Financial News

Luxfer (NYSE:LXFR) Beats Expectations in Strong Q3, Stock Soars

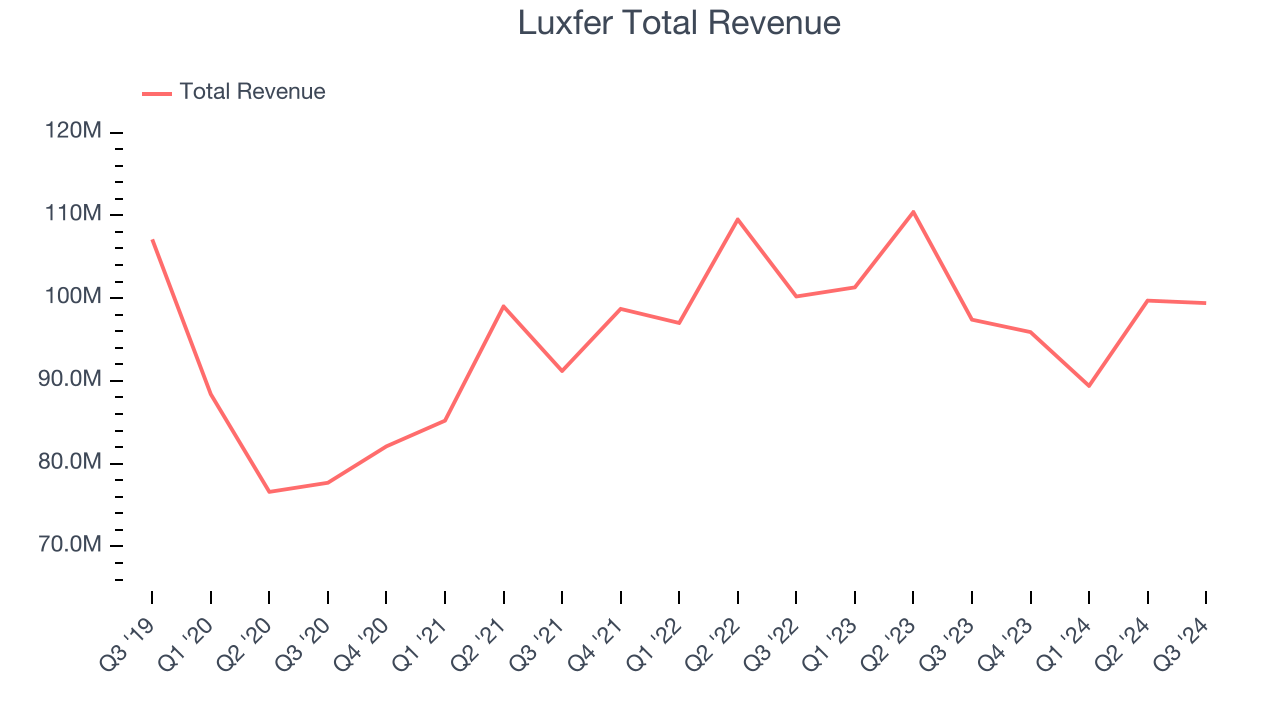

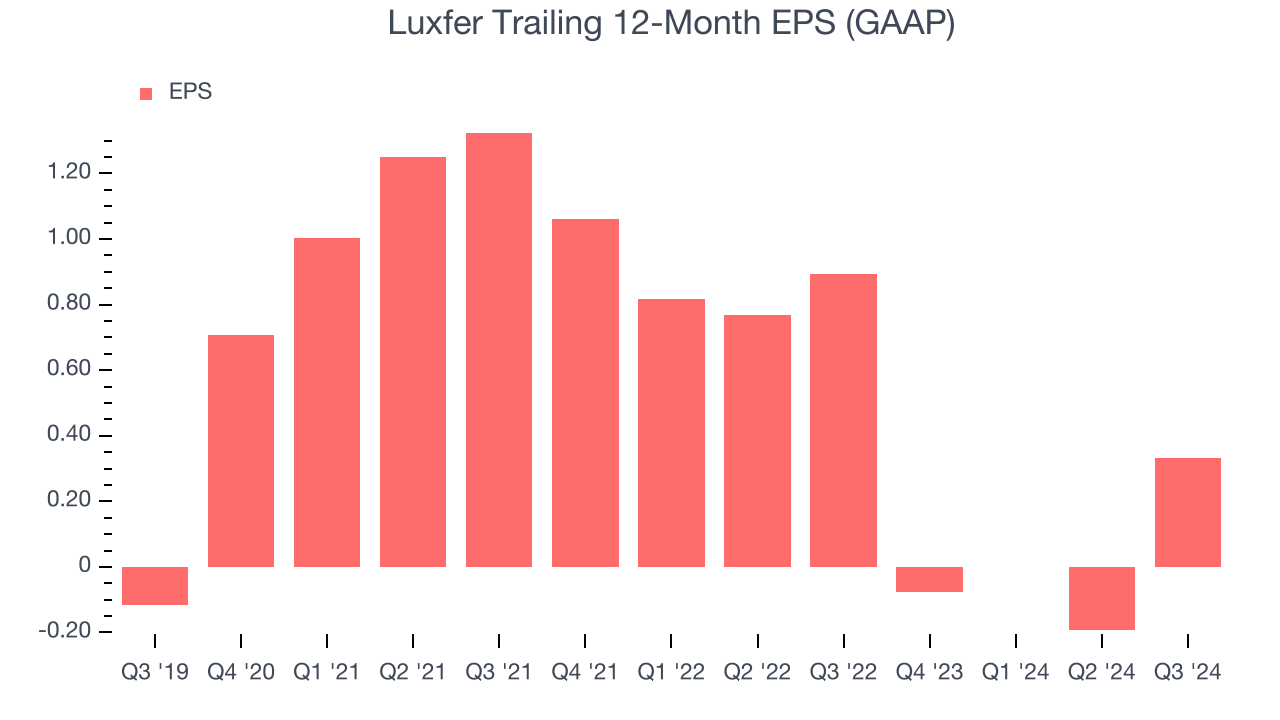

Speciality material and gas containment company Luxfer (NYSE: LXFR) announced better-than-expected revenue in Q3 CY2024, with sales up 2.1% year on year to $99.4 million. Its GAAP profit of $0.47 per share was also 213% above analysts’ consensus estimates.

Is now the time to buy Luxfer? Find out by accessing our full research report, it’s free.

Luxfer (LXFR) Q3 CY2024 Highlights:

- Revenue: $99.4 million vs analyst estimates of $85.8 million (15.9% beat)

- EPS: $0.47 vs analyst estimates of $0.15 ($0.32 beat)

- EBITDA: $15.4 million vs analyst estimates of $10.2 million (51% beat)

