Financial News

Kontoor Brands (NYSE:KTB) Posts Better-Than-Expected Sales In Q3

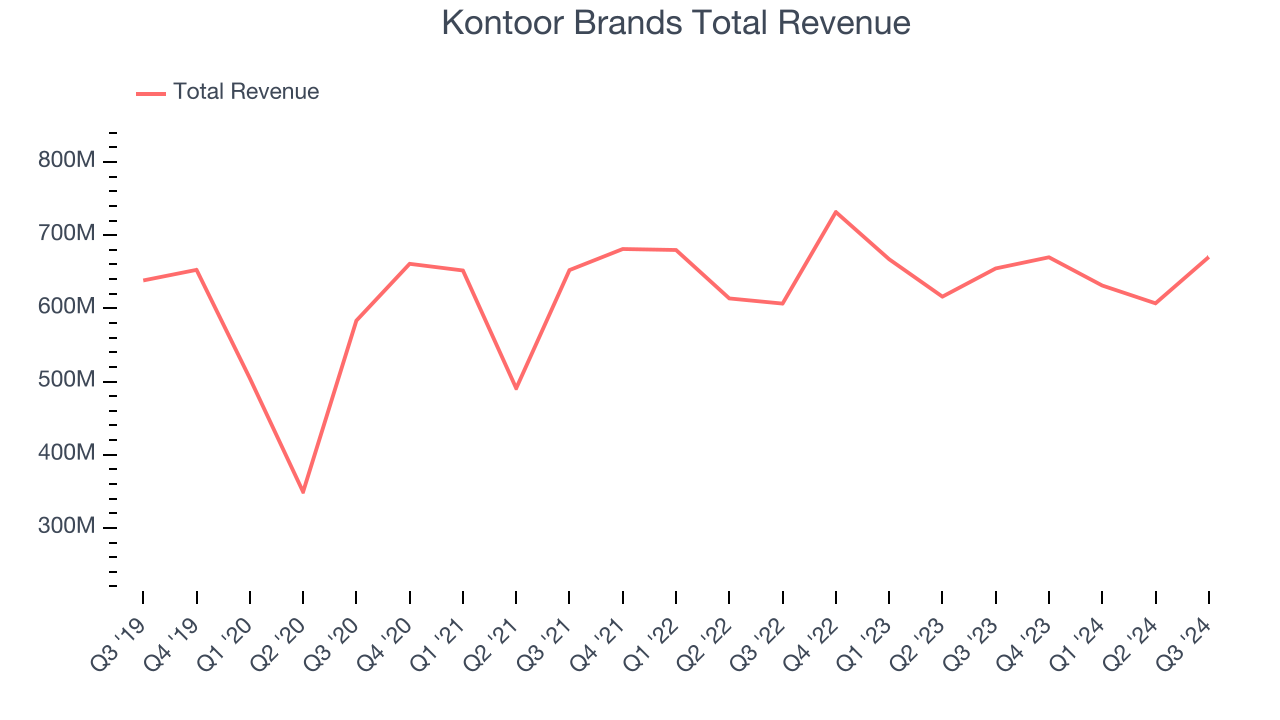

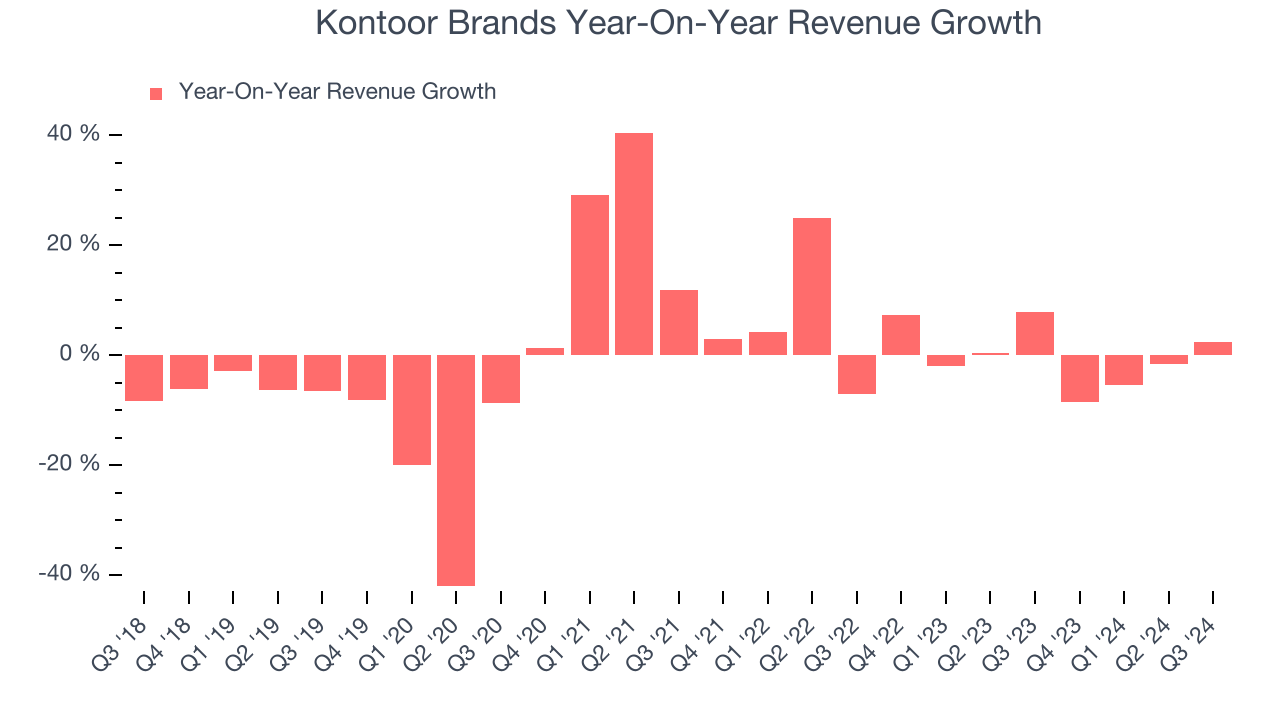

Clothing company Kontoor Brands (NYSE: KTB) reported Q3 CY2024 results topping the market’s revenue expectations, with sales up 2.4% year on year to $670.2 million. The company expects the full year’s revenue to be around $2.6 billion, close to analysts’ estimates. Its non-GAAP profit of $1.37 per share was also 8.6% above analysts’ consensus estimates.

Is now the time to buy Kontoor Brands? Find out by accessing our full research report, it’s free.

Kontoor Brands (KTB) Q3 CY2024 Highlights:

- Revenue: $670.2 million vs analyst estimates of $663.4 million (1% beat)

- Adjusted EPS: $1.37 vs analyst estimates of $1.26 (8.6% beat)

- EBITDA: $112.9 million vs analyst estimates of $106.3 million (6.3% beat)

- The company reconfirmed its revenue guidance for the full year of $2.6 billion at the midpoint

- Management slightly raised its full-year Adjusted EPS guidance to $4.83 at the midpoint

