Financial News

Bank of Idaho Holding Company Reports First Quarter 2024 Financial Results

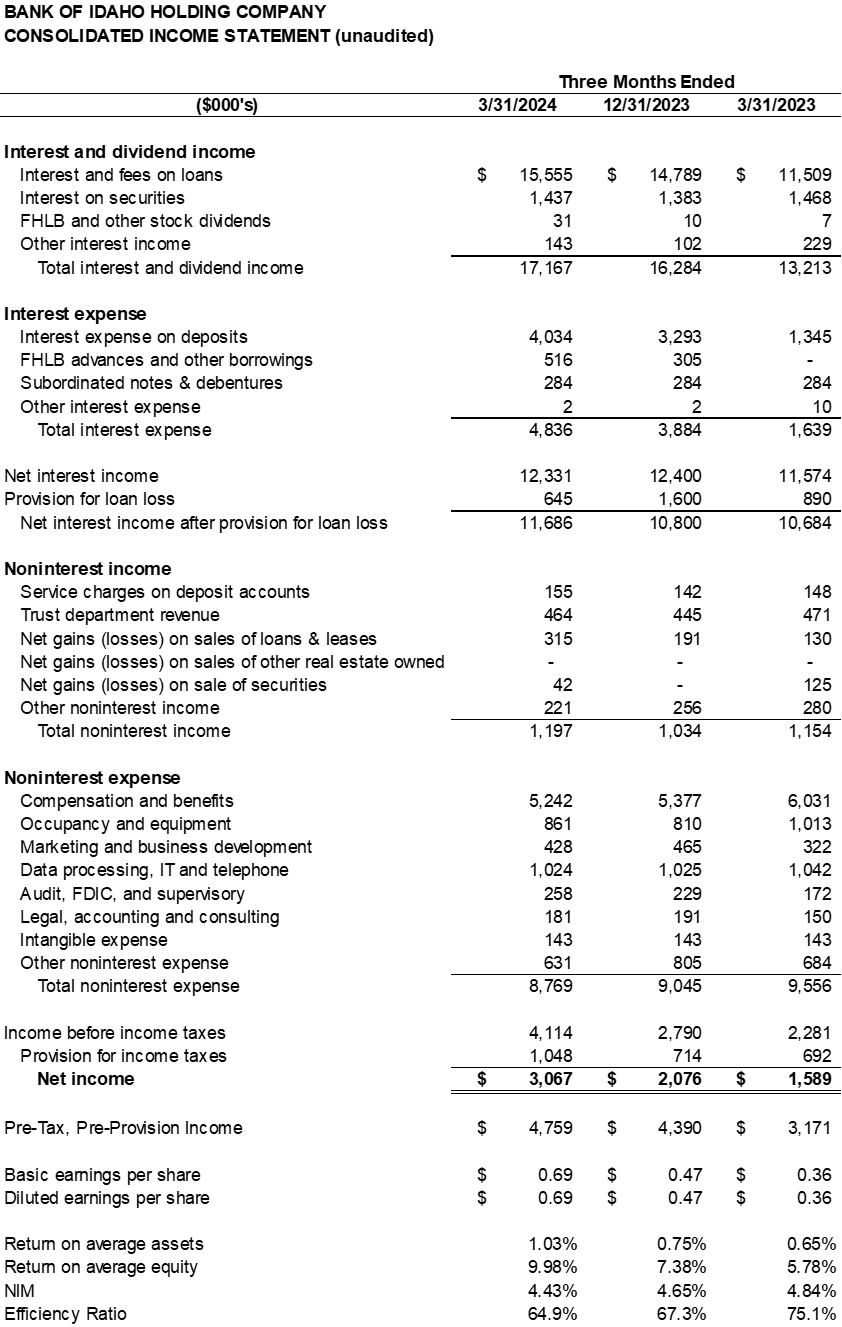

IDAHO FALLS, ID / ACCESSWIRE / April 23, 2024 / Bank of Idaho Holding Company (the "Company") (OTCQX:BOID), the holding company for Bank of Idaho (the "Bank"), today announced its unaudited financial results for the quarter ended March 31, 2024. The Company reported consolidated net income of $3,067,000, or $0.69 per diluted share, for the first quarter of 2024. This compares to $2,076,000, or $0.47 per diluted share, for the fourth quarter of 2023, and $1,589,000 or $0.36 per diluted share, for the first quarter of 2023.