- Gross Margin (GAAP): 22.5%, up from 15% in the same quarter last year

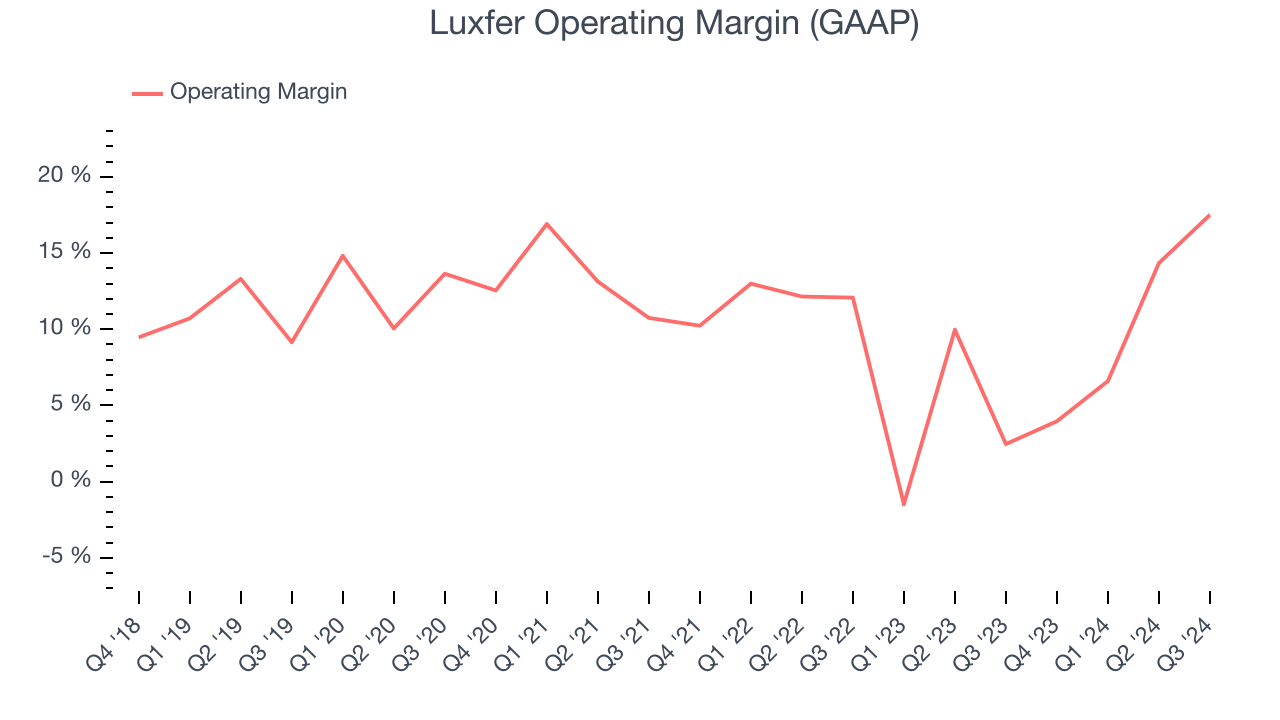

- Operating Margin: 17.5%, up from 2.5% in the same quarter last year

- EBITDA Margin: 15.5%, up from 6.3% in the same quarter last year

- Market Capitalization: $352.2 million

Company Overview

With its magnesium alloys used in the construction of the famous Spirit of St. Louis aircraft, Luxfer (NYSE: LXFR) offers specialized materials, components, and gas containment devices to various industries.

General Industrial Machinery

Automation that increases efficiency and connected equipment that collects analyzable data have been trending, creating new demand for general industrial machinery companies. Those who innovate and create digitized solutions can spur sales and speed up replacement cycles, but all general industrial machinery companies are still at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Sales Growth

