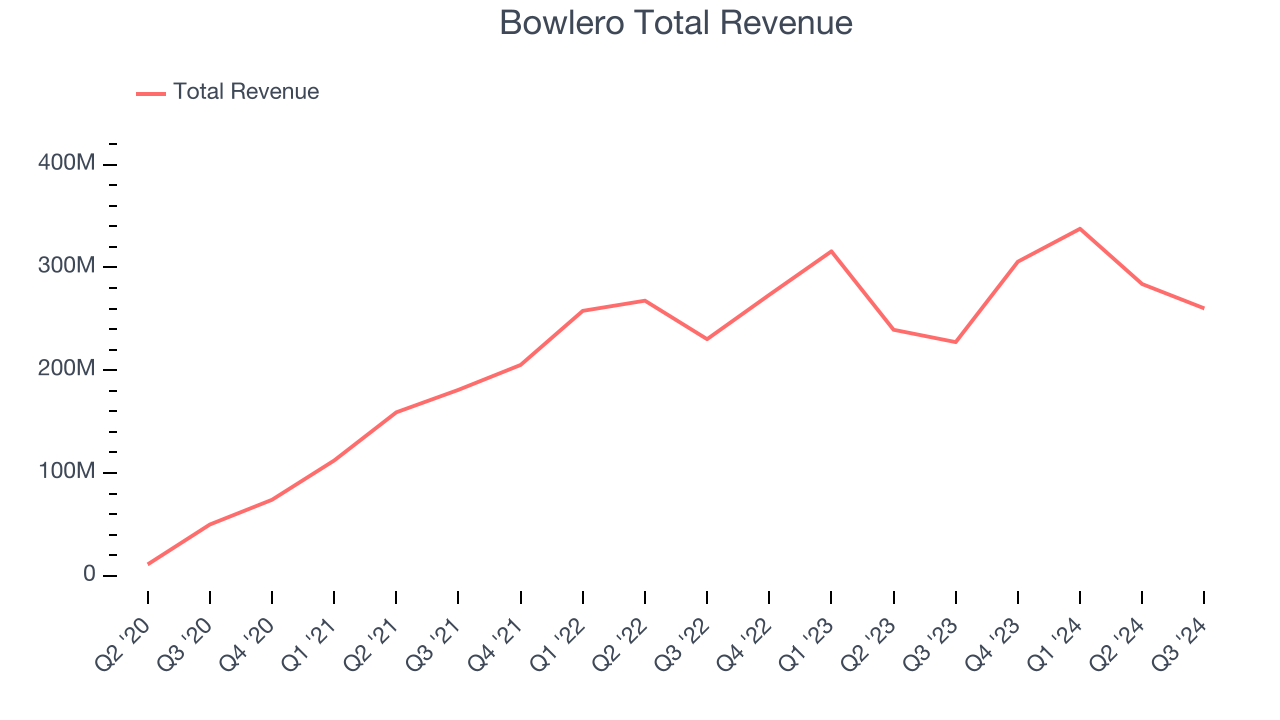

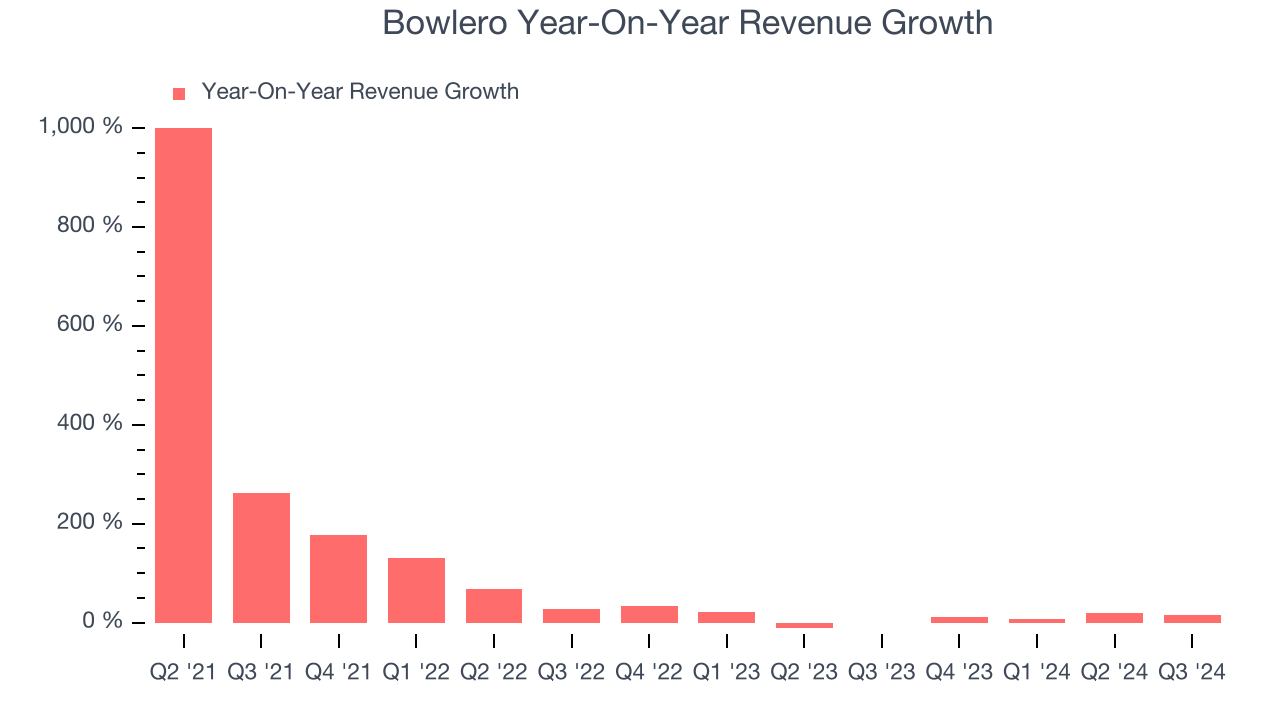

A company’s long-term performance can indicate its business quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, Bowlero’s sales grew at an incredible 72.8% compounded annual growth rate over the last four years. This is a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or emerging trend. Bowlero’s recent history shows its demand slowed significantly as its annualized revenue growth of 11.2% over the last two years is well below its four-year trend. Note that COVID hurt Bowlero’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

Bowlero also reports same-store sales, which show how much revenue its established locations generate. Over the last two years, Bowlero’s same-store sales averaged 5.4% year-on-year growth. Because this number is lower than its revenue growth, we can see the opening of new locations is boosting the company’s top-line performance.

This quarter, Bowlero reported year-on-year revenue growth of 14.4%, and its $260.2 million of revenue exceeded Wall Street’s estimates by 4.3%.

