Financial News

Watsco (NYSE:WSO) Misses Q3 Sales Targets

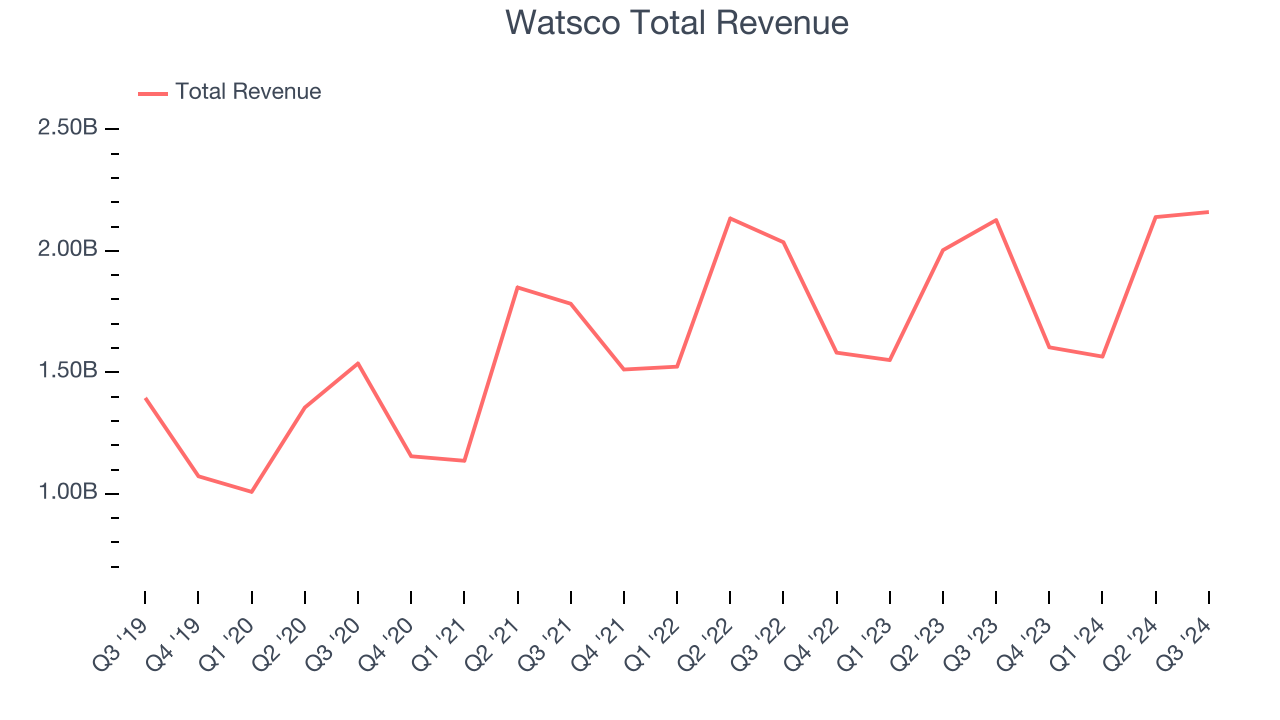

Equipment distributor Watsco (NYSE: WSO) fell short of the market’s revenue expectations in Q3 CY2024 as sales only rose 1.6% year on year to $2.16 billion. Its GAAP profit of $4.22 per share was also 10.9% below analysts’ consensus estimates.

Is now the time to buy Watsco? Find out by accessing our full research report, it’s free.

Watsco (WSO) Q3 CY2024 Highlights:

- Revenue: $2.16 billion vs analyst estimates of $2.24 billion (3.6% miss)