"We are pleased to announce an excellent first quarter with the Bank of Idaho generating $4.8 million in pre-tax, pre-provision income and $0.69 earnings per share. Our commitment to prioritizing credit and pricing discipline continues to set the foundation for ongoing growth," said Jeff Newgard, Chairman, President, and CEO of Bank of Idaho. "As a result, portfolio loan production for the first quarter was $72.8 million. We are positioned in dynamic geographic markets, which produce strong loan growth. We remain confident for the remainder of 2024 and beyond."

Quarterly Summary

Loans held for investment grew $33.9 million, or 3.8%, in Q1 2024 and increased $173.6 million, or 23.4%, from Q1 2023.

Total core deposits increased $30.9 million, or 3.3%, in Q1 2024 and were up $101.6 million, or 12.0%, from Q1 2023.

Pre-tax, pre-provision ("PTPP") net income was $4.76 million in Q1 2024, compared to $4.39 million in Q4 2023 and $3.17 million in Q1 2023.

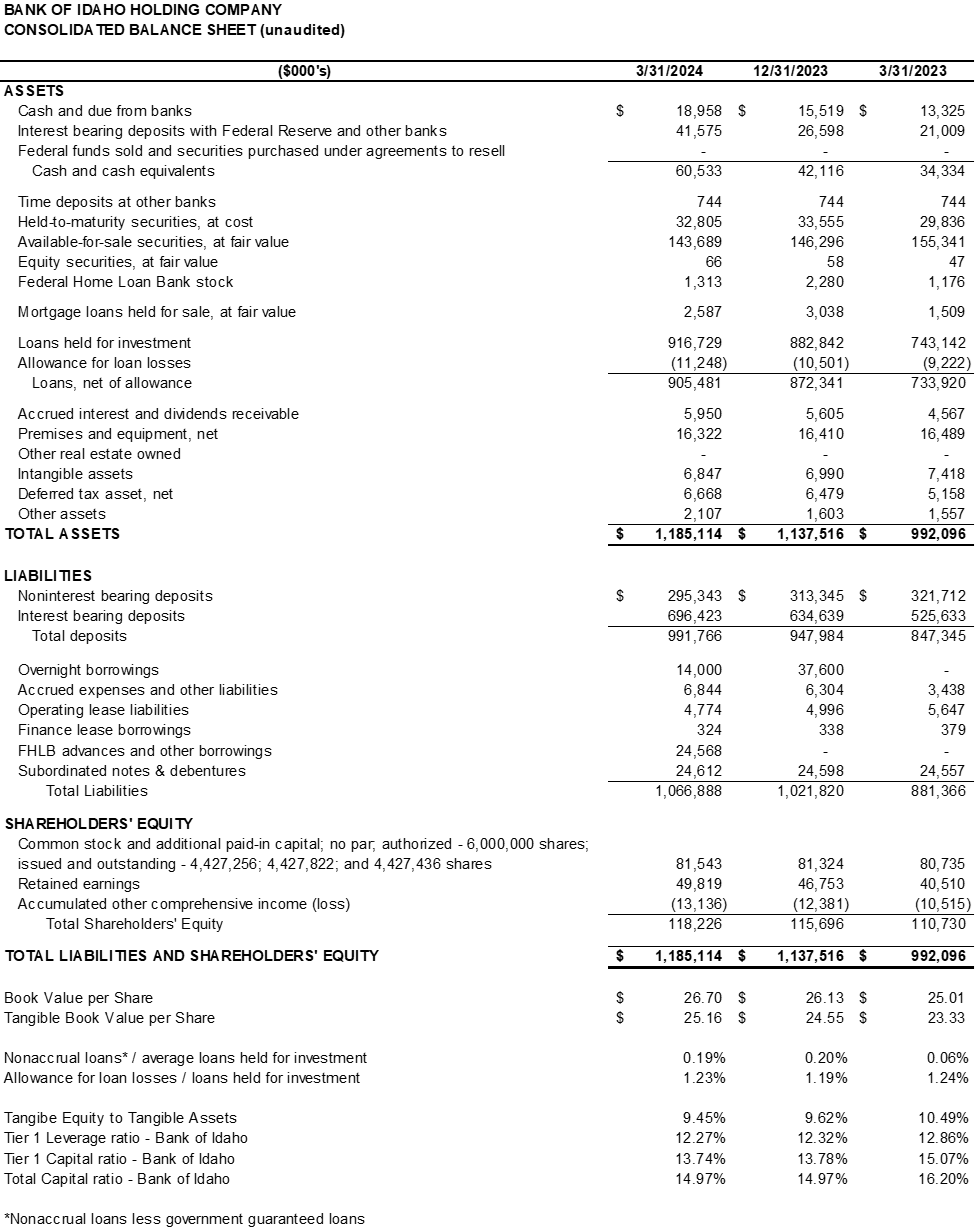

Tangible book value ("TBV") per share increased to $25.16, or 2.5%, from $24.55 at Q4 2023, and increased 7.8% from $23.33 at Q1 2023. The increase in TBV is attributable to earnings offset by an increase in unrealized losses within our securities portfolio.