Looking ahead, sell-side analysts expect revenue to grow 5.7% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and illustrates the market thinks its products and services will face some demand challenges.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Cash Is King

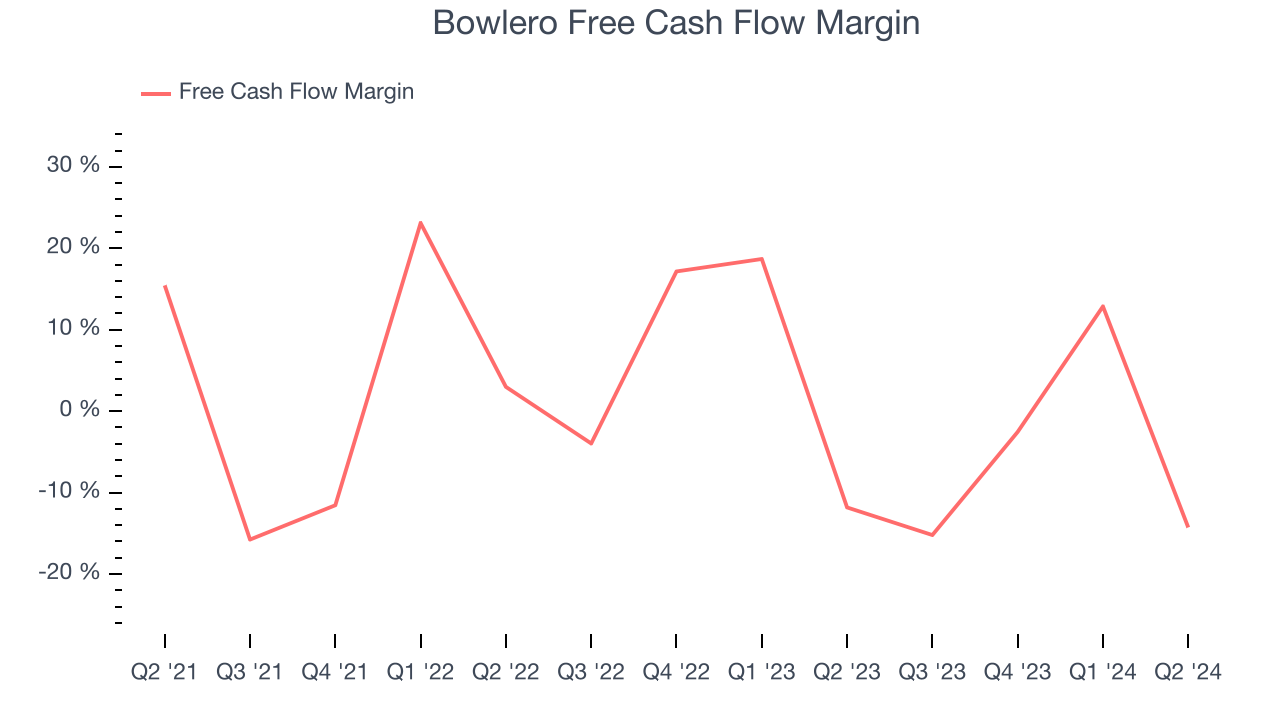

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Bowlero has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 1.9%, lousy for a consumer discretionary business.

The company’s cash burn increased from $34.59 million of lost cash in the same quarter last year . These numbers deviate from its longer-term margin, raising some eyebrows.

Key Takeaways from Bowlero’s Q3 Results

We enjoyed seeing Bowlero exceed analysts’ revenue and EBITDA expectations this quarter. We were also glad it slightly lifted its full-year revenue guidance. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 8.6% to $11.26 immediately following the results.

Sure, Bowlero had a solid quarter, but if we look at the bigger picture, is this stock a buy? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.

More News

View More

Recent Quotes

View MoreQuotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.