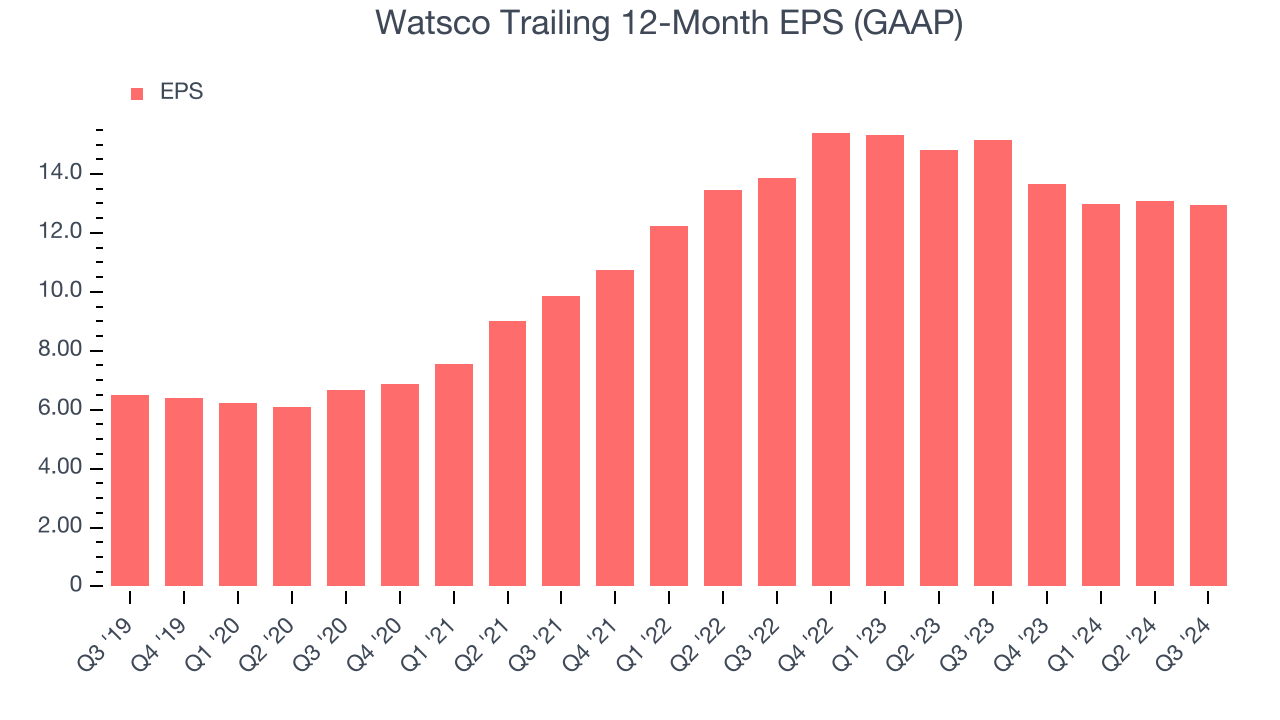

- EPS: $4.22 vs analyst expectations of $4.74 (10.9% miss)

- EBITDA: $285.7 million vs analyst estimates of $290.1 million (1.5% miss)