Operating Results

Net income for the first quarter of 2024 was $3,067,000, or $0.69 per diluted share, compared to net income of $2,076,000, or $0.47 per diluted share, for Q4 2023, and $1,589,000, or $0.36 per diluted share, for the same quarter last year. The increase from the prior quarter was the result of a decrease in provision expense of $955,000, an increase of $163,000 in non-interest income, a decrease in non-interest expense of $276,000 offset by an increase of $334,000 in tax expense.

Net interest income for Q1 2024 was $12.3 million, a marginal decrease of $70,000, or 0.6%, from the prior quarter as interest income kept pace with the increases in interest expense due to new loan production being backloaded in the quarter.

Net interest margin for the first quarter of 2024 was 4.43% compared to 4.65% in the previous quarter and 4.84% for the same quarter last year. While there continues to be margin pressure from the Fed's restrictive rate policy and liquidity tightening mandate, we continue to see healthy loan demand at attractive spreads that allows us to defend our operating margins. While the cost of funding continues to increase, the growth in earning assets at current market yields is expected to outpace the funding cost pressures. Relative to the first quarter of 2023, the consolidated net interest margin decreased due to rising deposit costs.

Noninterest income, including net gains and losses, for Q1 2024 was $1,197,000, an increase of $163,000, or 15.8%, from $1,034,000 in Q4 2023. The increase was attributable to generating more income from gain on loan sales in the current quarter and a one-time gain on sale of securities. Relative to the first quarter of 2023, noninterest income increased $43,000, or 3.7%.

Noninterest expense of $8.77 million in Q1 2024 was a decrease of $276,000, or 3.0%, from $9.05 million in Q4 2023 and a $788,000, or 8.2%, decrease from $9.56 million in Q1 2023. The decrease from Q4 2023 was due to lower compensation expenses and other noninterest expenses. Compensation expense in the first quarter of 2023 included a one-time catch-up in incentive expense. The Company's efficiency ratio was 64.9% for Q1 2024, compared to 67.3% for Q4 2023, and 75.1% for Q1 2023.

Total assets were $1.19 billion as of March 31, 2024, an increase of $47.6 million, or 4.2%, from $1.14 billion at December 31, 2023. First quarter 2024 balance sheet activity was characterized by $33.9 million, or 3.8%, growth in portfolio loans. Loans were funded by the growth in deposits of $43.8 million, or 4.6%. Cash and cash equivalents increased $18.4 million along with an increase of $1.0 million in total borrowings. Prior to the change in Federal Reserve's Bank Term Funding Program ("BTFP") rate structure, we borrowed $24.6 million from the BTFP at a rate of 4.87% and paid down FHLB overnight borrowings.

Loans held for investment were $916.7 million as of March 31, 2024, an increase of $33.9 million, or 3.8%, from $882.8 million as of December 31, 2023, and an increase of $173.6 million, or 23.4%, from $743.1 million as of March 31, 2023. The increase in total loans held for investment from the previous quarter came from growth in all loan categories, with the largest increase in the Bank's commercial and commercial real estate loans. We continue to see significant lending opportunities across our markets.

Deposits were $991.8 million as of March 31, 2024, up $43.8 million, or 4.6%, from the previous quarter, and up $144.4 million, or 17.0%, from the same quarter last year. Our deposit portfolio continues to undergo a remixing as customers move deposits from noninterest-bearing accounts into yield seeking accounts; however, this has slowed since the start of the year. We continue to see organic deposit growth opportunities within our markets but at an elevated cost due competition from both bank and non-bank organizations. Noninterest bearing deposits represented 30% of total deposits and 31% of core deposits as of March 31, 2024, compared to 33% as of December 31, 2023, and 38% as of March 31, 2023.

Borrowings were $63.2 million as of March 31, 2024, which consisted of $24.6 million of Company subordinated debt, $24.6 million of BTFP advances, and $14.0 million of overnight borrowings compared to $24.6 million of subordinated debt and $37.6 million in overnight borrowings in the previous quarter.

