Financial News

Micron’s 2026 Earnings Upside Makes MU Stock Hard to Ignore

Micron (MU) stock has been on a remarkable run, surging about 282% over the past year. Such a sharp rally would normally raise concerns about valuation, but Micron’s solid earnings outlook suggests the rally is far from over.

The primary driver behind Micron’s rally is the accelerating demand for its memory and storage solutions, led by the advancements in artificial intelligence (AI) and other compute-intensive workloads. Micron’s broad portfolio of DRAM and NAND products positions the company well to capitalize on the opportunities stemming from the multi-year data-center buildout.

What makes Micron’s investment case more compelling is the disconnect between the MU stock price and its projected earnings power. Wall Street expects the company’s EPS to expand dramatically by fiscal 2026, reflecting both improving pricing conditions in the memory market and stronger end-market demand. On those forward estimates, Micron’s valuation looks surprisingly modest, suggesting the market may not yet be fully pricing in the magnitude of the earnings growth.

Looking beyond 2026, Micron also appears well-positioned to maintain momentum into fiscal 2027, even as year-over-year (YOY) comparisons become more challenging. Structural demand from AI, cloud infrastructure, and advanced computing, along with higher pricing, could continue to push margins and earnings higher.

Analysts See a 300%-Plus Jump in Micron’s EPS

Micron has entered fiscal 2026 with solid momentum, delivering a first-quarter performance that reflects a meaningful improvement in its underlying business. The company posted strong revenue across all of its operating segments, reflecting solid, broad-based demand for its memory and storage products. Profitability expanded sharply, signaling that Micron is benefiting from higher sales and a much more favorable industry backdrop.

Over recent quarters, Micron has consistently produced solid earnings, and current industry conditions suggest that this trend may continue. The memory market is experiencing tighter supply, which is helping support higher pricing. For Micron, an increase in average selling prices can drive significant gains in margins and earnings.

During Q1, the company benefited from higher shipment volumes, better pricing, and continued cost discipline, all of which translated into a meaningful acceleration in profitability. Gross margins expanded sharply as these factors took hold. On an adjusted basis, Micron’s gross margin rose to 56.8%, a substantial improvement from 45.7% in the prior quarter and 39.5% a year earlier. This margin expansion highlights the operating leverage inherent in the business when demand strengthens and pricing power improves.

The strength was even more evident at the operating profit level. Adjusted operating margin reached 47%, reflecting a 12-percentage-point sequential increase and an improvement of 19.5 percentage points YOY. This operating momentum also flowed directly through to the bottom line. Adjusted EPS surged to $4.78, representing a 167% YOY increase.

Looking ahead, Micron appears well-positioned to sustain this performance. Demand driven by AI and data center expansion continues to accelerate, while supply constraints across the industry remain supportive of pricing. Management has indicated that these tight market conditions are likely to extend beyond calendar year 2026, leading to higher revenue growth and margin expansion over multiple quarters.

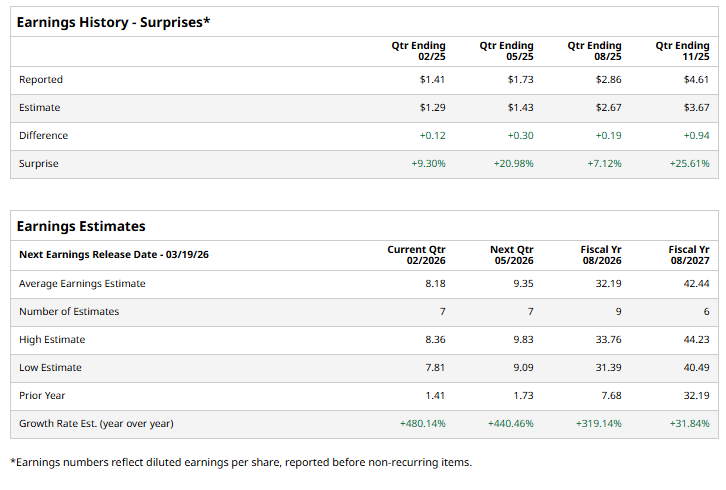

Analysts currently expect Micron to generate EPS of $32.19 in fiscal 2026, implying YOY growth of more than 300% — 319% to be more precise. Given the company’s strong start to the year and the supportive industry environment, there is potential for earnings expectations to rise further if pricing and demand remain firm.

Micron Stock Is Hard to Ignore

Even after a strong rally, MU stock appears attractively valued relative to its earnings potential. Micron currently trades at about 12 times forward earnings, indicating the stock is deeply undervalued relative to its projected earnings. Micron’s low valuation and solid growth expectations suggest there is meaningful upside for MU stock.

Wall Street analysts remain optimistic about Micron’s prospects, maintaining a consensus “Strong Buy” rating based on 41 analysts with coverage.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Why the Big 3 Cruise Stocks Are Looking More and More Like Sinking Ships

- Buy the Dip in Apple Stock Before January 29, According to Goldman Sachs

- Micron’s 2026 Earnings Upside Makes MU Stock Hard to Ignore

- Blue Origin Is Gunning for AST SpaceMobile. Should You Sell ASTS Stock Now or Keep Betting on Gains?

More News

View More

Recent Quotes

View MoreQuotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.