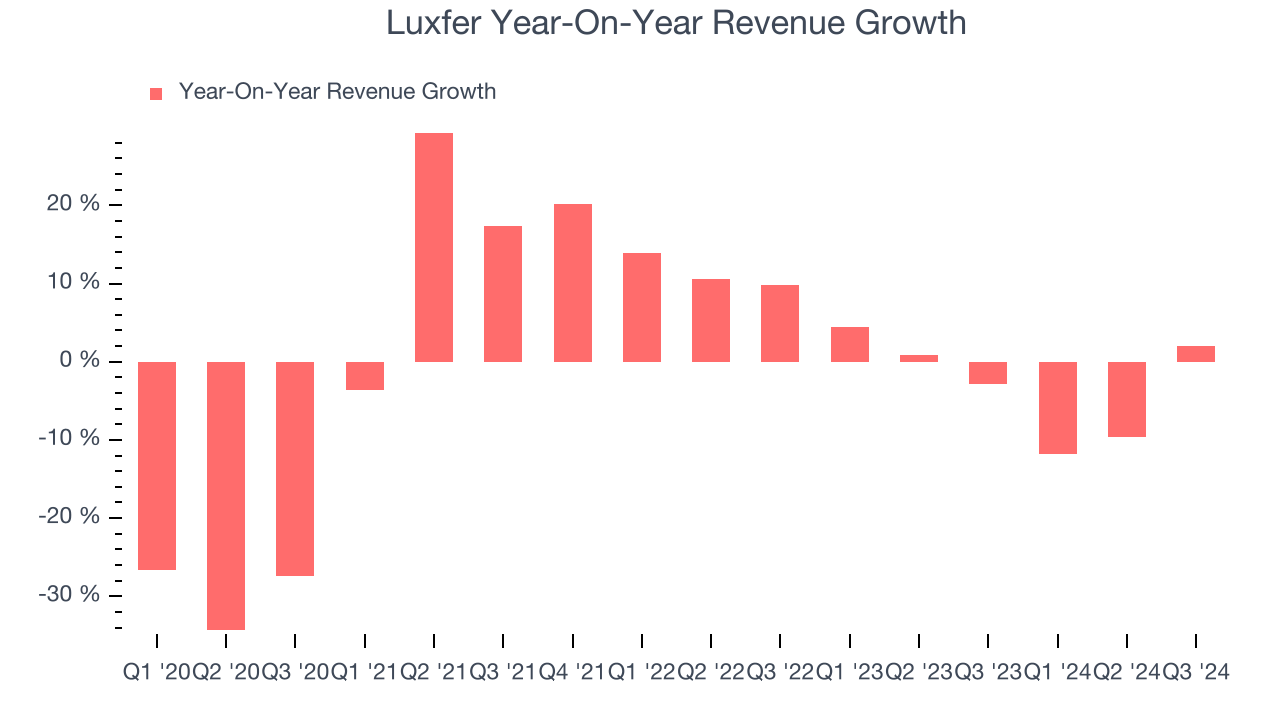

A company’s long-term performance is an indicator of its overall business quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for multiple years. Over the last five years, Luxfer’s revenue declined by 3.3% per year. This shows demand was weak, a rough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Luxfer’s annualized revenue declines of 2.6% over the last two years align with its five-year trend, suggesting its demand consistently shrunk.

This quarter, Luxfer reported modest year-on-year revenue growth of 2.1% but beat Wall Street’s estimates by 15.9%.

Looking ahead, sell-side analysts expect revenue to grow 1.1% over the next 12 months. While this projection illustrates the market believes its newer products and services will fuel better performance, it is still below average for the sector.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Luxfer has managed its cost base well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 10.6%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Analyzing the trend in its profitability, Luxfer’s annual operating margin might have seen some fluctuations but has generally stayed the same over the last five years, highlighting the long-term consistency of its business.

In Q3, Luxfer generated an operating profit margin of 17.5%, up 15 percentage points year on year. The increase was solid, and since its operating margin rose more than its gross margin, we can infer it was recently more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth was profitable.

Luxfer’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

Like with revenue, we analyze EPS over a more recent period because it can give insight into an emerging theme or development for the business.

Sadly for Luxfer, its EPS declined by more than its revenue over the last two years, dropping 39.1%. However, its operating margin actually expanded during this timeframe, telling us that non-fundamental factors affected its ultimate earnings.

In Q3, Luxfer reported EPS at $0.47, up from negative $0.05 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Luxfer’s full-year EPS of $0.33 to grow by 183%.

Key Takeaways from Luxfer’s Q3 Results

We were impressed by how significantly Luxfer blew past analysts’ revenue, EBITDA, and EPS expectations this quarter. Zooming out, we think this was a solid quarter. The stock traded up 6.2% to $13.55 immediately after reporting.

Luxfer may have had a good quarter, but does that mean you should invest right now?When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.

More News

View More

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the following

Privacy Policy and Terms Of Service.