- Gross Margin (GAAP): 44.7%, up from 41.5% in the same quarter last year

- Operating Margin: 14.7%, up from 13.1% in the same quarter last year

- EBITDA Margin: 16.9%, up from 15.2% in the same quarter last year

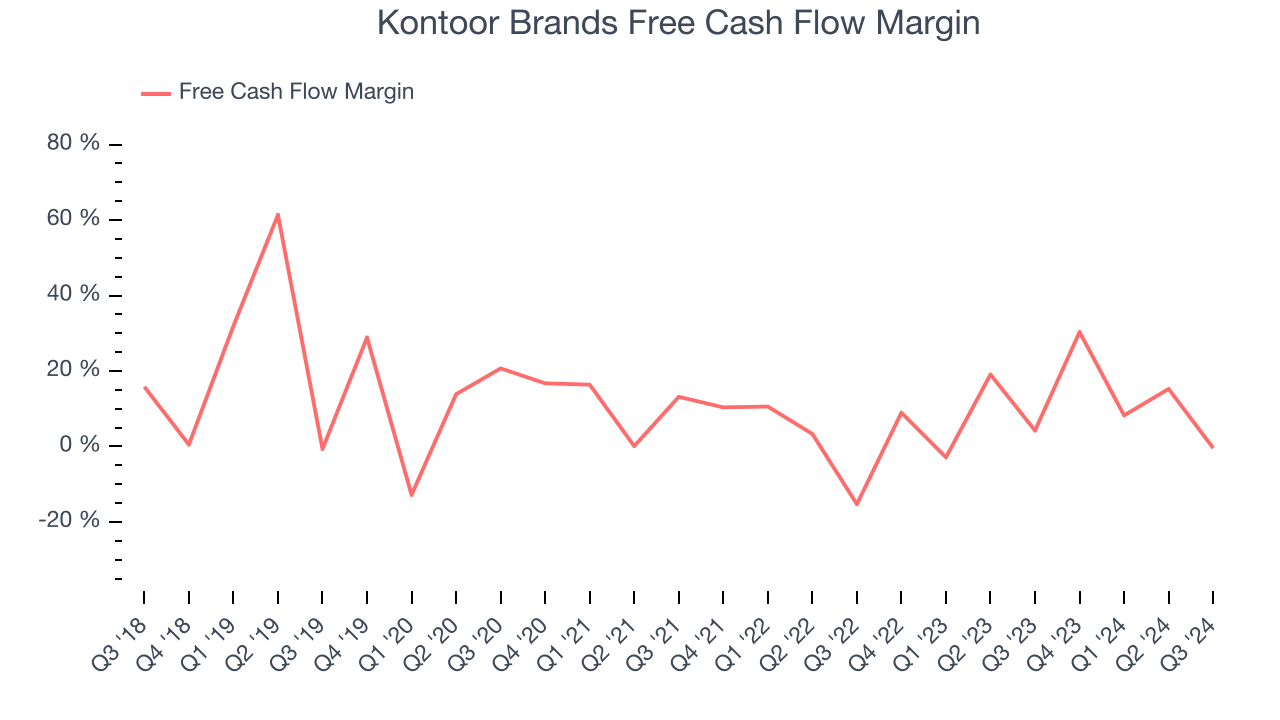

- Free Cash Flow was -$2.77 million, down from $27.57 million in the same quarter last year

- Market Capitalization: $4.26 billion

“Our third quarter results exceeded expectations driven by strong execution and business fundamentals,” said Scott Baxter, President, Chief Executive Officer and Chair of Kontoor Brands.

Company Overview

Founded in 2019 after separating from VF Corporation, Kontoor Brands (NYSE: KTB) is a clothing company known for its high-quality denim products.

Apparel, Accessories and Luxury Goods

Within apparel and accessories, not only do styles change more frequently today than decades past as fads travel through social media and the internet but consumers are also shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some apparel, accessories, and luxury goods companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Sales Growth

A company’s long-term performance can indicate its business quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Kontoor Brands’s demand was weak over the last five years as its sales were flat, a poor baseline for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Just like its five-year trend, Kontoor Brands’s revenue over the last two years was flat, suggesting it is in a slump.

This quarter, Kontoor Brands reported modest year-on-year revenue growth of 2.4% but beat Wall Street’s estimates by 1%.

Looking ahead, sell-side analysts expect revenue to grow 3.2% over the next 12 months, an improvement versus the last two years. While this projection shows the market thinks its newer products and services will spur better performance, it is still below the sector average.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Kontoor Brands has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 10.2% over the last two years, slightly better than the broader consumer discretionary sector.

Kontoor Brands broke even from a free cash flow perspective in Q3. The company’s cash profitability regressed as it was 4.6 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Key Takeaways from Kontoor Brands’s Q3 Results

It was good to see Kontoor Brands beat analysts’ EBITDA and EPS expectations this quarter. We were also glad it raised its full-year EPS outlook. On the other hand, its full-year revenue guidance was underwhelming. Zooming out, we think this was a decent quarter featuring some areas of strength but also some blemishes. The stock remained flat at $76.56 immediately following the results.

So do we think Kontoor Brands is an attractive buy at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.