- Gross Margin (GAAP): 26.2%, in line with the same quarter last year

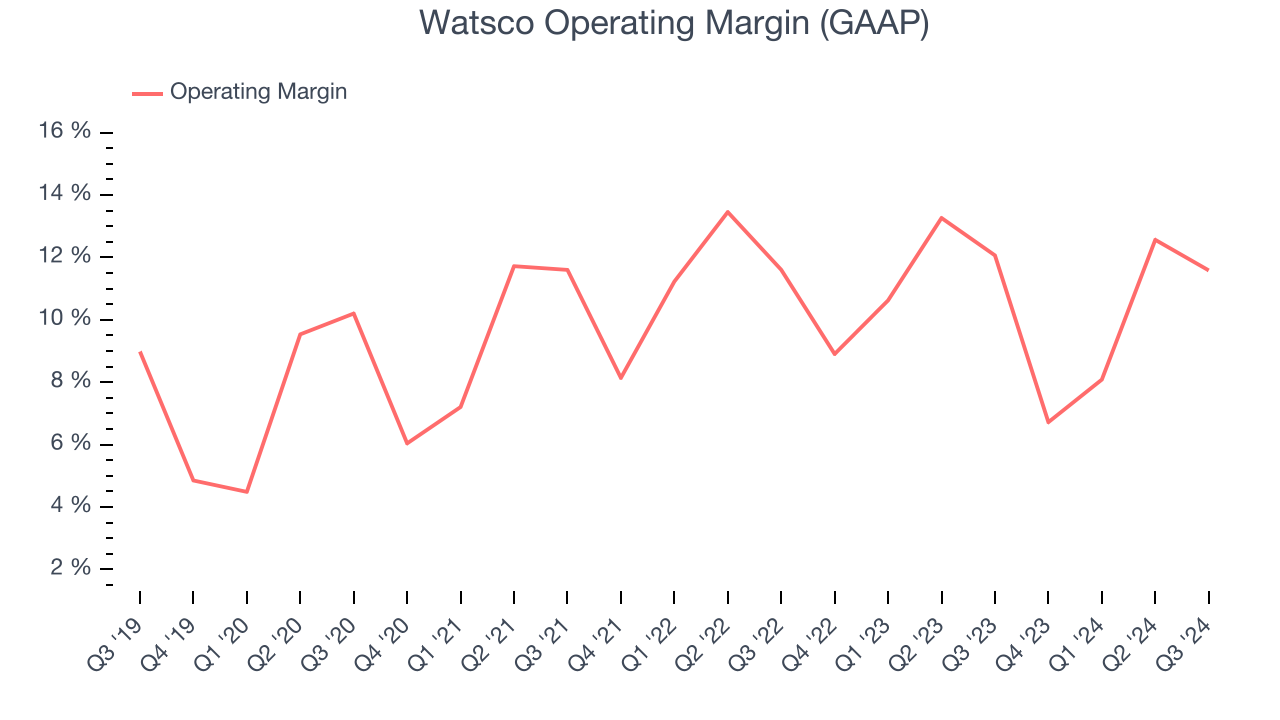

- Operating Margin: 11.6%, in line with the same quarter last year

- EBITDA Margin: 13.2%, in line with the same quarter last year

- Free Cash Flow Margin: 10.3%, down from 16.1% in the same quarter last year

- Same-Store Sales were flat year on year (4% in the same quarter last year)

- Market Capitalization: $18.29 billion

Albert H. Nahmad, Chairman and CEO commented: “During the third quarter, Watsco achieved record sales and net income, produced strong cash flow and made further strides to improve operating efficiency across its network. We believe the market environment for HVAC products stabilized this year, and we look forward to helping our customers navigate next year’s regulatory transition toward the new A2L systems. This regulatory change will ultimately impact approximately 60% of our sales and offers our contractor customers the opportunity to upgrade older HVAC systems with new products that are both more energy-efficient and environmentally-friendly.”

Company Overview

Originally a manufacturing company, Watsco (NYSE: WSO) today only distributes air conditioning, heating, and refrigeration equipment, as well as related parts and supplies.

Infrastructure Distributors

Focusing on narrow product categories that can lead to economies of scale, infrastructure distributors sell essential goods that often enjoy more predictable revenue streams. For example, the ongoing inspection, maintenance, and replacement of pipes and water pumps are critical to a functioning society, rendering them non-discretionary. Lately, innovation to address trends like water conservation has driven incremental sales. But like the broader industrials sector, infrastructure distributors are also at the whim of economic cycles as external factors like interest rates can greatly impact commercial and residential construction projects that drive demand for infrastructure products.

Sales Growth

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Watsco’s 9.8% annualized revenue growth over the last five years was solid. This shows it was successful in expanding, a useful starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Watsco’s recent history shows its demand slowed as its annualized revenue growth of 1.8% over the last two years is below its five-year trend.

We can dig further into the company’s revenue dynamics by analyzing its same-store sales, which show how much revenue its established locations generate. Over the last two years, Watsco’s same-store sales were flat. This number doesn’t surprise us as it’s in line with its revenue growth.

This quarter, Watsco’s revenue grew 1.6% year on year to $2.16 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 8.5% over the next 12 months, an acceleration versus the last two years. This projection is above the sector average and shows the market thinks its newer products and services will spur faster growth.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Looking at the trend in its profitability, Watsco’s annual operating margin rose by 2.4 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q3, Watsco generated an operating profit margin of 11.6%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

We track the long-term growth in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth was profitable.

Watsco’s EPS grew at a spectacular 14.8% compounded annual growth rate over the last five years, higher than its 9.8% annualized revenue growth. This tells us the company became more profitable as it expanded.

Diving into Watsco’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, Watsco’s operating margin was flat this quarter but expanded by 2.4 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business. For Watsco, its two-year annual EPS declines of 3.4% mark a reversal from its (seemingly) healthy five-year trend. We hope Watsco can return to earnings growth in the future.

In Q3, Watsco reported EPS at $4.22, down from $4.35 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Watsco’s full-year EPS of $12.94 to grow by 17%.

Key Takeaways from Watsco’s Q3 Results

We struggled to find many strong positives in these results as its revenue and fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 3.1% to $470 immediately following the results.

Watsco didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now?We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy.We cover that in our actionable full research report which you can read here, it’s free.

More News

View More

Recent Quotes

View MoreQuotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.