Asset quality remained strong in Q1 2024. Nonaccrual loans, excluding government guaranteed balances, totaled $2,194,000, or 0.19% of loans, as of March 31, 2024, compared to $1,770,000, or 0.20% of loans, as of December 31, 2023, and $621,000, or 0.06% of loans, as of March 31, 2023. The Company had no OREO for Q1 2024, Q4 2023, or Q1 2023.

The Allowance for Credit Losses ("ACL") totaled $11.2 million, or 1.22% of loans held for investment, as of March 31, 2024. The Company recorded $645,000 in provision for loan loss expense in the first quarter of 2024 compared to $1,600,000 in provision expense in the previous quarter, and $890,000 provision in the first quarter of 2023. The Company recorded net charge-offs of $77,000 in the first quarter of 2024.

Capital ratios of the Company and Bank continue to exceed the "well-capitalized" capital levels set by their respective regulators. As of March 31, 2024, the Bank's Tier 1 leverage ratio was 12.27% and the total risk -based capital ratio was 14.97%. As of March 31, 2024, the Company had tangible common equity (total stockholders' equity less intangible assets) of $111.4 million and tangible book value per share of $25.16. Tangible common equity increased $2.673 million in Q1 2024 due to quarterly earnings of $3.076 million offset by a $755,000 increase to accumulated other comprehensive loss ("AOCL") related to increased unrealized losses on our securities portfolio. The Company's tangible common equity to tangible assets ratio was 9.45% as of March 31, 2024, down from 9.62% in the previous quarter. There were no paid dividends during Q1 2024 or in any quarter presented.

About Bank of Idaho Holding Company

Bank of Idaho Holding Company is a bank holding company headquartered in Idaho Falls, Idaho. The Company's subsidiary, Bank of Idaho, is an independent commercial bank providing a range of business, personal, and mortgage banking products and services, as well as trust and wealth management services, to customers in Idaho and eastern Washington. The Company's common stock is traded on the OTCQX exchange under the symbol "BOID."

Non-GAAP Financial Measures

Some of the financial measures included in this press release are not measures of financial performance recognized in accordance with generally accepted accounting principles in the United States ("GAAP"). These non-GAAP financial measures include "efficiency ratio," "tangible common equity," "tangible common equity to tangible assets," "tangible book value per share," and "pre-tax pre-provision net income." Efficiency ratio is computed by dividing total noninterest expense, including intangible expense, by the sum of net interest income and noninterest income, including gains and losses. Tangible common equity is computed by subtracting goodwill and core deposit intangibles from total stockholders' equity. Tangible common equity to tangible assets is computed by dividing total assets, less goodwill and core deposit intangibles, by tangible common equity. Tangible book value per share is computed by dividing tangible common equity by common shares outstanding. Pre-tax, pre-provision net income is computed by adding provision for loan loss expense and income tax expense to net income. The Company believes these non-GAAP financial measures provide both management and investors with a more complete understanding of the Company's financial position and performance. These non-GAAP financial measures are supplemental and are not a substitute for any analysis based on GAAP financial measures. Not all companies use the same calculation of these measures; therefore, this presentation may not be comparable to other similarly titled measures as presented by other companies.

Forward-Looking Statements

This press release contains, among other things, certain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including, without limitation, statements preceded by, followed by, or that include the words "may," "could," "should," "would," "believe," "anticipate," "estimate," "expect," "intend," "plan," "projects," "outlook" or similar expressions. These statements are based upon the current belief and expectations of the Company's management team and are subject to significant risks and uncertainties that are subject to change based on various factors (many of which are beyond the Company's control). Although the Company believes that the assumptions underlying the forward-looking statements are reasonable, any of the assumptions could prove to be inaccurate. Therefore, the Company can give no assurance that the results contemplated in the forward-looking statements will be realized. The inclusion of this forward-looking information should not be construed as a representation by the Company or any other person that the future events, plans, or expectations contemplated by the Company will be achieved.

All subsequent written and oral forward-looking statements attributable to the Company or any person acting on its behalf are expressly qualified in their entirety by the cautionary statements above. The Company does not undertake any obligation to update any forward-looking statement to reflect circumstances or events that occur after the date the forward-looking statements are made, except as required by law.

CONTACT:

Matt Borud, Bank of Idaho

Phone: 208.412.2322

Email: mattborud@bankofidaho.net

SOURCE: Bank Of Idaho Holding Co

View the original press release on accesswire.com

More News

View More

Recent Quotes

View MoreQuotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.